A Turney Client Privilege

Kavango's update Dec 2025 - an OB 25 for 25 idea

Dear reader

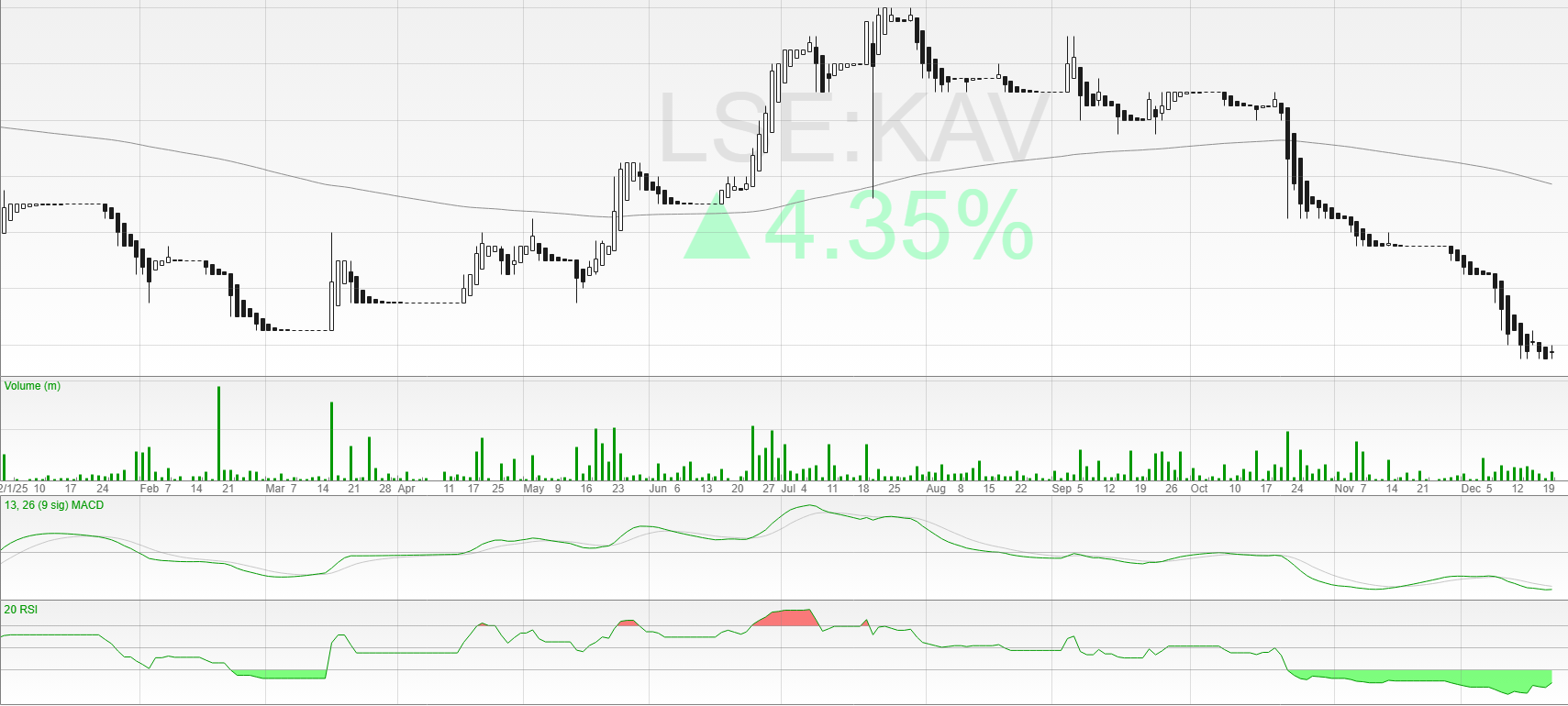

Excitement and progress at KAV gave way to a sell off in UK-listed Kavango falling to 0.6p in the UK. But not in Zimbabwe. Even on Friday the share is listed at the equivalent of 1.42p.

And last week a $383k fundraise at a 66% premium to its UK share price.

This OB 25 for 25 idea is down -8% at 0.6p from the 0.65p price I included this. If I bothered with technical indicators I’d probably be saying about its extremely oversold RSI of 17 which is now rising - a strongly bullish signal.

But instead I’ll stick to the fundamentals. Of course sentiment has taken a knock which the sudden departure of Ben Turney, now ex CEO. What went on there? We simply don’t know, and let’s call it a Turney-Client privilege although Purebond the majority shareholder is calling the shots here so it would have been their decision, and the remaining Directors are credible people who have succeeded in a similar venture before. It doesn’t feel like a reason to worry even if Mr Turney is a decent chap who in my view did a great job leading KAV.

Let’s revisit the KAV thesis:

No debt

Extensive shareholder support running into tens of millions of pounds, and not at discounted amounts.

A series of fully permitted mining leases in Zim with exciting indications of gold.

Prolific history of past Gold production at these projects both underground and open pit.

Current level of Gold production is 60 ounces/month

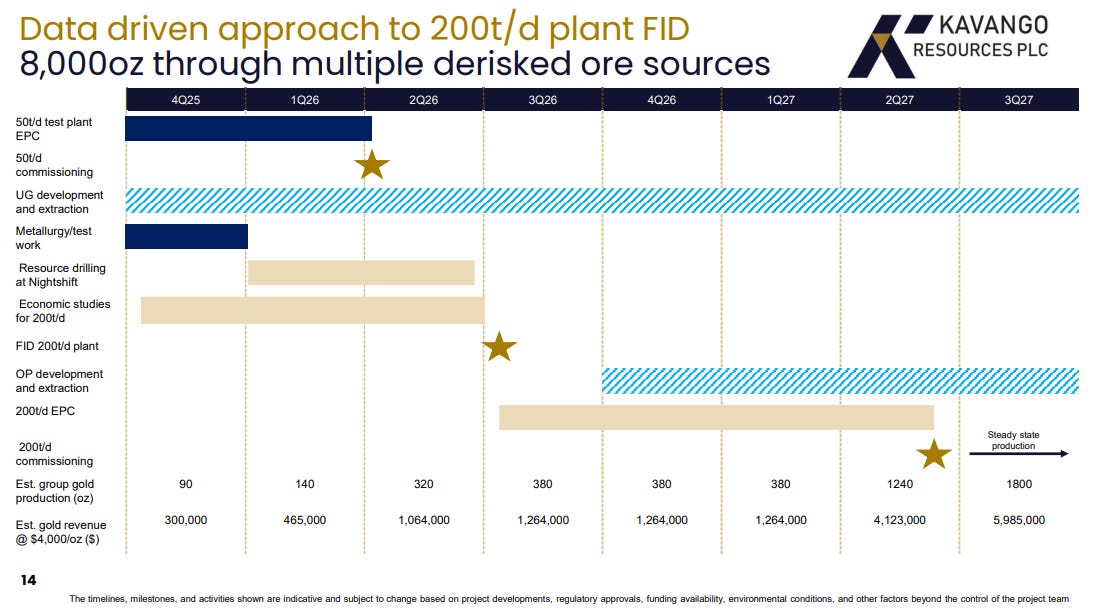

50 TPD expansion underway at Bill’s Luck (commissioning in 1Q26)

50 TPD would deliver a 1.6 Koz per annum of Gold run rate

250 TPD expansion planned (by 1H27)

250 TPD would deliver 8 Koz per annum of Gold run rate

Longer term plan to expand to 500-1000 TPD (16-32 Koz)

Several exciting Copper projects in Botswana

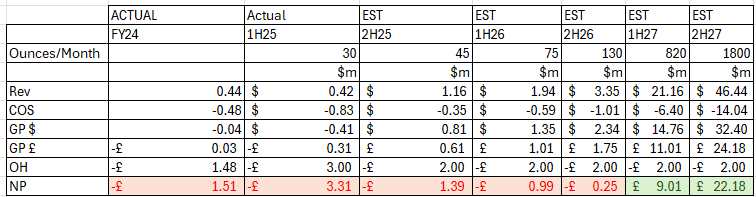

The above revised plan would get KAV to near to net profit break even, where the 250 TPD would take KAV to cash flow positive and modestly profitable. Higher gold prices or slightly higher ounces could do this too.

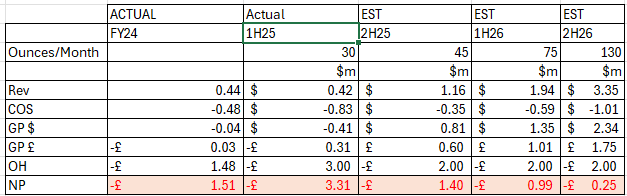

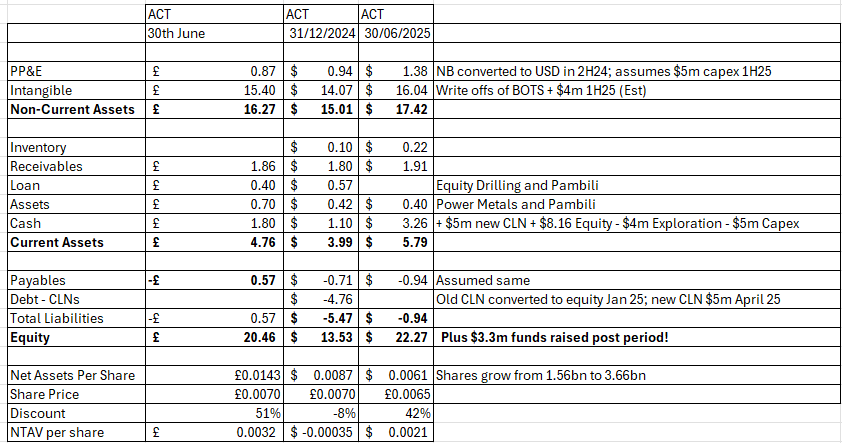

The 1H25 results were as below. Post period KAV have raised $3.3m and diluted shareholders by 0.6bn shares. Even so, and assuming a -$3.3m Loss for 2H25 KAV’s balance sheet remains quite strong with an estimated $5m of cash and receivables as at December 2025.

Where the share price is 1.42X book value. Not many gold producers you can acquire for that low a premium.

Of course the 50 TPD plant hasn’t yet happened and next Spring while this will substantially slow cash burn it does still leave a question over the cost to expand the operation to 250 TPD.

Perhaps more dilution. The 2027 picture even only at today’s $4300/ounce gold looks substantially different.

Of course other options might exist too.

KAV also owns 16.6% of Canadian-listed Pambili also operating in ZIM

Higher copper prices might find a buyer for KAV’s three Botswana Projects - the KSZ, the KCB or Ditau.

The KCB particularly is contiguous to Sandfire whose stock price has nearly doubled in 2025. Sandfire extracted 44.7Kt of copper equivalent in 2024 generating an EBITDA of $179m at a 52% margin. The margin in 2025 particularly now in December is much higher.

Political Risk

Fellow Zim Gold Miner Caledonia Reported last week:

“On December 17, 2025, the Zimbabwe Minister of Finance announced certain changes to these proposals in the second reading of the 2026 National Budget to the Zimbabwe parliament, specifically;

· The proposal to increase the royalty rate from 5% to 10% when the gold price exceeds US$2,500 per ounce will now only apply should the gold price exceed $5,000 per ounce.

· The proposed change to the tax treatment of capital expenditure whereby the current 100% upfront deduction would instead be spread over the life of the project, affecting the timing, but not the total amount of tax payable, has been withdrawn.

· The proposed change to levy withholding tax at 15% on interest payable on offshore loans has been withdrawn.

Conclusion

This has never been a low-risk idea and KAV disappointed in the past. It appears to be on track to reaching break even and then to profitability. It will join the many other companies that have successfully operated out of Zim for many years.

I continue to hold for the upside which I believe will come in 2026.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

KAV sadly still not on T212, but thank you OB for the assessment, which is (as PER) GREAT! If I could get your donor link to work I'd partake, but it won't work in either of my browsers (Brave and DDG) even with VPN and all other protections off.... It's not usually this hard to give money away! 🤣

Might have to reactivate my Freetrade account for this and other reasons, ta. Or use my non-taxpayer wife's..... 🤔