Dear reader

Places like Copper-filled Fiery creek fire the imagination. Uranium Olympic Dams too.

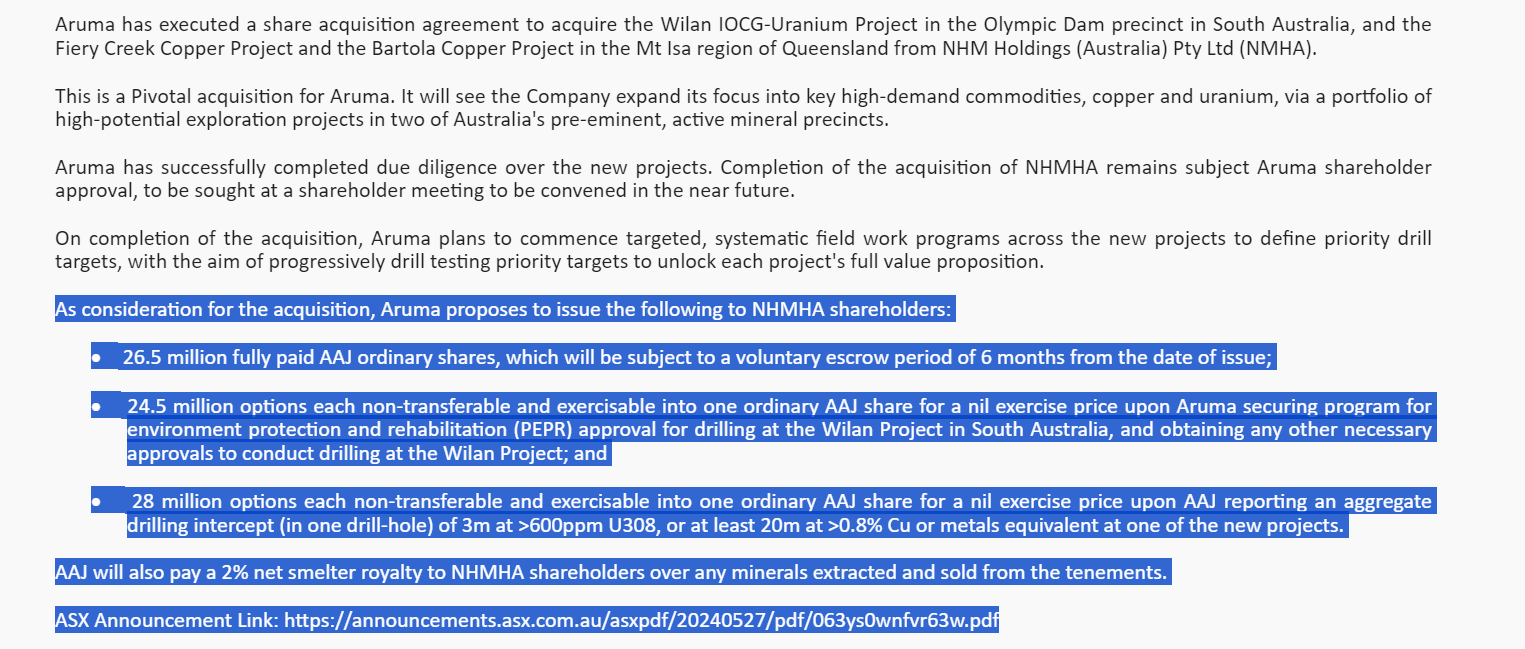

Today we recveived the following news.

Today’s announcement is, subject to successful drilling intercepts of Uranium or Copper, that 79m shares in ASX-listed AAJ be issued. AAJ currently has 196.2m shares in issue so the shares in issue would rise to 275.2m. 20% of the 79m are POWs so 15.8m shares. And that equates to POW owning 5.75% of AAJ in the event of success. Plus POW would receive a NSR of 0.4% of any minerals mined.

AAJ is a A$3.55m market cap so the theoretical value is about £80k. If they find something that holding could move to a £1m or more.

For an asset which POW didn’t even bother to list on their web site having an asset they’ve turned into £80k today and perhaps more tomorrow is alright for a day’s work.

GSA

Last week POW’s 75% acquisition of GSA transaction completed.

Following on from my article POW-dered opportunities where I spoke of a Memorandum of Understanding already in place with a major Saudi Arabian supplier of fly ash with several further discussions ongoing, those “several further” are described in some more detail:

MoU

GSAe currently has two Memorandum of Understanding in place with major Saudi Arabian supplies of vanadium and nickel bearing fly ash with advanced research due to commence shortly to optimise the metal extraction process route to enable detailed plant design, construction, commissioning and even operation as required for potentially several treatment facilities initially in Saudi Arabia.

So the potential of this deal is wide than one plant.

UK Industrial Waste

GSAe is currently working with a UK firm on the next phase of a program to develop a demonstration scale plant in the UK to process two types of industrial waste for extraction of critical metals from a single plant in the region of 20,000 ton per annum throughput. On successful implementation of this plant, initial discussions have commenced on the potential to construct a much larger plant with a targeted 200,000 ton a year capacity for long term processing and metal extraction as well as zero waste production also in the UK.

A new opportunity - and a 200kt capacity means this is must be a large processor.

Mining CO Saudi Arabia

GSAe is working with a major Saudi Arabian mining company to evaluate processes to extract REE and other strategic metals from tens of millions of tons of mine tailings in Saudi Arabia.

GSAe is in discussions with several mining and smelting companies to find solutions for their current and future mine tailings and slag residue.

GSAe currently have a UK Government Grant through Innovate UK for research in a consortium consisting of GSAe and the University of Lincoln ("UoL") as partners, alongside commercial supplier MLC (formerly Mississippi Lime Company) and metals trader Lipmann Walton & Co Ltd whereby GSAe leads the project and provide patented technology for metals extraction and concentration.

UoL is contributing proprietary technology in polymer manufacturing and filtering, while MLC will supply waste samples and offer technical advice. With over 2 million tonnes of metal-containing waste in landfills in the UK alone this research is a significant step towards a commercial operation with GSAe partnership.

Conclusion

Wilan offers another route to value, and joins a list of projects which are in play which on one level are worth practically zero yet could “strike gold”.

The exciting work at GMET’s pilot mountain continues. This increases in urgency now that the Chinese are imposing an $11k/tonne tariff on Tungsten from 1st August 2024.

POW’s Molopo farms drilling programme continues.

The “potential transaction” at FCM continues, albeit the FCM shares are suspended due to late accounts.

The preparations for the IPOs of UEE, FDR and New Horitzon Metals continue.

GSAe also offers a series of exciting capabilities and cash-generating projects.

So much going on at POW. Blink - and you could miss it.

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings including those held in VC stocks might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"