At 39p is it a Baker steel?

Mining the value at BSRT

BSRT - Market Cap £40.2m, 106.45m shares in issue, 36p ask/39p bid. NAV 66.4p/share.

Baker Steel Resources Trust

This article has changed name throughout the past week.

It started as “At 36p….”. So it’s gone up 10% this week - after a long time in the Doldrums amidst a falling NAV. Has the market woken up to the value?

I don’t think so.

It’s probably fair to call BSRT eclectic. If you are interested in a mix of public and private assets, early and late stage where the mine development risk (and reward) is on offer then this is an interesting play on that.

Do they do anything to do with baking? Nope. Is this to do with Steel? Nope.

The 2 gents running the show are Mr Baker and Mr Steel. Hence the name.

So let’s discuss some of its assets.

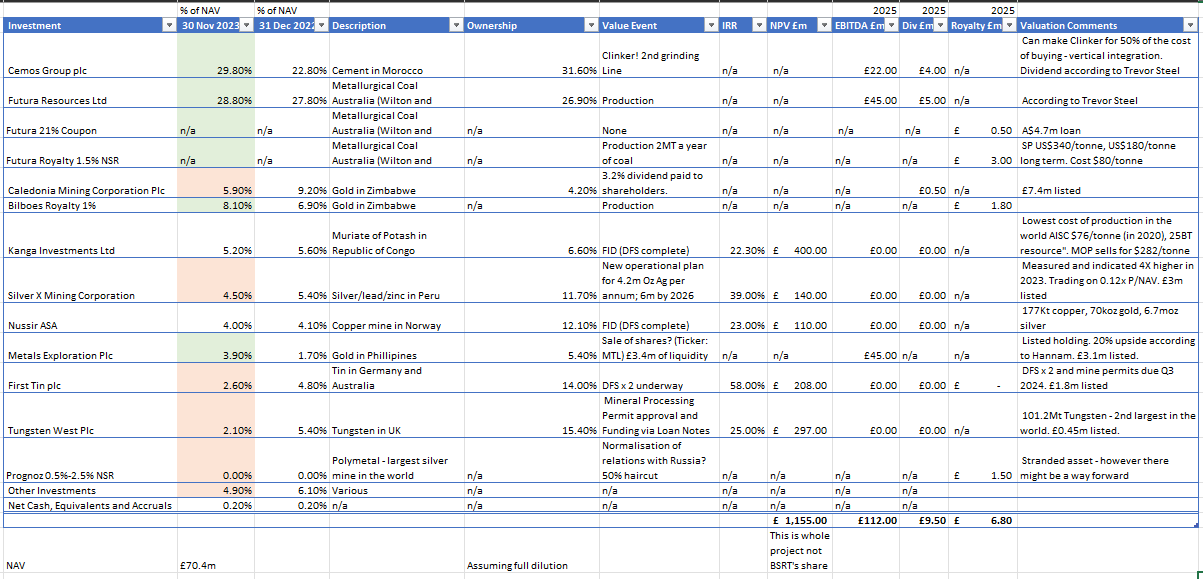

Futura

I was gobsmacked when the FID went ahead. Funding coal projects, even in Queensland Australia is so difficult. Rightly so! It felt like BSRT had no chance. But then it happened. Partly with BSRT funding it, with a convertible loan at 21% interest. Painful? No, that’s just the going rate to loan money to get a coal mine off the ground. BSRT also have a royalty and own a share of the company too.

The first mine is funded and a 2nd mine will either be funded from profits or from further funding. The build cost is very modest and the mine shares a facility next door so transportation and processing has needed minimal consideration.

ESG? Well this is metallurgical coal, not thermal. So used for Steelmaking. Unfortunately the world doesn’t currently have a viable alternative although electric arc furnaces and hydrogen powered furnaces are starting to look interesting. Realistically if we want to build stuff, we need steel. To get steel we need coal. The metallurgical baby was thrown out with the thermal bath water and no one cared. Not a single share purchase. BSRT didn’t move 1p on the news. Couldn’t believe it. I topped up straight away thinking I’d have no chance. I had every chance. Zero buys other than mine on the news. Am I wrong? Or is the market wrong?

Cemos

Cemos is a Cement manufacturer in Morocco. It started production in 2019 and is now expanding. It buys in Clinkers (no sniggering please) and the cost of making this is 1/2 the price of buying. So not only is it adding a 2nd line but also integrating clinker production. This is a photo of clinker and it’s made from clay and limestone. Who knew?

Caledonia (CLDN)

This is a UK listed gold miner based in Zimbabwe. BSRT did a deal to sell its share of the Bilboes mine which adjoins their Blanket mine (no it’s not the Frodoes mine). Great synergies of developing both mines etc etc. But Bilboes had a phenomenal AISC. $1000 an Oz. Incredibly cheap therefore profitable. I knew it had to be worth something. BSRT received a combination of shares and a NSR. It’s fair to say Bilboes is a year or so away from development. When the news was announced BSRT didn’t move 1p. Not a single purchase. I topped up back then too.

Others

BSRT have Kanga, Nussir where essentially they were due to IPO but got clobbered by the freezing of the market. These both have attractive economics (see the grid below) but need funding.

Tungsten West (TUN) did IPO but requires funds. Again attractive resource. First Tin is also listed (1SN) but is earlier stage (pre DFS).

There are then other listed holdings like Metal Exploration (MTL) and Silver X which are both listed and either profitable or heading to profitability. These have upside potential if held or there is an opportunity to realise cash and reinvest that in other opportunities.

Finally, the Prognoz Royalty is a particularly interesting holding. The problem is this mine is owned by Polymetal and located in Russia. So repatriation of the royalty means BSRT have written it off to zero. However, interestingly Barings announced 2 days ago they were able to repatriate funds from Russia, albeit at a 50% haircut.

This is how the valuation looks for BSRT:

Valuation Thoughts

As can be seen, the listed value (as at 08/12/23) of its holdings are £15.8m. That’s on a market cap of £40.2m.

So the net £25.4m for the forecast Royalties alone puts this on a PE of just 5 (excluding the Prognoz Royalty too)

Not in the price is Cemos currently generating £7m EBITDA but forecast to grow that to EBITDA of £22m in 2025, and to generate about £4m dividends a year. Including Futura and Caledonia puts this on a PE of 4 on the forecast dividends alone.

Not in the price are Nussir and Kanga with a pro rata NPV of £39m. That’s the value of the market cap alone.

Not in the price are the convertibles BSRT holds over holdings like Tungsten West and Futura. Difficult to value but could be worth millions.

It also assumes selling all the listed holdings are at sensible valuations …. they aren’t. First Tin for example has a NPV of pro rata £30m yet its shares are £1.8m. Potential 15 bagger. Silver X and Metals Exploration have serious upside both given their 2-3 year plans and where I believe Silver and Gold prices will be in 2025. Even Calendonia at £9 a share is thought by CG to be a target price of £14. UK shares are bombed out. The listed holdings alone could easily exceed £40m in time, in my view.

The terrible war in Ukraine will end. Things with Russia will subside. Polar acquisition (Prognoz) has a NSR of 0.5%- 2.5% where it’s 0.5% when silver is $19/oz. 1.25% at $24/Oz (as now). But 2.5% at $30/Oz Silver. Isn’t that hard to imagine Silver at $30 an ounce. The royalty caps off at $40m. (£31.7m). That alone is 80% of the current market cap of BSRT.

If you look over 5 years we appear to be at a nadir to the share price. The value and newsflow going forward should put a floor under the price.

Risk

The risk at BSRT is that progress can be slow. Mine development takes time. And it has been slow. Go back and look at their 2019 report. Some holdings have been in a 4 year holding pattern.

Generally risks have been numerous but unforeseen. Covid. Inflation. Interest Rates. Supply Chain Challenges. Frozen IPO market. War. Unfriendly jurisdictions. Take your pick on the risk(s). Will 2024 be better?

BSRT’s NAV has been hurt by falling valuations of holdings. Tungsten West particularly could imminently go bust. If that happens perversely BSRT could benefit. Perhaps by providing a bail out, finance, and taking a larger slice for their trouble. Of course PIs get shafted/diluted in the process. My point is perhaps if you can’t beat ‘em join ‘em. BSRT are smart investors in what I’ve seen of how they’ve financed and participated in funding rounds.

Comms

While there is a monthly report of NAV, with news snippets, it can feel slow. You can learn a bit more by visiting each holding’s web site of course. Holdings have their own presentations and news flows. Video comms are sporadic perhaps once a year.

There are quite a number of moving parts to BSRT.

Cash

A final thought is that the forward dividends and royalties alone make this interesting. It’s not just reliant on some listed holdings going up on the stock market - although there’s an element. It’s not just reliant on a DFS (definitive feasibility study) or an FID (Final Investment Decision) although there’s an element.

Perhaps there’s a synergy going forward where cash from one part funds the DFS or FID of the earlier portfolio. That’s usually how it works with VC too. Or perhaps there’s chunky dividends in the future for holders. Or maybe both. The fact there’s cash coming, gives optionality, not just hopes and dreams. That makes this attractive.

I read about “Bowling” as a type of technical indicator recently, and perhaps BSRT is one of those too, if you like your technical indicators. I prefer a different sort of numbers. Ones that have £s and pence. Or Tonnes and Ounces.

All in my opinion of course. I hope you find the article useful and entertaining. This is not advice.

Enjoy your weekend

Oak

https://www.ii.co.uk/analysis-commentary/investment-trust-boards-and-without-skin-game-ii528173

I note from this article that the chairman takes a fee of £42k pa but has no position in the trust's shares.

Do you have a youtube channel where you discuss your ideas and thoughts on these sort of things?