I KDNC believe it

What should investors make of Cadence's dilution?

Dear reader,

£0.5m raised by Cadence (KDNC) at an eyewatering 43% discount. Surely no share is worth holding after suffering those kinds of dilution?

Cadence Minerals (AIM: KDNC; OTC: KDNCY) announces that it has successfully raised, subject to Admission, £500,000 before expenses (the "Fundraise") through the placing of 16,666,667 new ordinary shares (the "New Ordinary Shares") in the capital of the Company at a price of 3 pence per Ordinary Share (the "Issue Price") and the issue of warrants to the subscriber of the New Ordinary Shares in the ratio of one warrant to each one New Ordinary Share subscribed for (the "Warrant"). The Fundraise was with a single institutional investor.

Or is it?

Having run the numbers today, I found the dilution is less severe than you might think. Part of the reason for this is that the money is being poured into optimisation studies ahead of the definitive feasibility study of Amapa, expected later this year.

Let me talk you through the numbers.

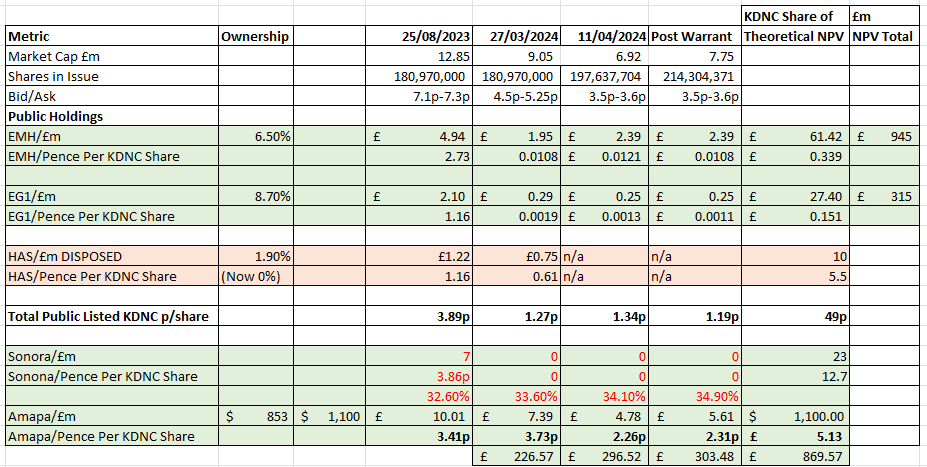

Last August, when KDNC was trading at 7.1p bid and 7.3p ask its publicly listed holdings European Metals (EMH), Evergreen (EG1) and Hastings (HAS) were worth 3.89p per KDNC share.

EMH and EG1 are lithium plays and lithium miners have had a torrid 12 months. The price per tonne has cratered, falling by 70%. This is the price over 12 months. However the future prospects for lithium are bright, not least because of EVs but also electrification and the need to manage power from intermittent renewables. In fact you can see lithium is 10% above recent lows.

EMH

EMH fell accordingly this past year, but also on delays to its DFS. Reaching a low of 13.5p which meant KDNC’s 6.5% holding equated to just 1.08p per KDNC share last month. Yet today (admittedly on a positive update that it can successfully produce Lithium Hydroxide and Carbonate - the two forms of lithium industry desires) it reverted to 1.21p/share. But that’s increased to 1.2/3.5 vs 1.08/4.5 so from less than a 1/4 of KDNC’s value to now over a 1/3rd.

More than this, the economics, the IRR, the flow sheet, the geography (proximate to German and Czech car production), the backing (CEZ is a multi-billion owner of the other 51% of EMH’s Lithium Mine) are all very attractive. Based on a £945m Net Present Value**, KDNC’s 6.5% holding has a NPV value of £61.42m or 33.9p per KDNC share. So a 10 bagger, if it can get there. It’s worth noting that EMH’s DFS is imminent after being delayed from Q1 to Q2. Here we are in Q2.

** you might sneer at the credibility number but know this. This is based on a 2019 PFS and is based on Lithium with Tin and Tungsten by credits. For each tonne of Lithium there’s 0.3T of tin and 0.1T of Tungsten. The Tin byproduct is priced at $21.5k (today it is $32k); Tungsten at just $420/tonne today it is $13k/tonne!

Evergreen (EG1)

EG1 has fared less well, price wise, but has actually reported positive news this week and last month. Its geochemical sample results continues to build on positive results and assay results from 1,174 soil samples received reflect similar large-scale lithium trends to those previously identified. Next step is to drill. KDNC’s 8.7% holding worth a mere £0.25m may seem irrelevant. Except there are follow on milestone payments (in shares) worth up to A$3.47m. On today’s EG1 A$5.69m market cap that would give KDNC 43.1% of EG1 (A$0.48+3.47)/(5.69+3.47). Again the NPV of EG1 is £315m so £27.4m to KDNC on an 8.5% ownership (15.1p a share). But 43.1% would be £135.8m so 70p a KDNC share. So a 20 bagger for KDNC, if it can get there.

Hastings was disposed of to raise cash for Amapa, so a £0.75m realisation so a simple 1.3X return, but would have been an 8 bagger at its NPV.

Sonora is a Mexican land holding with lithium, controlled by a Chinese firm, Ganfeng, and under dispute with the Mexican authorities. This is currently being adjudicated and there’s a err Mexican stand off. Perhaps the Mexicans will win and it’s worth zero, or perhaps not and it’s worth somewhere between 3.86p - 12.7p per KDNC share. As soon as any news breaks of the grab being ruled illegal (by Mexico’s supreme court) KDNC should at least double. So let’s call it a possible double bagger, but potentially more.

Finally, Amapa had an NPV of $949m but following some cost optimisations and improvement to its iron grades (which fetch higher prices) its NPV is somewhere north of $1.1bn. The “Amapa/Pence per KDNC share” is the share price minus the listed holdings, so was 3.41p last August, 3.73p last month and has dropped to 2.26p today. If the 16.7m warrants are exercised at 5p (as I expect they will) then assuming the £0.83m cash raised assuming that is poured into Amapa increases the holding from 34.1% to 34.9% so the Amapa price per share rises slightly to 2.31p.

However those warrants are a 6% dilution increase the Amapa holding by an (estimated) extra 0.8% of the $1,100m NPV….. that’s an increase in KDNC’s Amapa holding of £7m… so almost by KDNC’s entire market cap! 6% down and nearly 100% up!

Cash that gets us closer to a FID (final investment decision) on Amapa and unlocks the value there has to be welcome. 34.9% of $1,100 is £303.5m. Over a fully diluted 214m shares that’s still £1.42 per KDNC share. So a 40 bagger.

So, while the 43% discount on a small £0.5m raise looks shocking, if you process the actual numbers they tell a different story. Today’s rise in EMH just shows how oversold the whole sector is and how a positive update drives a swift reversion in price.

A theoretical 71 bagger even after discounts and dilution, based on net present values of 4 assets - part ownership of EMH, part ownership of Evergreen, land holdings at Sonora, and the Apapa Iron Ore operation.

That’s what the numbers say, in any case.

Regards,

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".