SUP-erb work!

After provide a near spot on H1 forecast I’m sorry to say my H2 forecast is rather wrong!

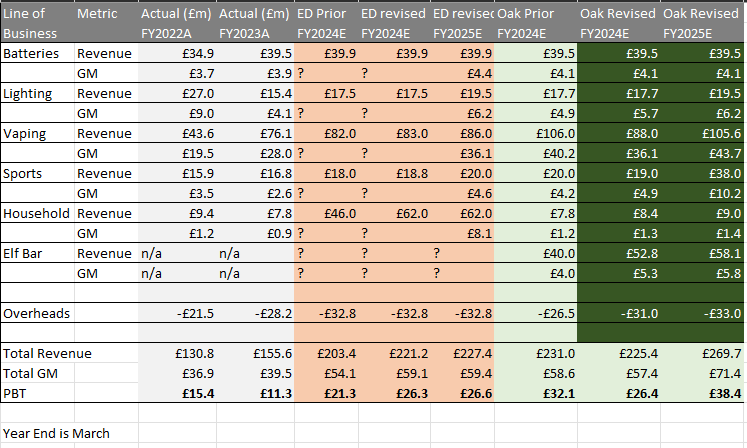

It’s too low! It now transpires in a cheeky trading update this afternoon that my prediction that profits will grow far faster in FY24 H2 and my Y25 will actually be nearly achieved in FY24.

On top of this a £1m buy back has been announced. On a current market cap of £136m its effect will be to shrink something like 0.7% of shares, at current prices, but it sends a signal. That despite the disposable announcement SUP is flying!

You have to make your own decisions and this is not advice but I feel strongly that many will fill your boots. Today began with an 11% drop, that drop rapidly returned to zero loss and ended up 10% on the day.

My forecasts are as below. My forecast of a PBT of £38.4m will be nearly achieved in FY24 (£37.5m adjusted EBITDA equates to about a £33m PBT)

Also SUP forecast that today’s news on disposables will BRING FORWARD sales and mean sales and profits in FY25 (which begins 1st April this year) should be even higher.

Plus the recent acquisition in Hayes, London at below £0.2m cost and book value of £1.2m bodes well for the sports business with a 40% increase to capacity, bought at a fraction of its price. SUP’s Sci-MX protein product is continuing great guns but I would not be at all surprised to see further brands being acquired where this capacity proves useful. We are not watching a static beast; quality management is driving the success at SUP.

Disposed to Change

Today’s announcement to ban disposable vapes by the end of 2025 makes SUP seem perfectly positioned. It has already set out changes to its packaging, its flavours and is already compliant with its remaining supply chain.

Zeus’ rationale is based on:

100% of revenue from disposable vapes is removed from end of 2025.

80% of disposable vapers will switch to an alternative pod/refillable vaping product which sells for, on average, ~75% the price of disposable vapes. So 75% of 80% is 60% of disposable revenue will convert to Refillable Vapes. The blended gross margin on refillable vapes is estimated at 13%, about the same as margins on disposable vapes.

SUP reveals disposables account for about £9 million of Adjusted EBITDA. Using Zeus’ estimate of 40% reduction in profit from the disposals ban that’s £3.6m net profit reduction….. from FY27 (the ban comes into force from the end of 2025 and the FY26 y/e is 31/03/26).

In the grand scheme of things today’s news is a case of who cares! A £3.6m loss through a slightly lower margin on refillable Vapes, when SUP has grown from £18.1m adj EBITDA in FY22 to more than double £37.5m adj EBITDA in FY24 isn’t material.

Conclusion:

Today’s news puts SUP on a PE of below 8.

For a growing company, leading in the area of vaping with strong, resilient cross sell into other products this company continues to impress.

This article is not advice. My advice is to get advice if you need advice.

Have a good evening

OAK

> of all it’s not a large amount and second of all it’s buying shares at a premium to NAV (so it’s actually dilutive to shareholders).

No, that's not true and not how it works. Companies aren't worth their NAV, their are worth their future discounted fcf.

It's only value desctructive if a company buys back shares when the share price if overvalued to it's future discounted free cash flows, NOT nav.

Backing up the truck here...