A rocket for MARS

MARS Marston's 1H26 results

Dear reader

Chief Rebel has been examining the heavens intently watching new ideas like SSIT, ironically leaving a space for me to speak of one of his 2026 ideas that remains on the launchpad: Marstons ticker MARS.

With Pubs closing every day in the UK thanks to Rachel’s taxes, there’s no space race for these venues - more of a MARS survival movie. How do you grow things in harsh environments? Find a recipe, put in the means to make it grow and be the last man standing - that can make you the greatest, in the words of Matt Damon:

Can you find Musky excitement at 1,325 pubs operator Marstons ticker MARS? Or a whiff of fear as MARS-upials quake and detractors lick their lips with fetid glee.

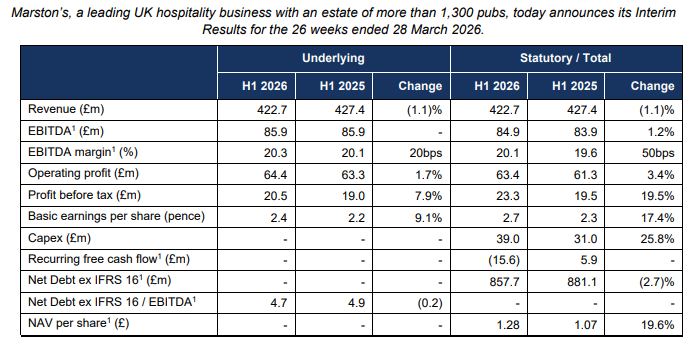

Not so fast. Its 1H26 results were solid although the market punished MARS, down 14% to 45p. Nothing to fear except fear itself? Let’s consider the facts.

“Solid” means -1.1% revenue, and “only” a 0.2X reduction in leverage from 4.9X to 4.7X. Reductions in debt are not fast enough exclaim detractors.

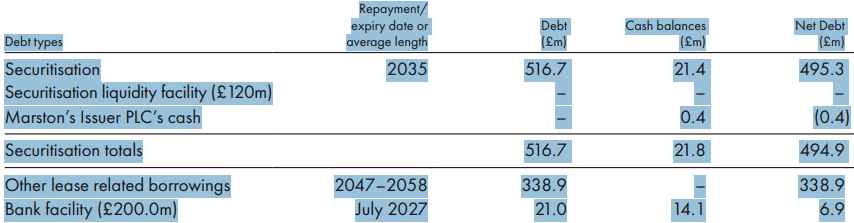

Is that true? Peculiar. MARS debt is safe as houses - or pubs. No cliff edge exists for these. Securitised debt, akin to a mortgage, means MARS borrows at a reasonable weighted average 6.4% with repayments out to 2058.

Hmm yes, there is the matter of a £6.9m net debt due July 2027. But £6.9m is nothing: That’s about 3 weeks of average cash from operations, or 3 days of cash gen perhaps with silly season World Cup fever round the corner. Cheer on the home nations? Nah, I’m cheering on you footie fans! (And your wallets)

Detractors then point out that revenue dropped -1.1% year on year, although half of this was due to temporary closures while renovations were carried out. The other part was softer midweek demand, although peak trading was up 5.3%. So we can play top trumps as to the good and bad aspects of the results, the point being that MARS are positioning accordingly with opening times and staffing levels.

Their bear case is based on a catastrophic explosion for those carefully planted metaphorical potatoes. For example this detractor commented:

“Those results were to the 28th March.

That is Before all the cost increases.

Minimum wage rises , Rates rises, energy rises and food cost rise to come.

Unemployment up customer base down”

Let’s examine the facts about that:

Min Wage means £12.27/hour which is a 6.7% increase. Alright for some. So assuming everyone gets an extra 6.7% from 1st April (even those not on min. wage) then that adds £5.8m in 2H26 - assuming headcount is static. It wasn’t static in 2025, and heads were cut by around 1,300. Technology and automation will likely replace heads, but yes there will be some impact.

Business rates rises meanwhile are unlikely to increase costs in 2H26 since most MARS venues are small and get lower rates under the new multiplier system.

Energy rises will be zero as MARS has hedged its energy for 2026 and 2027. Food cost rises are currently 3.3% but some say these could hit 10% by the end of 2026. It hasn’t happened yet and it’s not clear whether oil will go stratospheric - or not. Is the Green Chicken correct that all the fears from people like the OB are unfounded and high oil prices are a blip and will all blow over? UK unemployment is up 0.5% in 2026 to 5% it’s true, and catastrophically youth unemployment at 16.2% is up from 14.2%.

But don’t worry kids. After 18 months Labour guarantees work experience to get Britain working.

So detractors can point to some cost rises - but this is not a new phenomenon. MARS can (and will) increase prices and drive efficiencies to counter this.

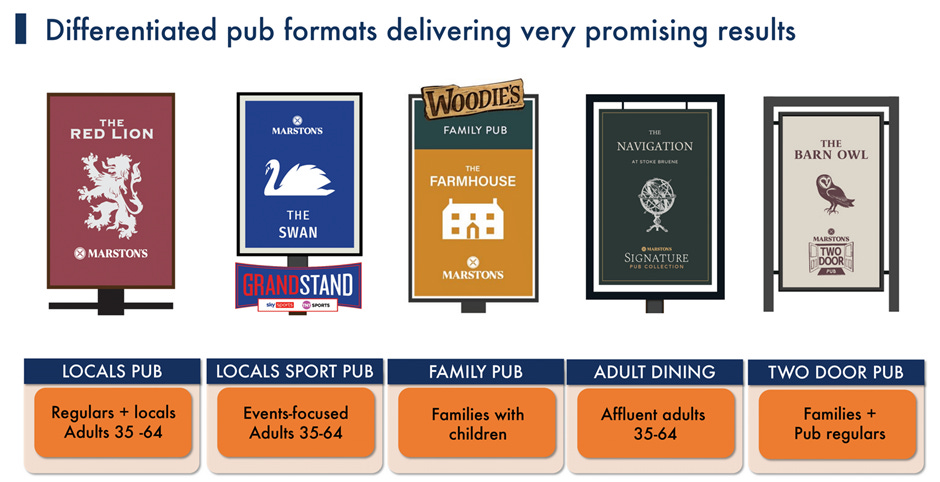

NEW INITIATIVES - FIGHTING BACK

MARS is launching new formats and initiatives to survive. The choice of format isn’t co-incidence or chance. The choice is carefully made based on data…

The selection of which pubs to convert is data driven and based on real-time data analytics across the estate:

DATA ANALYTICS USED TO CHOOSE FORMAT:

Demographics

Trading patterns

Propensity for event demand

Past spend behaviour

Labour productivity

A stand out among these formats is the Grandstand.

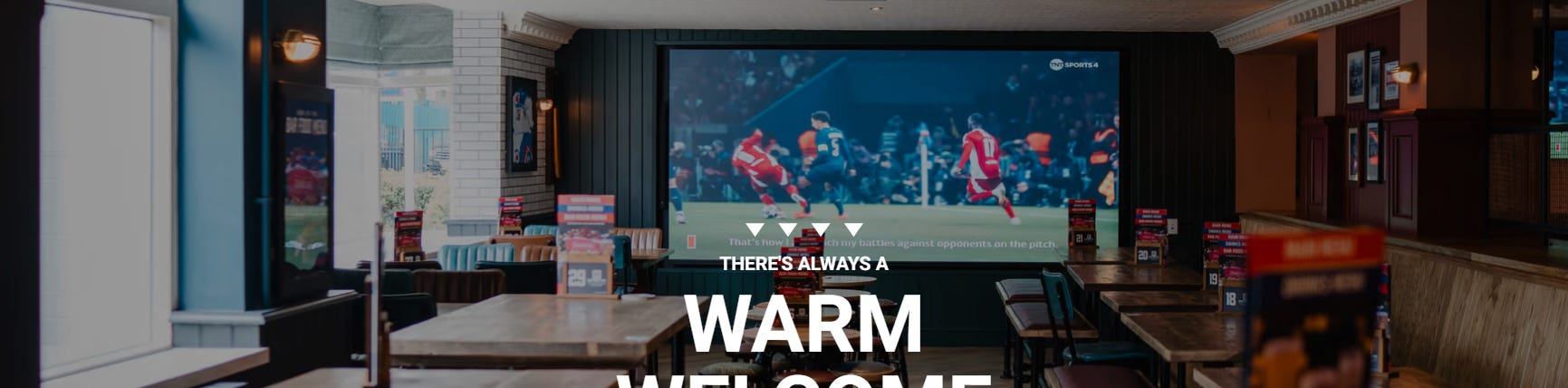

Grandstand

A Pub and a TV on the wall. Oh that’s so 1990s. I’m no great expert on evolving pub culture but pubs used to be places to talk, play pool and darts. Television wasn’t the centrepiece. It was the late 1990s that more and more pubs added TVs - I guess the advent of Flat Screens did it, as well as bSkyb showing sporting events. Pubs drew in crowds. Crowds meant more TV and bSkyb.

Fast forward to 2026 and we still love sharing sporting events with our mates. We just do. Home alone isn’t as much fun. And yes you can go over someone’s house to watch it on their 50 inch screen - but a MARS pub has a 120 inch screen - and all your mates will be there so are you going to be Douggie-no-mates and stay at home?

The focus at Grandstand venues is:

Energy and communal atmosphere - replicate a Stadium

Giant screens that show multiple live games shown simultaneously

Tiered stadium-style seating areas to maximise people’s viewing

Upgraded outside viewing spaces/beer gardens,

Integrated order & pay App - order and the drinks come to your table.

Sport covers Football, Rugby, F1, Boxing and Cricket.

If only there were unmissable sports events this summer. Oh wait…

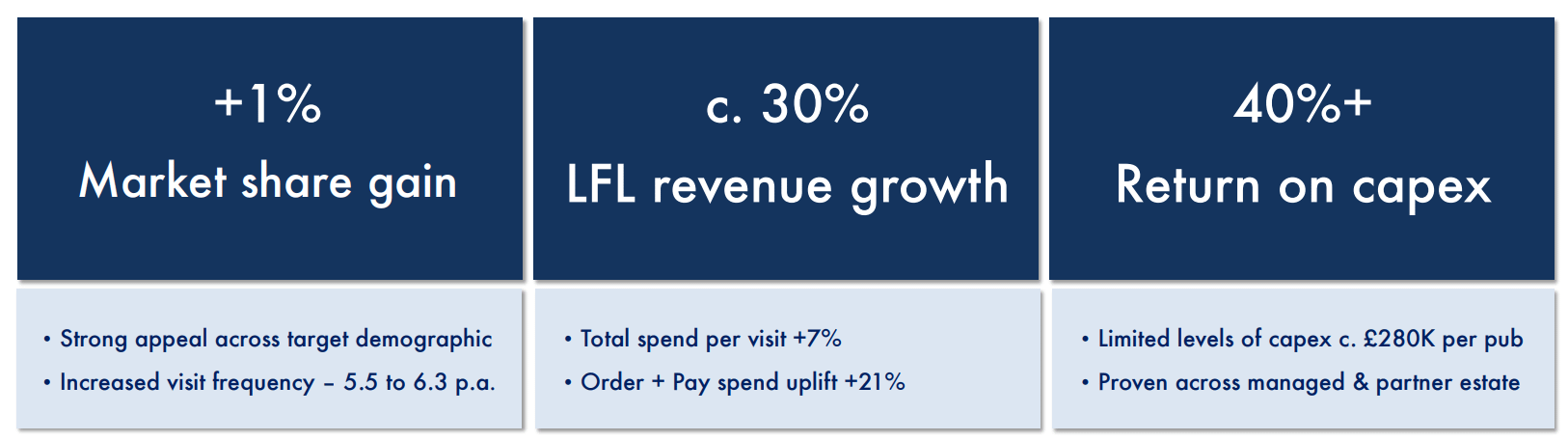

MARS says they have proved the model across 90 converted sites (so 7% of total) and their analysis shows:

Increased visit frequency

Higher guest reputation scores

Higher spend per visit - around 30% LFL revenue growth for Grandstand sites

EBITDA margins materially above group average, 40%+ return on capex.

At an average £280k refurb this implies a greater than £110k improvement to profit per pub per year. There’s no noticeable fading effect.

MARS believe a further 250 pubs can be converted to this format, implying a £67.5m expansionary capex cost and a £27.5m improvement to EBITDA so about +13%. Of course converting 250 will take time. 100 more will be converted during FY27.

Management also said the concept appears scalable. They identified roughly:

- 250 pubs potentially suitable for Grandstand conversion,

- within a broader 600-site conversion opportunity across all formats.

CASH MONSTER

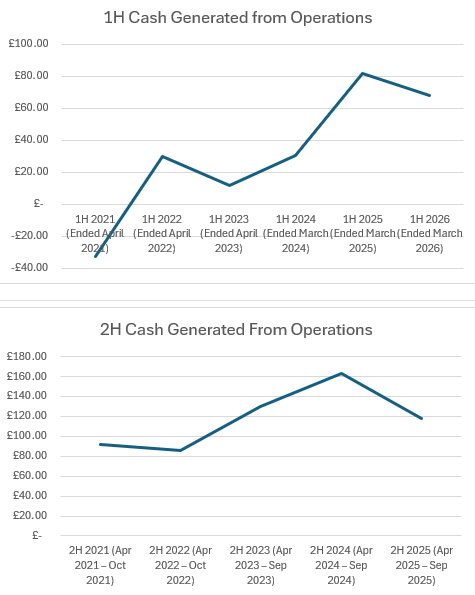

MARS is a cash machine monster in many ways. It generated over £10m more FCF in FY25 than FY24, and no less in 1H26 than 1H25.

This is cash from operations since 2021. Ok, 2021 was a pretty appalling year and of course is the covid period, but there have been plenty of challenges since then. Of course, yes, cash generated needs to be used to pay interest, pay down debt but the point is there’s no vast reduction of cash generation despite Rachel’s taxes, inflation, unemployment and all the challenges UK businesses face.

Yet if we look at a 7 year price chart the share is priced as though Covid lock down is in full swing….. Err it’s not.

Marcap of £285m and recurring free cash flow of £53m puts this at a P/FCF of well below 6X, that’s 18.5p of actual cash is generated each year for each £1 of shares. The number would P/FCF of 4X or 25p per £1 if you add back the £14m of expansionary capex.

Systems, Tech & Infrastructure

Marston’s has modernised its physical pub estate into a highly digitised, dual-revenue ecosystem:

Digital Sales Boost: Mobile and app-based Order & Pay platforms have driven a 10% increase in like-for-like sales, while table-based ordering delivers a 15% higher average spend than traditional bar transactions.

UK’s Largest EV Network: Partnering with Osprey Charging across nearly 200 sites, Marston’s has built the hospitality sector’s top EV network. The model requires zero capital expenditure: Marston’s operates on a profit-share basis on electricity and leases parking bays to EV firms, securing a steady rental stream while capturing captive footfall inside the pubs.

Management Team

The upgraded leadership team focuses heavily on digital delivery, consumer marketing, and aggressive debt reduction:

Tech Leadership: Chief Digital and Technology Officer Rob Beattie brings elite consumer pedigree, having run massive global digital infrastructures for Papa Johns, Domino’s, and Camelot.

Turnaround Strategy: CEO Justin Platt—a career marketing and consumer strategist from Merlin Entertainments—has revitalised the brand. Confidence is high, backed by a stabilising technical chart and significant insider director share buying.

NAV and VALUE

Valuation Disconnect: With zero material share dilution in five years and a £2.2 billion property asset base, Marston’s is on track to drop leverage below 4.0x EBITDA, paving the way to reinstate its dividend and attract institutional City buyers.

NAV per share increased to £1.28 (H1 2025: £1.07), up 19.6% year-on-year and approximately 24% since FY2024 (£1.03), reflecting progress since the October 2024 Capital Markets Day.

How real is that NAV?

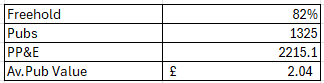

Five years of data backs up the tangible value where disposals have achieved £1.2m per freehold property - on average - and already at or above book.

The £2.21bn PP&E is fixtures, land, equipment as well as property but taking the 82% of the pubs which are freehold (1087) and dividing you get to just over £2m per pub NAV.

Did I mention you buy said pubs for a 64.8% discount to NAV when you buy MARS for 45p? 65% off and a pubs and restaurants business thrown in for free.

Let’s break it down to one pub! And One share.

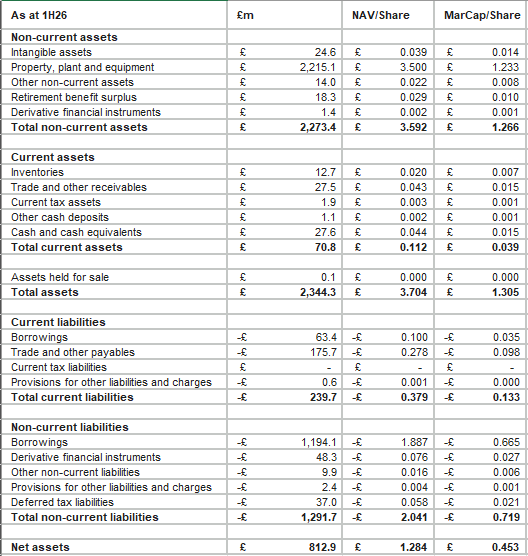

This is the balance sheet for 1H26 where you can feast your eyes on what a 45.3p share gets you. £3.50 of PP&E (pub, party time and entertainment?) and £0.20 of other assets offset by -£2.41 of liabilities.

If I take the £812.90m NAV and divide by the freehold properties that means of that metaphorical £2m pub you’d only see £0.75m of the assets due to creditors owning -£1.25m of that pub. But then again you’re only paying just over £0.25m for that pub. Wait what?

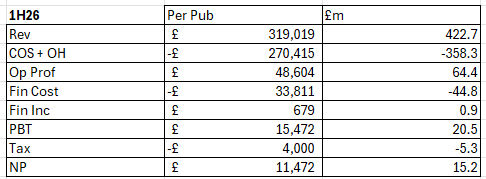

The One pub P&L

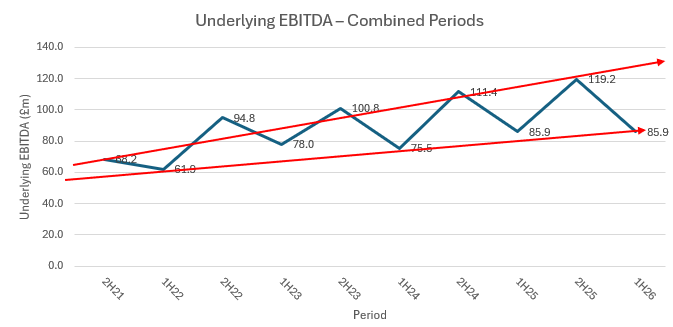

The winter half of the year is the worse half, as the 5 year EBITDA chart shows but in 1H26 each one of my 1325 pubs delivered £11.5k net profit after Rachel took -£4k.

Summer Season 2H delivers over double the profit, so my pub should deliver £35k-£40k over a year on £263.5k.

If I were buying a pub I’d be pretty happy, obviously my “landlord salary” is already in the costs so that ~£35k is investor return.

Besides - it’s a pub with land value, a building, an EV charging business, a restaurant, a pubs business with World Cup seats - for just over a quarter mill?

Just a quarter mill? I’ll be at the pub, but before that, I’m off to see a man about a dog.

NB the OB will be on holidays over the next week or so so look out for new podcasts, videos and articles later in June. If you enjoy this substack please do give back through Trees For Life and Aspire. This is your “subscription”.

Regards

The Oak Bloke.

Disclaimers:

This content is for educational and informational purposes only. It does not consider your personal circumstances and is not financial, investment, tax, legal, or professional advice. Nothing here is a recommendation, offer, or solicitation to buy, sell, or hold any investment. Investing involves risk, including the loss of capital. You are solely responsible for your own decisions

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Nice write-up!

I did a back of the envelope valuation of Marston's last year but ended up finding a higher-upside stock to pile into instead.

A director buying alongside a stabilising chart is worth more to me than any broker target.

You can see Platt's marketing background in how they're picking the conversions too, all data-led rather than gut feel.

https://www.marstonspubs.co.uk/shareholder-vouchers/

It's worth holding 500 for the vouchers. However not all brokers pass the benefit on - HL, II and Halifax do.