AUGM Grinder Value Finder

1H26 results at Augmentum Fintech - an Oak Bloke 2024 idea

Dear reader

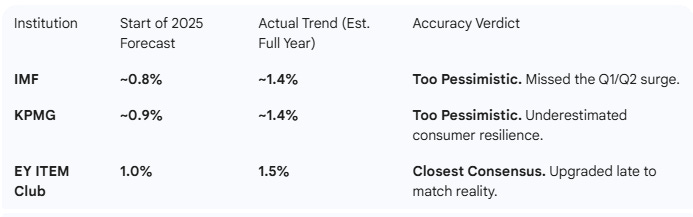

Most people were too pessimistic last year on UK growth. If we’d not seen uncertainty brought on by Rachel’s imaginary black holes and the scaremongering threats of her taxes that slowed things in 3Q25 then the UK’s GDP performance could’ve been even stronger. Considering the Trump tariff malarkey, 3.75% interest rates, ~3.4% inflation the UK also had to endure 1.4%-1.5% is a very strong result - in my opinion.

Far stronger than people believed at the end of 2024:

In 2026 where UK interest rates are forecast to fall (3.25% expected), inflation to fall (2.1% targeted), employment remains high and UK investment is at a 60-year high, and government spending too, even if consumer and business sentiment remains dented and demure. Moreover I believe a repeat of the budget shenanigans should not repeat in November 2026. Peace might just happen in the Ukraine, and the Middle East appears far less dangerous than 12 months ago.

Yet the forecasts are for just 1.1% UK GDP growth…. There is a simple test: Are conditions better or worse than last year?

Once you answer my rhetorical question and then make the assumption that the UK is going achieve even even more growth in 2026 - perhaps as much as 2% - then who benefits the most?

Banks.

But many finance and banking shares have already rocketed in 2025 (LLOY +79%, NWG +62%, STB +243%, ORCH +114%). Will there be more to come? Perhaps.

What about for those Banks who didn’t rise in price? Bargains in our midst.

AUGM didn’t rise. It fell. Its share price was down -15% in 2025 and is down -1.6% in 2026 YTD. Yet it holds a number of Challenger Banks and many more Financial Services Fintechs.

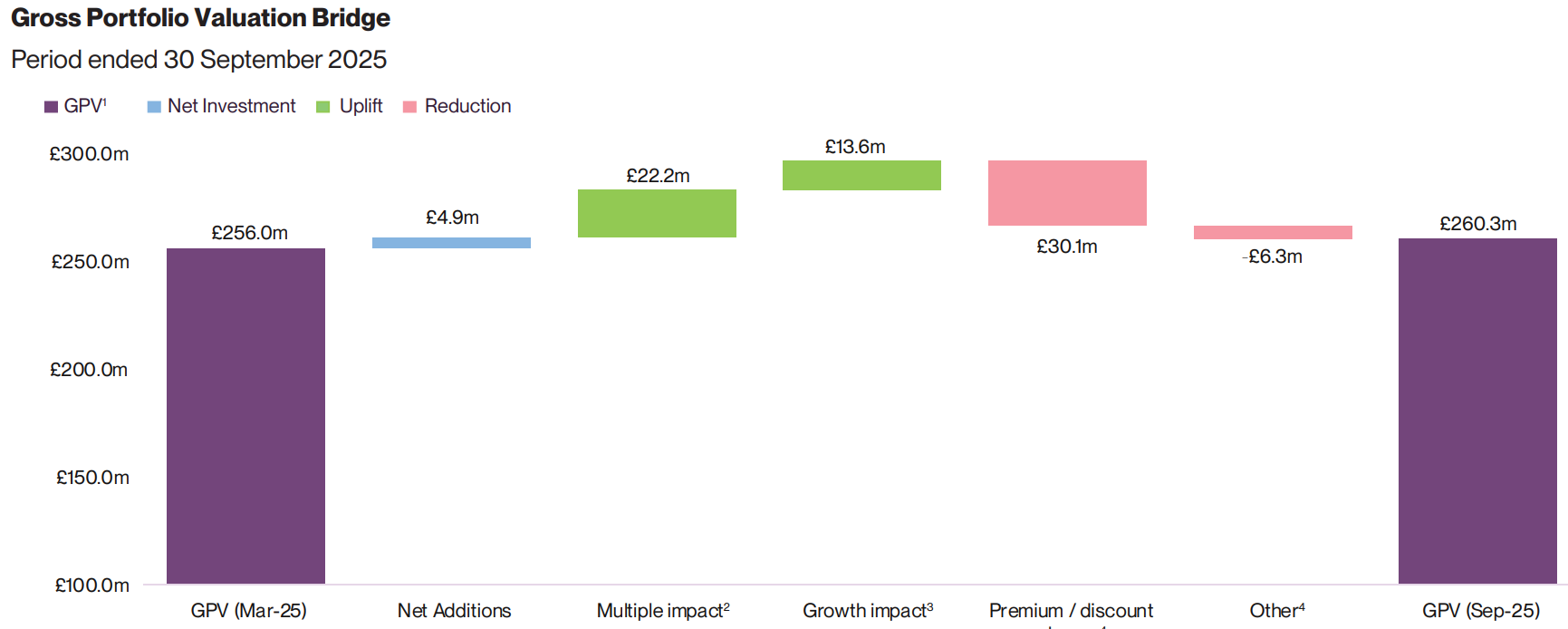

The AUGM September 2025 results were (on the face of it) meh, with NAV down -1.2% but not sharply negative. The reductions equalled the increases and the -1.2% loss in NAV largely represents costs of running the trust.

A flat “fair value” evaluation hid growing revenues of +18% at the top 10, and +24% revenue growth overall (holdings’ total sales were £1.2bn up from £1bn), and an average 8.5% average EBITDA (of £103m) up from 7.8% in 2024.

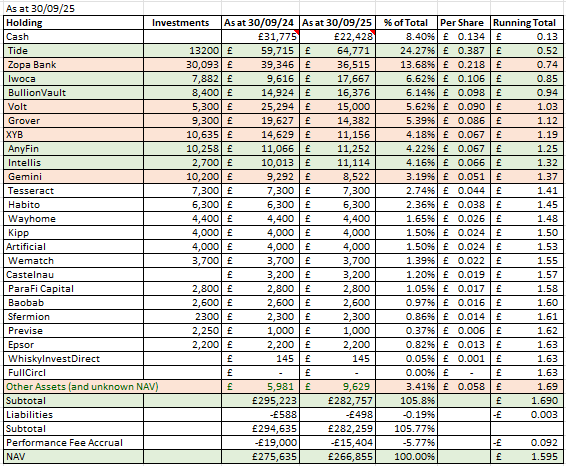

The persistent 45% discount is so severe that the book value of Cash + Tide + Zopa + Iwoca + Bullion Vault (the 4 largest holdings) exceeds the share price by 5p a share, with everything else thrown in for free.

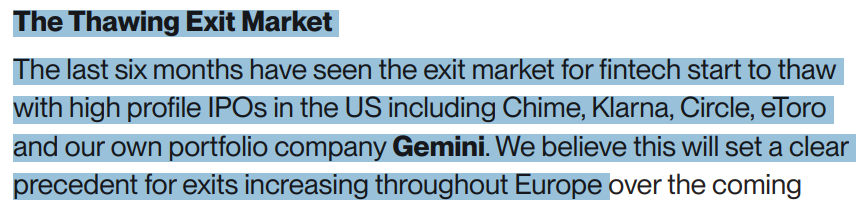

That further assumes book value of the top 4 holdings is THE extent of their value. Numerous Fintechs listed in 2025 including AUGM holding crypto fintech Gemini.

Let’s consider the progress at the top holdings:

#1 Tide 24.3% of NAV (43% of market cap)

In 2025 Unicorn-holding Tide grew its customers from 1m to 1.8m (after doubling in 2024) and Tide now has 0.8m businesses in the UK (a 14% market share of SMEs), 0.8m in India and 0.2m in France and Germany.

A follow on funding round in late 2025 of $120m valued Tide at $1.5bn. AUGM holds 5.4% worth £65m. The funds will be used to accelerate Agentic AI and Insurance Services.

AI at Tide

AI is central to Tide’s mission to save small business owners time and money. By combining predictive, generative, and agentic AI, Tide is building a platform that not only supports entrepreneurs but actively works on their behalf. Already, AI – and increasingly with agentic AI as a driver – is delivering tangible results in fraud prevention and managing member queries.

In 2026 and beyond, intelligent agents will complete full administrative workflows end-to-end – supporting members, but importantly will co-create with AI, or review and approve outcomes. We’ll do this while maintaining trust through robust governance, explainability, human oversight, and region-specific data controls.

With proprietary data, direct member connectivity, and a strong governance and regulatory framework, Tide is uniquely positioned to lead responsible AI adoption globally.

Tide Insurance Services

Insurance is the next phase of Tide’s expansion into much-needed business protection, specifically for SMEs. Tide launches Employers’ Liability, Public Liability, and Professional Indemnity insurance in the UK in 2026.

Engineering and Technology

Product engineering is the heart of Tide, and in the coming months our global Chief Data and Technology Officer will join the Executive team to work alongside Vinay Ramani, our Chief Product Officer. Through its One Platform prism, Ramani will oversee engineering and technology foundations across London, Sofia, Hyderabad, and Lithuania, driving strategy and delivery across AI & Data, Marketing, Member Operations, Payments and Business Services, and Credit & Financial Services.

The $120 million strategic investment led by TPG will accelerate international expansion. This includes scaling the Lithuania centre, where Tide plans to hire 60–70 additional, mainly backend, professionals over the next three years, to advance AI-driven product innovation.

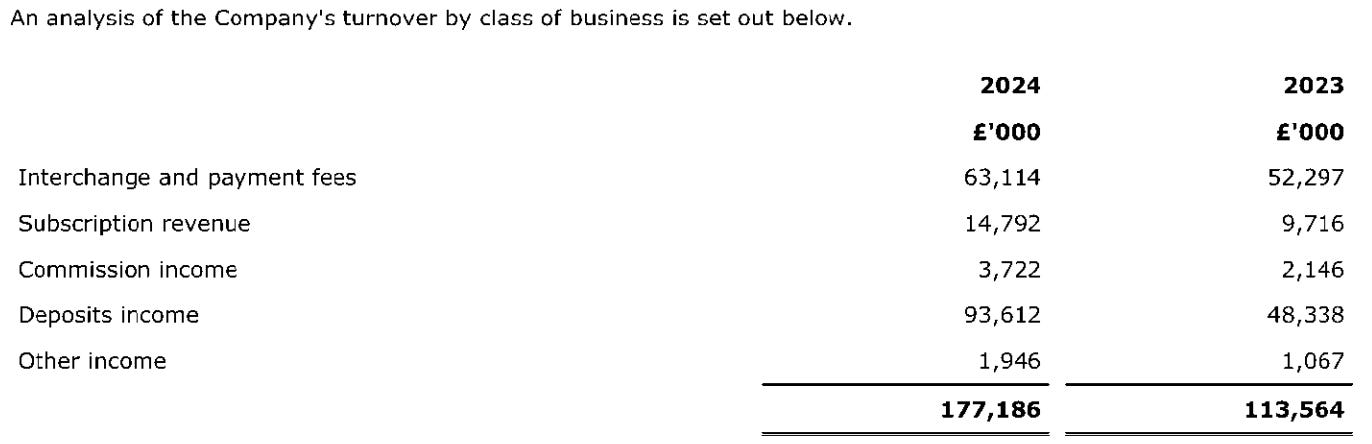

At a modest assumed £25/month turnover average that’s £240m turnover for the UK alone. Factor in Payroll at £12/month for the 1st 2 employees and £2 per employee/month thereafter, well that could quite easily double turnover to £0.48bn. But it appears only 50k are paying let’s say £25 per month since subscription revenue in 2024 was only £15m total. Up over 50% since 2023, and the accounts (since this is privately held) are released 9 months after the end of the period.

Nevertheless, growth in all forms of income mean the 2024 loss was -£14.4m reduced from -£34.1m. Is 2025 a break even year for Tide? With an 85% gross margin and overheads which grew by just -£22m between 2023 to 2024 it is entirely conceivable that Tide is profitable in 2025 and increasingly profitable in 2026.

Tide now has a ~14% market share of all UK micro (0-9 employee) businesses, with more than 800,000 customers. It bought Funding Options in November 2022, has FCA approval providing a credit offering to customers from over 120 lenders. It also provides a series of business tools for businesses too small to have a finance person (or team). Namely to provide card payments, direct debits, invoicing, accounts, or if your business needs are a bit more complex then out of the box integration to small business accounts (Sage Business Cloud Accounting, QB, Xero, and others). All the functionality is done from within a single app. It also bought Onfido and offers Payroll and HR services as part of that single app experience too. With insurance added in 2026 too.

2023 saw Tide launch in Delhi and Mumbai, India and in its last announcement it had more than 800,000 members. The market size in India is enormous. There are 63m micro businesses in India and many are run by millenials and Gen Xs. Tide also launched in France and in Germany where there are a further 2.19m micro businesses. So there’s plenty of runway ahead and the TAM has grown by 14 times by entering those geographies.

#2 ZOPA 21.8p a share (Plus Cash PlusTide is 74p total) i.e. 83% of the share price

Zopa launched investments this month targeting the 15m “reluctant investors” who prefer to hold cash in low yield accounts. Investors will be able to move money seamlessly between a cash ISA and stocks’n’shares ISA. (Nice idea).

Zopa has grown its customers to 1.6m from 1.4m a year ago and its current account is a best buy in the financial press. Its profits for 2025 are expected to nearly double to £60m.

An IPO in 2026 is not out of the question.

Zopa hit a £5bn milestone of customer deposits in 2025. It entered the Buy Now Pay Later space with its acquisition of DivideBuy boosting growth further. It funded that through a £220m funding round with AUGM participiation.

Zopa has a strategic tieup with JohnLewis Money to offer personal loan to the 23 million John Lewis and Waitrose customers. Considering that Zopa only has 1.3m customers, this partnership is very exciting and could drive growth. It also has a partnership with Octopus Energy and its 6.8m customers to offer “green energy loans”.

3# IWOCA (10.6p a share, so 85p total)

Iwoca is rumoured to be discussing its sale or IPO at £1bn or more. That would potentially be a 40% uplift to the £700m valuation today.

The “Triple Profit” Year: The headline news for IWOCA in 2025 was the release of their FY2024/25 accounts, which showed the company had entered a new league of financial stability:

Profit Tripled: Pre-tax profit jumped to £59.1 million, up from £21.7 million the previous year.

Revenue Surge: Revenue hit £234.1 million (a 64% YoY increase).

Lending Milestone: The company originated nearly £1 billion in new loans in a single year, bringing their cumulative lending since inception to over £4.5 billion.

Strategic Expansion into “Medium-Sized” Business

Traditionally a micro-lender, iwoca spent 2025 aggressively moving “upmarket” to fill the gap left by traditional banks like Barclays and HSBC:

The £1 Million Flexi-Loan: In late 2024/early 2025, iwoca doubled its maximum loan size to £1 million.

Construction Sector Push: In November 2025, iwoca committed to providing £1.5 billion in total funding to UK SMEs by the end of 2026, specifically earmarking £300 million for construction firms to support the UK’s housing targets.

Major Product Launches (2026)

The Business Credit Card: In January 2026, iwoca officially entered the payments space by launching its first dedicated business credit card. It is designed to compete with Amex by offering rewards specifically tailored to SME spending and integrated credit lines.

Embedded Lending Partnerships: They signed a major deal with Teya (a massive SME financial services platform) in August 2025, integrating their “Flexi-Loan” into Teya’s digital terminals, essentially turning every Teya card machine into a potential lending point

IWOCA has over 11,000 proof points

I fell off my chair when I saw iwoca had a 4.8 trustpilot score and over 11 thousand reviews.

These are the two latest glowing reviews.

Iwoca isn’t just about making working capital loans but it has evolved to provide an integrated means to offer buy now pay later to a B2B transaction.

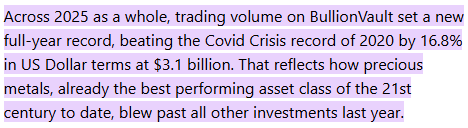

4# Bullion Vault (+9.8p so 94p … 4p more than today’s share price)

As you might imagine BV has had an incredible 2025. AUGM receives a dividend of circa 7% and this year it will likely be 10%+, worth £1.5m-£2m to AUGM.

#5 Volt (+9p)

Volt continues to refine its business model and focus. The company has streamlined its team, with a 25% cost reduction, while strengthening its compliance and risk capabilities, and adding licencing to support entry into regulated verticals. Operationally, Volt now processes 90% of traffic through its own “rails”, improving margins and reducing third-party dependency. The pipeline remains promising, with new partnerships including DaoPay and Paylado, as well as upcoming integrations with tier 1 merchants across multiple verticals.

#Non Top 10 Retail Book

I would stress that the remainder are not just rubbish either. For example many readers will have had dealings with Retail Book over the past year. A week ago changes to regulations and red tape should mean the IPO market and secondary market bursts back to life in the UK due to POATR in 2026. Very good news for UK shareholders.

The Public Offers and Admissions to Trading Regulations (POATRs) removes long-standing barriers and makes it easier for individuals to access a wider range of investment opportunities on equal terms as institutions.

With the removal of restrictive caps and simplified processes, more companies will be able to make their equity and debt fundraisings available to retail investors. This means greater choice and the ability to diversify your portfolio.

A wider set of opportunities provides the potential for wealth creation, given the higher long-term returns of investment versus savings products. From September 1986 until December 2024, the total return of the FTSE All-Share Index was almost four times that of the average savings return, although it’s important to note that past performance is not a reliable indicator of future results.

Commentators:

The market has dismissed Augmentum. Commentators have too. One commentator said “it lacks momentum”, and another complains of the “mark-to-myth” implying that the valuations are based on infrequent funding rounds. Of course that’s not factually true (at least not 100% of the time). A “wait and see” approach is preferred, to wait for an actual exit before buying in. It rather assumes you can achieve such perfect timing. Others point to the small declines in the NAV as the reason to steer clear, thereby missing the progress at its holdings.

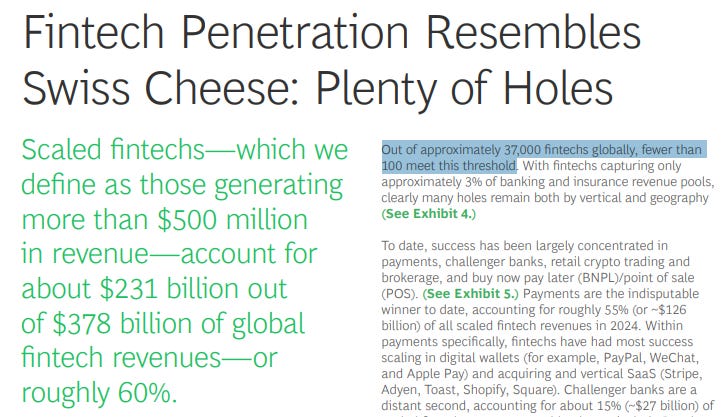

For example, this BCG report from May 2025 said of 37,000 fintechs globally, fewer than 100 generate more than $500m revenue.

AUGM has meaningful stakes in three of those “fewer than 100” fintechs

While the UK can be seen as a negative, it is one of the few places that has embraced open banking, and therefore there is an opportunity for UK challenger banks to lead the world in agentic AI. And of course AUGM is not solely focused on the UK either.

Conclusion

The market is treating AUGM like a speculative “growth-at-all-costs” fund, or a stodgy “going nowhere” fund whereas holdings were encouraged four years ago to pivot and a large part of the portfolio has matured into a profit engine. The top three are now significantly profitable - and growing profits.

Have profits come at the expense of growth? Not really. 20% growth at the top 10 is decent.

When the book value of the top 4 plus cash more than covers the market cap, it is quite hard to justify a zero valuation to 23 other holdings - particularly when you consider that is including a leading global platform for Silver, PGM and Gold Bullion, plus two listed holdings (Castelnau and Gemini)!

The share price also assumes AUGM has zero past track record of success. But that’s not the case. AUGM consistently achieved an average 33% uplift relative to its last reported NAV upon exit (e.g. Onfido, FullCircl).

Once the news breaks on the sale of Iwoca, or an IPO of Tide or Zopa it seems this will be a trigger to a rapid rerate at AUGM. Even indirect Fintech IPOs in 2026 for non-AUGM holdings like Monzo and Starling could provide a reference point to a rerate. That day I believe is soon.

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings including those held in a Fund might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

OB...very thorough and helpful report, as usual. It will be very interesting to get the portfolio update (again) at end of this week. I have taken a small position ahead of this as I agree with your analysis. I see JC has asked about WISE, which I am also invested in. Recent trading update confirmed that it is a fast growing company. My business associates all have WISE accounts for use on their travels. Market does not seem to understand the company (viewed as too expensive!!!), but I think this will change with its proposed US listing (see what happened to Indivior (INDV)).

Well played Oak Bloke, another great pick!