300. Triumph or Harrumph?

The Oak Bloke performance - Inception to Date

Dear reader

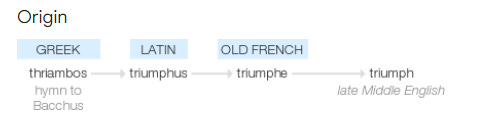

Leonidas might have sang a Thriambos, a hymn, while facing impossible odds. The truth of Leonidas was that while, yes, 300 Spartans marched out (accompanied by 900 auxiliaries), Leonidas commanded a force of some 7,000 Greeks at Thermopylae. But Death and Glory, and a triumph for Greece, indeed.

The Oak Bloke, meanwhile, claims no such command, and nor does he face any such foe, Immortal or otherwise. The connection is that the Oak Bloke has now written 300 articles, and a fitting picture for article 300 had to be in honour of Leonidas.

If a triumph can be claimed then it is 300 articles in 330 days. That’s not bad going! Could a Spartan write more speedily? Too fast and you make mistakes say some, you’re writing faster than I can read said another! Readers ask are you one person (err yeah, who else would I be? Me, myself and Irene?). Another asked is the Oak Bloke actually an AI? That one made me chuckle. If I were a Johnny 5 I’d probably need to give output.

As is my habit, this article is to pause and reflect on the successes and failures of the Oak Bloke. After all as investors we will not get all things right. We enjoy triumphs and suffer setbacks. We risk becoming complacent in the face of success and to double down on conviction in the face of adversity. Like a Canute we cannot command the ebb and flow of markets. Canute could have considered better timing. Wait for high tide and command the sea to recede and it shall obey. If only the markets were as predictable as tides. Canute had an easier task than investors, if you think about it.

We also rely on (and even pay for) sources of information that “should” be accurate but aren’t always. So sometimes those sources of info like in the RGL-er can trip you up and make you look foolish. But also that simply other times that we are human and we make mistakes and sometimes miss info in the reams and reams of RNS’s and Annual Reports. If I were an AI, I could simply blame hallucinations. Flap my Johnny 5 eyebrows downwards and look abashed, or leak a bit of engine oil from my camera eyes.

So on to the actual article. And perhaps to think a little more on triumph. As a reader of investment article ideas (I’m talking about you, reader) do you wonder whether you are wasting your time? I mean if reading these articles is a waste of time then you must stop and never return. The problem is how can you tell?

Of course you could go through each one of my 300 articles you could note down the 83 different companies I analysed (to a greater or lesser extent) the past 11 months, you could note down the date of the article when I gave an opinion about the idea (remember “this is not advice” as the mantra goes), you could look up the share price on that date. You could then look up today’s share price and work out the gain or loss. You could then add up the winners and the losers. You can average the percentage wins and average the percentage losers and work out a true ROI of the merits and perils of listening to the Oak Bloke. You could couldn’t you? But would you?

Probably not. Which is why I said article 300 was special.

I did.

I was quite curious, you see. Like you, I wondered whether I am wasting my time writing. Do the triumphs outweigh the fails? Is there any point? Regardless of today’s share price, there is a benefit to me, as I’ve written a number of times before, that setting out my thesis battle tests the idea. Cements my understanding. I’m also extremely proud to have been able to raise a substantial amount of money for charity through my writing. If I’d done an actual fun run instead I doubt I’d have raised anywhere near as much, and my feet would hurt besides. Also I enjoy writing articles.

Anyway, I bet you’re curious to know the results?

I shall delay no longer.

Evens. If you acted on each of my ideas the day I first wrote about a company, you’d have broken even. Now there are a number of factors to consider here.

First of all I calculated based on closing prices at the 23rd July. So “today” is the 23rd July throughout the article.

Second, I write about a number of ideas more than once. DEC is probably the idea with the largest number of articles. Some articles contained multiple ideas. So I’ve gone with the earliest date.

Third, would you buy and hold? Perhaps, perhaps not. A number of ideas could be traded, or could be top sliced, could be averaged down. GROW, for example, grew and is up 44% from 16th September to yesterday but it hit £4.22 a month back and I top sliced, while I bought back more at £3.44 and it’s going back up again. My analysis assumes the same amount invested in each and every one of all 83 ideas and held from date of idea to the 23rd July. Although I do explore the highs and lows later on. It isn’t at all logical that a reader would rush out and buy on the day of an article and not sell until today. So I investigate what if you’d bought at the lowest price on or after my article date and then sold at the highest price after the article and before today.

Fourth, I generally write articles that are based on an existing or potential long position (as do most of us I think) so why would I go about looking to spread fear, uncertainty and doubt? Not my natural style. But there have been occasions when a reader has asked me to look at a particular stock and I’ve then written an article to say why I like or don’t like it. Also there are some stocks where I have been curious to understand their vast success in “the Fun Run” and have come away thinking there are risks or the valuation feels fully valued, and have said so. So far I have been right on most if not all of those, too. So for those where I’ve had a “bearish” stance (although to be clear I’m not shorting anything) then any falls in price subsequent to the date of my article I consider a win.

Fifth I’ve not considered Dividends. As readers will know, the OB 19 has delivered a substantial return via dividends in 2024 so calculating the dividends on 83 ideas would have been a vast amount more work to calculate. But you could factor in a couple of percent if you liked.

Sixth, I’ve used bid/ask where possible i.e. the “buy price” is at the ask price, and the “outcome” is the bid price yesterday - at market close. I used HL to deliver the data.

Seventh and this is the most important of all. It is ENTIRELY in your gift, reader, to act or not act on any of my ideas in whatsoever way you wish. The point is it is unlikely you would or could have acted on each and every one of these ideas the very day I realeased them and want to still have all 83 holdings and not sell a single one until today. So the analysis is artificial in some ways. But nevertheless gives you an idea.

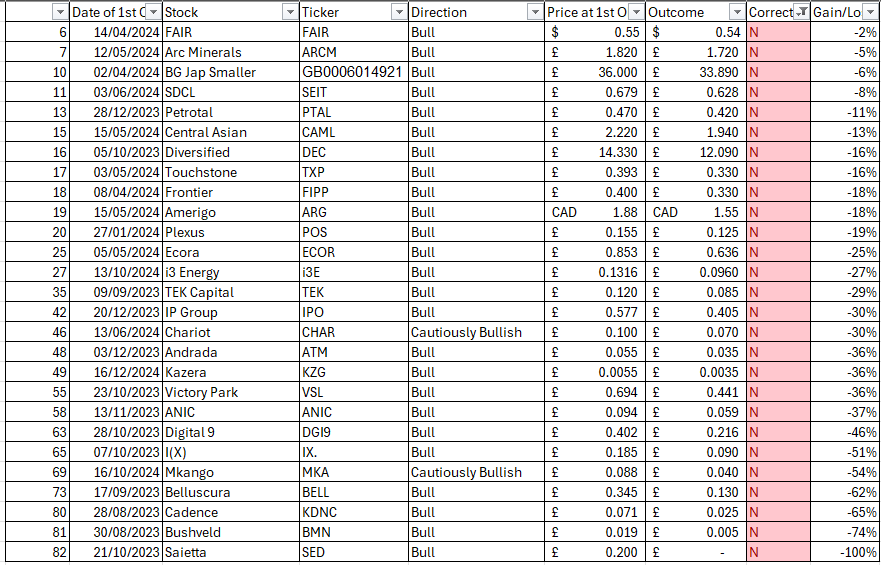

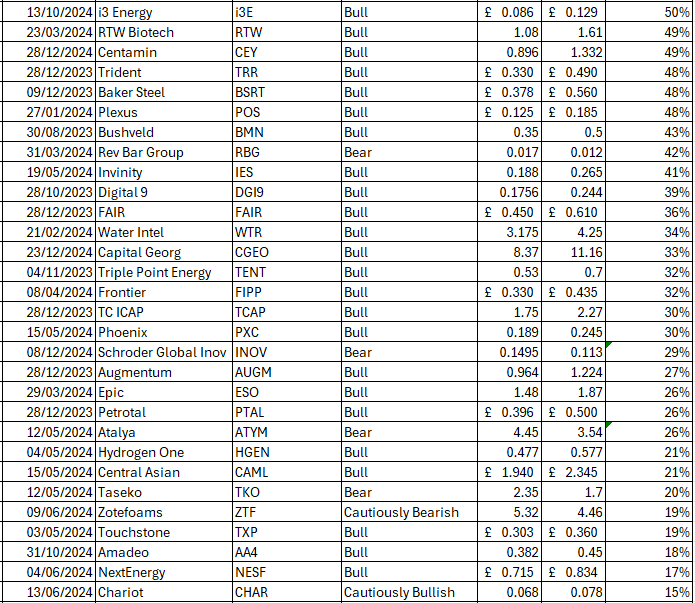

LOSSES DATA (DETRACTORS TAKE NOTE)

27 ideas have lost money and 1 was a catastrophic 100% loss. Eagle-eyed readers will spot quite a number of OB19 constituents in the losers too. No wonder I’m nearly in last place in the 2024 Fun Run. Ouch.

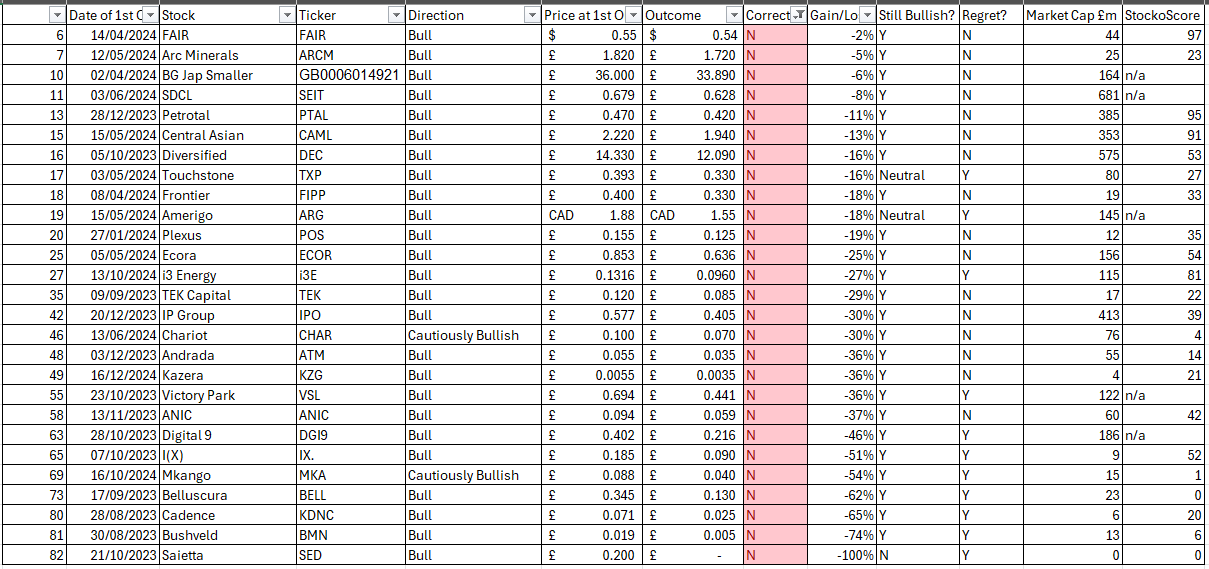

The first column is just a unique reference, the date of 1st OB article comes next. Then the stock and ticker. The gist of the article “Bull” up or “Bear” down. Price at the date of the article comes next then the price at the 23rd July. Next is it a gain or a loss and what gain or loss (%) is it.

There is a reason to show you the losers first. It struck me that it would be valuable to seek patterns. Are these of a certain size? Are they a certain vertical? Are they speculative? What is the pattern? Are they a low score on the Stocko system? How did they lose?

While, yes, certainly I can see “Copper”, “Oil”, Venture Capital, Special Situations, Small Cap technology, but there’s a bit of a hot potch and no decisive reason that I see.

Certainly the heaviest losers have a commonality that cash has held them back, led to dilution or made them go bust. Although that’s not true of ANIC and no longer the case for DGI9, now funding is in place for BELL and BMN the risk of cash has diminished, even ATM and CHAR have secured funding. Meanwhile IPO for example sits on bags of cash plus is achieving realisations at book so cash is not a factor there.

Adding in market cap and stockoscore doesn’t explain things terribly well either (n/a means they don’t provide a score).

There definitely is a pattern of larger market caps have lost less on average and smaller market caps have lost more on average, but there are exceptions too.

Of course some articles are fairly recent. Arc Minerals for example has 2 months pedigree while Bushveld let’s say has had 11 months. If I’d begun writing about BMN 2 months ago it would not even appear in the losers list.

I also notice those with a higher stocko score have fallen less on average. But, this will also reflect that as they fall their scores have reduced. I(X) for example was an “86” when I included it in my OB ideas for 2024 list. Now it is a “52”. The investment thesis is no different in 7 months.

I also notice for example, CAML, that the 12 month low is £1.51 yet on the 15th May 2024 its price was £2.22. Perhaps I should have not written about Copper when prices were above $10k and while there was a buzz about copper. This is likely a consolidation in copper before a further push up. Trading economics forecasts that. It puts copper 20% above today’s $4.07/lb.

I will explore highs and lows later on. It makes very interesting reading.

You’ll also notice there’s columns for “still bullish” and “Regret?”. This is for myself but I’m happy to share it with you, to ask two questions. Ignoring that I’m on a loss where do I believe the share price will go from here.

For example Bushveld at 0.5p, let’s ignore that it’s a whopping 74% down and consider will it grow from here? Can it hit 0.6p for example (20% gain). I’ve answered yes to Bushveld. The most recent article explains my thinking why.

Remember too reader, that many of the great and good all had broker notes on BMN and target prices of something like 4p-8p. Even BNP Paribas. Canaccord Genuity spoke highly of Saietta until suddenly they didn’t. Fully appreciate some or even all of that was “paid research” but they are still hanging their colours - as did the Oak Bloke.

Second question was to ask myself, if I could go back in time and erase the decision to write about it, would I? Now the obvious answer is to say yes to 100% - because then I’d be bragging about a massive win and zero losses. But that is not the real world and the test I set myself was yes I could do that, but then I couldn’t own that stock ever again. So would I erase history if I could?

So in other words does the regret of the loss outweigh the loss of not ever holding that stock again and future gains (I don’t hold all of these ideas just to be clear). I concluded there was a point at nearly 50% loss where the regret outweighed any bullishness. But it was an interesting exercise.

The Winners

I haven’t carried out a similar analysis on why I’ve succeeded, but let’s look at some patterns.

First of all numerically I chose the right direction 48 times and the wrong direction 27 times. So statistically the Oak Bloke is right about 2/3 of the time, it would seem.

(Detractors believe I’m always wrong. Statistically that statement is untrue).

By the way, eagle eyed readers will notice 48+27 doesn’t add to 83. So 8 times there was no gain or loss - or in the case of JSE as I declared myself “watching” I am not going to count that one as a win or a loss. Here’s a list of those too:

I was shocked to see Revolution Bar Group (Ticker RBG) was at the same price as 31/3/24 by the way! I expected it to be zero by now.

Back to the winners:

Guardian has been a superb share and I wrote several times such as in POW-lot mountain as to the apparent value. The CEO appears to have captured the “Zeitgeist” of keeping shareholders informed, providing PR, interviews, stocking excitement from what I read in the chattersphere. If I compare GMET and similar projects the difference is in the presentation. Maybe Guardian Metals offers a lesson for the dilapidated AIM market of the standard of IR which is now expected by investors.

Pinewood, too, just seemed so obviously overlooked. My instinct is I need to look for more Pinewoods in the future. If there is a lesson to learn in 11 months perhaps that is it. No cash concern. Cash concern is on my radar.

While TEK Capital itself hasn’t been consistently positive, it did double bag this year (more on that in a little bit on how buying at a low point and selling at a top price would’ve been very profitable), while Salt, has delivered a 115% return from its private valuation as at 2nd October 2023 to its IPO and now public valuation as of 23rd July.

Others like Kavango (Ticker: KAV) on a 94% gain since my article was a total surprise to me and possibly to many readers too. There’s gold in Zim there hills! And nickel-copper in the BOTS too.

VC holdings like Molten, Chrysalis and and even Net Scientific all feature as wins and if I’d done this exercise a month ago would be higher than today. While the UK hasn’t enjoyed the Tech exuberance of the US, we nonetheless suffer falls when the US decides tech is out of favour. $1tn wiped off US tech. Ouch. I’m not surprised as I’ve expressed before.

Really great to see ideas like Venture Life have made 60% since I wrote about it on the 26th September. Supreme also - took a while but then shot up. Also ideas like “the complicated story of Hansa, Ocean Wilson (ticker OCN)” up 36%, I’d not realised it had done so well. Yet its latest NAV is £27.75 vs £12.45. I really must revisit OCN, again.

But at the other extreme, of minimal risers, ideas like Amadeo now back to the same price as last October have caught my eye. That, and AVAP, are on my “to do” list as I (and myself and Irene, for sure) embark on 301 articles and beyond.

A result of 0% (plus dividends) isn’t that great.

But at least you have something with the Oak Bloke you don’t find anywhere else. You do now have full disclosure, the facts. Warts and all. How many other investment writers have given you that?

But what about the highs and low analysis I hear eagle-eyed readers ask. You can’t finish on a 0% gain/loss without revealing what the possible gain could have been. After all, timing the markets, and choosing which - if any - of my ideas are worthwhile is your job reader, not mine. So let’s look at the max/min results, the extent of your potential triumph

An 46% average gain.

10 ideas which would have doubled your money if you could only have timed them perfectly. Guardian Metals, for example, if you’d sold during 7th July and bought at 28th December you’d have made a 379% gain. Or TEK you could have picked up for 6.25p on 28th December and sold out on the 16th Feb at 17p pocketing a 172% gain.

66 of 83 ideas could have given you double digit returns too.

This is based on waiting for the optimal buy date some time on or after the OB article date and then the optimal ask price later than that buy date and before today. I’ve assumed you only buy and sell once; of course you might buy and sell (trade) numerous times riding the waxing and waning of a share price. DEC seems to be one share I read where people say that’s what they do.

Of course I’ve now no losses because in my analysis I waited until the optimal moment. The optimal moment may have been the 23rd July so no loss. But, for example, at Bushveld it may surprise some people, to see you could have made a 43% gain pre and post its funding with Orion being agreed - over 48 hours. Totally appreciate that would have been a very risky trade, and the failure to agree terms could have probably meant a potential 100% loss. But it illustrates the possible.

Realistically we don’t (can’t) time things perfectly and that’s why hindsight is a wonderful thing. Neither our trades, nor our articles. But this final piece of analysis has interested me greatly to see the sheer extent a patient investor can buy in and sell out at incredibly advantageous terms. In other words, there are times rushing out and buying on day #1 is the right strategy but often setting levels and patiently waiting for the right price to appear and pouncing only when the price is right delivered (or could have delivered) enormous results.

So to conclude:

Reading the Oak Bloke delivered a net 0% gain or a 46% gain - take your choice. Plus dividends.

Statistically around 2/3 of my articles are on gains.

I’ll take that, the satisfaction of charitable money raised through my efforts and 300 article in 330 days as a trio of triumphs.

This article is one of reflection not triumphalism. I would like to succeed more than 2/3 of the time. I would like 0%-46% to be a positive number to 46%. I would like to not ever be in last place in the fun run (I’ve avoided it so far). I wrote that enjoying success risks complacency. By writing this, and by reflecting on both success and failure, I, as an investor, can learn lessons to take forward and improve.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

Look , i enjoy your writing a lot and in a couple of cases drill deeper by looking into the companies websites , financial reports etc. I weed out the companies with very low market cap and not much liquidity in trading. Also i am hesitant with mining ventures and nano caps.I did&do overweigh my personal favourites high conviction stocks like Supreme , VLG,for example. This made me a lot of money ytd. Going forward i will increase my position in IPO and DEC....So your writing does inspire and is a good basis for further research and I thank you for your time and effort to share this material with us.

Greetings from southern Spain

I really enjoy your writing

Thank you for the efforts you go to

It’s my no 1 lookout

If it wasn’t difficult, would you include Dividends?

It depends on the approach but this may be a major source of growth for a conservative investor.

I also wholeheartedly agree with the above comment about deep value versus momentum.

The large caps are possibly lifted by the tide of higher interest rates.

Isn’t there also some sort of Warren Buffett quote about, “it’s not how many times you are right and how many times you are wrong, but how much you make when you are right and how much you lose when you are wrong”

Here’s to the next 300