ANIC - are you ok - Part 2

You've been hit by, you've struck by, a smoooooth NAV lift!

More news today fom Agronomics.

Solar Foods. Makes protein. Not from Soy - which is problematic. Not from animals.

From a Microbe, with Electricity - renewable, of course - and carbon dioxide.

Agronomics held its 5.8% holding at book value (€6 million) based on its Series A/pre-Series B participation in Solar Foods, at a €103 million valuation.

Today a Series B round values Solar Foods at €178 million and the Series B was oversubscribed.

That’s a 72.8% uplift or £3.8m. Its RNS speaks to an uplift of £5.7m - so a further £1.9m gain based on the conversion of the Convertible Promissory Note.

-

What is Solein from Solar Foods

The process takes a single microbe, one of the billion different ones found in nature, and grows it by fermenting it, which is also called a bioprocess. We feed the microbe like you would feed a plant, but instead of watering and fertilising it, Solar uses mere air and electricity. With its current process, this is 20x more efficient than photosynthesis (and 200 times more than meat).

By using fermentation to grow protein, the bioprocess of our first protein product Solein® may not be traditional, but it is natural. And the best part? It won’t run out.

Its production process consists of the five following steps:

RAW MATERIALS

NATURAL BIOPROCESS

HARVESTING

PROTEIN POWDER

FOOD

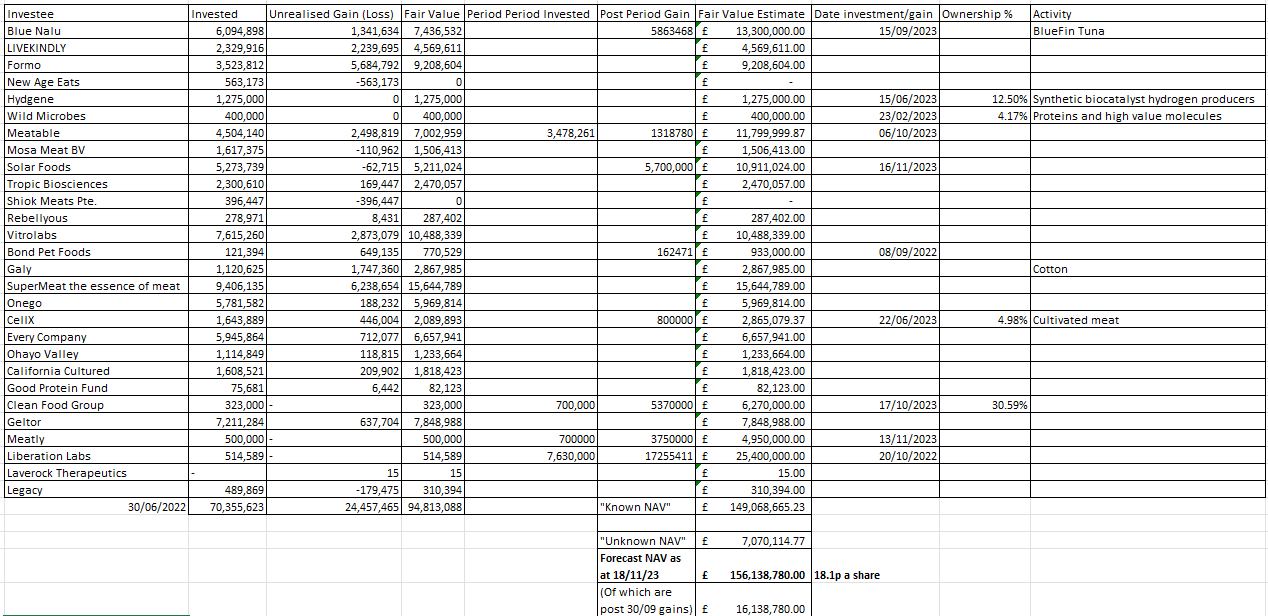

I’ve been piecing together an up-to-date NAV including the above news today.

Shocking! In ANIC are you ok I said the following (based on the September NAV).

ANIC: Agronomics, Market Cap £93.4m, Bid 9.3p Ask 9.6p, NAV 16.48p (30/09/23), discount to NAV 41.7%, 993.15m shares

I hadn’t considered post period progress.

ANIC: Agronomics, Market Cap £91.8m, Bid 9.1p Ask 9.4p, Estimated NAV 18.1p, Investments £164m + Cash £24m = £180.1m (16/11/23), discount to NAV 49.2%, 993.15m shares

So when Anthony Chow speaks to current NAV being “more like 21p a share” by the end of 2023 we’re around halfway there based on announcements.

Here’s a picture of what I’ve pieced together.

NB: I’ve used the £140m 30/09 NAV and added all the post 30/09 announcements which are just over £16m. I’ve then tried to reconcile to the 30/06/22 NAV (last published breakdown) but haven’t yet found £8.6m. So “Unknown NAV” isn’t some invention - it’s based on ANIC’s own published NAV but unreconciled, as yet.

If you have boots (Made from Cellular Agriculture leather mind), might it be the time to fill them with ANIC?

Half Price on a share whose NAV fair value has grown from £94m NAV to an estimated £156m NAV in 16 months. Gained through a deep nadir on the UK AIM, mind you.

Do the maths. Don’t do the maths. I’ve done the maths. Check my maths. Help me find the missing £8.6m.

-

This is not advice. If you need advice, I advise you get advice. Good luck in making your own investment decisions.

OAK

Hi Oak Bloke

ANIC dont help us with regular NAV figures (the last I can see via RNS on 2/5/23 giving the 31/3/23 figures) but the Liberation Labs value you are quoting looks incorrect- the 12/4/23 RNS gave that figure as a US$ 25.4m carry as against your US$514k below so thats most of the gap you are looking for hopefully?

Cheers. Steve