AVAP-orising the bear case

Considering Avation's FY2025 results at this OB25 for 25 idea

Dear reader

It was July 7th when I wrote The Oak Bloke is back in “Kerosene is nothing”. Ironic then that exactly 3 months later on October 7th I write “The Oak Bloke is Back”. Again.

**STOP PRESS - OB25 for 25 ideas hit a 56.6% gain ITD**

I’ll admit I’ve missed writing, although I’ve also enjoyed disconnecting from the world and submerging oneself into a foreign culture for a short time.

Back in July, Mr Scott in a free Friday article spoke of disliking AVAP because it had too much debt, and that it can only make money through disposals and it has a high cost of debt. Even behind his paywall, his and his team’s view on the FY25 results are silent at least relative to the search phrase “Avation” or “AVAP” at his substack. Since we can’t consider his present concerns, if any, let’s consider again Mr Scott’s past concerns.

Let consider too Stocko’s most recent view where they say that they have “lost faith in any near-term catalyst to reduce the discount to book value”. And that they now believe by reducing their view to Amber on AVAP they shall somehow cue a takeover of the stock.

#1 AVAP has “Too Much Debt”

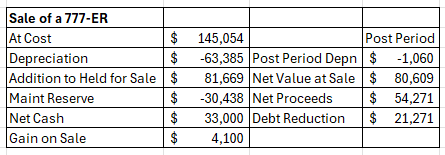

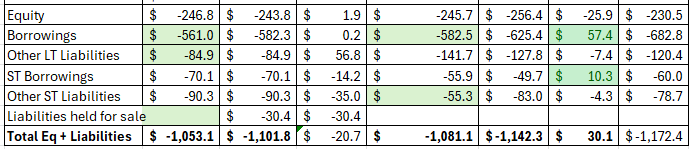

A -7% reduction in debt in FY25 is encouraging although -$604.2m remains a large number. The post-period sale of a 777 helps. That 777 was bought for $145m and this 8 year old aircraft had an est. $80.6m net value by 8th September 2025.

The various clues deduce a -$21.3m reduction in (warehouse) debt from $45m to $23.7m alongside $33m net cash, while a $4.1m gain determines there were $54.3m of proceeds which are also net of -$30.4m of maintenance reserves.

This is how the sale affects the balance sheet post period (I’ve not forecast for anyting post period other than the sale of the 777).

So AVAP’s debt, net of cash, restricted cash and receivables is now just -$456m

Include deposits and and derivative assets and the number drops to -$426m net debt.

Too much? You decide.

#2 The High Cost of Debt

Of course “too much” debt is also costing “too much” (an impact from Covid-era bail outs). This view ignores the potential for reduced cost of refinancing that debt too. It would have cost a vast amount to refinance this earlier than October 2025.

But that refinance is now possible from this month - October 2025. AVAP have wasted no time initiating that process. With the 5-year SOFR at 3.4% and 10-year at 3.5% and with a historic borrowing rate of +2.5% above SOFR then you are looking at a circa 6% refinance rate. Or lower if the improvement of ratings at Moody and Fitch from B2 to B1 count for anything too.

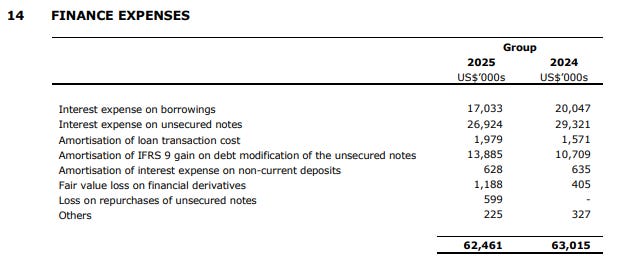

A $300m-$400m new bond issue has been announced. At a supposed 6% rate there would be a $18m-$24m per annum interest cost plus an amortisation on loan transaction cost (probably). Compare that with the current 8% - 9% costing $26.9m in FY25 shown below. That $26.9m cost is supplemented by $35.6m of other finance expenses.

Finance costs totalled -$62.5m in FY25. But that was then. In that cost is an unwind that has nearly unwound. There is a ~$6m remaining IFRS9 liability which would be extinguished in the event of a refinance. The point is in past years that that liability has been recognised as a Finance Expense and has included amortisation costs of -$13.9m per year. A refinance would not have a debt modification cost - only an arrangement and interest cost.

It’s likely that a floating rate SOFR+2.5% could be hedged so a FV loss on derivative may continue. So -$62.5m could become a -$24m interest -$2m arrangement -$1 derivative -$15 secured lending cost in FY26 = -$42m interest cost.

That’s a $20m per annum boost to profits per annum.

Remember, too, that’s based on raising a $400m unsecured bond (at 6%) so would give +$100m firepower too to expand the fleet. That would afford a further two 2nd hand narrow body aircraft.

Each could deliver $5.5m - $6m rental income so a 11%-12% lease return.

I noticed Stocko said when your average lease yield is 11.3% then paying 9% on your debt doesn’t leave much to pay your admin expenses and other costs. So a couple of things to say here: First the margin on a refinance moves from 2.3% to 5%-6% so that’s over double the prior margin. Second, that equation ignores the ~$250m of Shareholder’s equity at AVAP. i.e. you only pay 9% (or 6%) on the debt that supports assets IN ADDITION to shareholder’s equity.

#3 Only make money through disposals

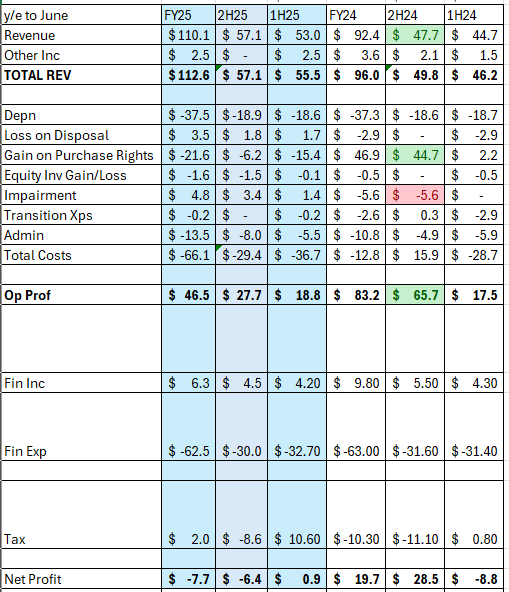

If you’re making a 48.5% operating profit I think it’s fair to say you’re making money on areas other than disposals. Don’t you think?

48.5% profit is $27.7m operating profit in 2H25 relative to $57.1m revenue in 2H25.

The 2H25 results show a 13.5% strengthening in margin to 48.5%. It’s fair to say there are extraordinary factors including recognition of maintenance reserves where there isn’t a linear approach to this being recognised to the P&L other than to repeat what I’ve written before - that on average (over 3.5 years) AVAP “overcharge” by about 4X and about $25m per year could go to the P&L (if it were steadily released).

They’ve never handed back maintenance reserve contributions although a learning experience for me was in relation to the Boeing 777-ER sale post period. The learning was that the maintenance reserve will follow the aircraft. Makes total sense really. While my instinct of $115m was actually pretty close but I hadn’t factored in the -$30.4m of accrued maintenance reserve liability so the net $80.6m. So net of this I was “out” by $4m vs my estimation.

#4 Lost Faith

This is a much more vague objection where you are speaking to sentiment. Market sentiment.

Maybe the way to best answer this is to think about why I’ve not lost faith. Why my faith is doubly enthused by the FY2025 results.

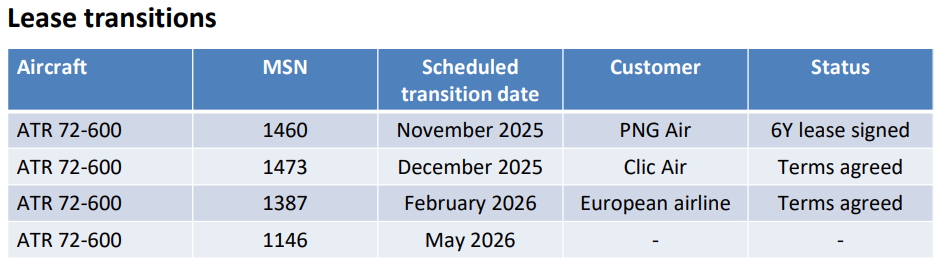

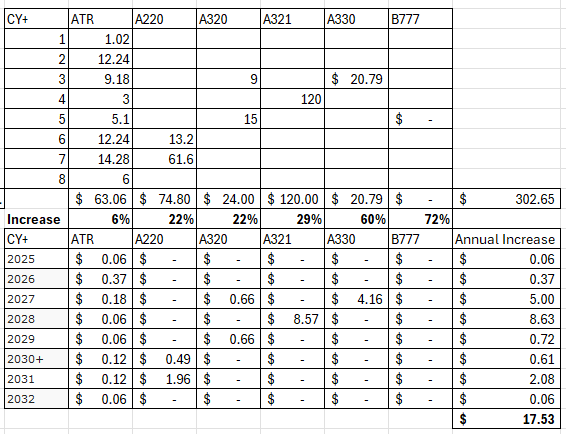

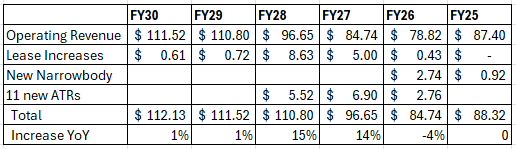

4.1 Growing Rental Income reflects a stronger lease market where demand outstrips supply (of lease aircraft). There are four lease renewals in the coming year so we should see further rises in rental income.

By applying the latest market lease rates to renewals further ahead we see a buoyant opportunity to potentially increase rentals.

It’s not just about increasing the lease rentals per aircraft either.

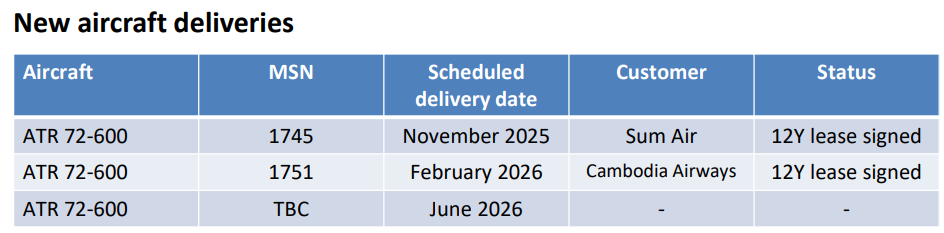

It’s about increasing the fleet too. As well as “flipping” two aircraft at a $3.5m premium to the Purchase Right value during FY25, AVAP are adding 3 ATRs to its fleet during the coming FY26 year including one next month.

4.2 Build up on Maintenance Reserve

There is a healthy “bank” of cash for the recognition of maintenance costs and a profit on top. The process of offsetting the maintenance of aircraft with additional margin appears to be working well.

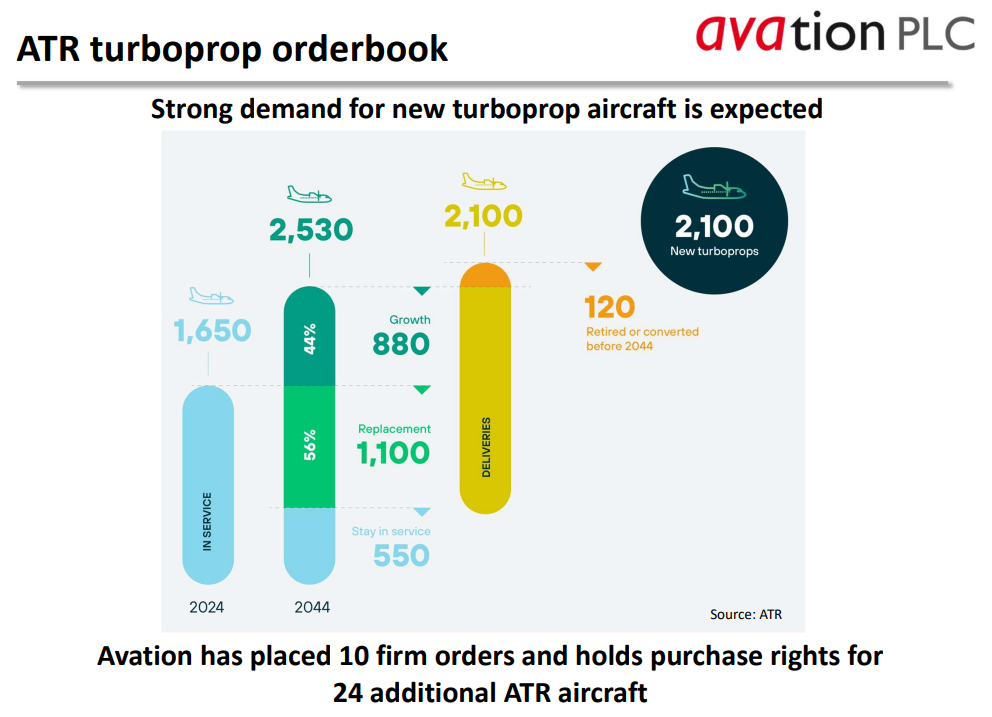

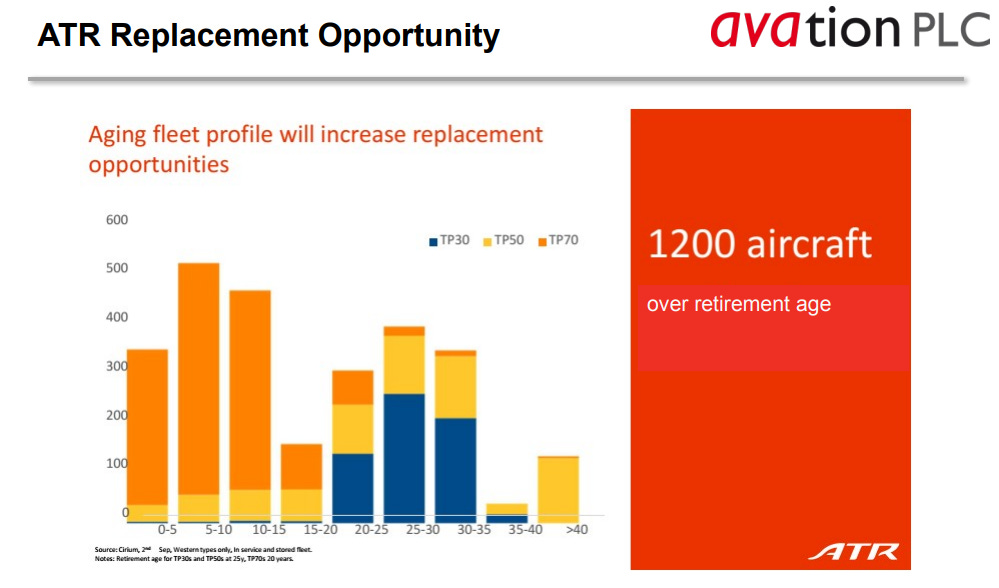

4.3 Better Engines; solid demand: ATR are a monopoly supplier to the Turboprop market. 2/3rds of all Turboprops need replacing and the market is growing by 50% too. The Purchase Rights have real value no matter what the discount rate “noise” might say. This macro is not changing any time soon where more and more people want to travel.

The market for replacement ATRs is vast - where the newer TP70 is hugely cheaper to run and to service. With 150 more aged 15-20 years and production per annum of 36 aircraft (180 total in 5 years) at current build rates it will take 40 years to clear the backlog. Then you spot that the 10-15 year old aircraft number about 450 so 3X as many. Regardless of what happens to the ATR in the USA (as it currently being discussed in aircraft circles) the existing Asian/African/European markets for ATR are vast. Adding the USA would add to the backlog. Canada has a vast fleet of Bombardier aircraft requiring replacement and the Bombardier executive jet option are a much more expensive option at 3X or 4X the cost of an ATR.

4.4 Lower Cost of Debt.

This has already been covered but a $20m+ interest cost benefit per annum even maintaining similar levels of indebtedness is NOWHERE in the price. I’m pleased that their focus is on restructuring the debt and look forward to a step change once bond renegotiations are concluded.

NB there are 5.7m warrants at 114.5p which might create ~8% dilution and raise ~£6.5m and which expire 31/10/26 so are also part of the hangover from Covid.

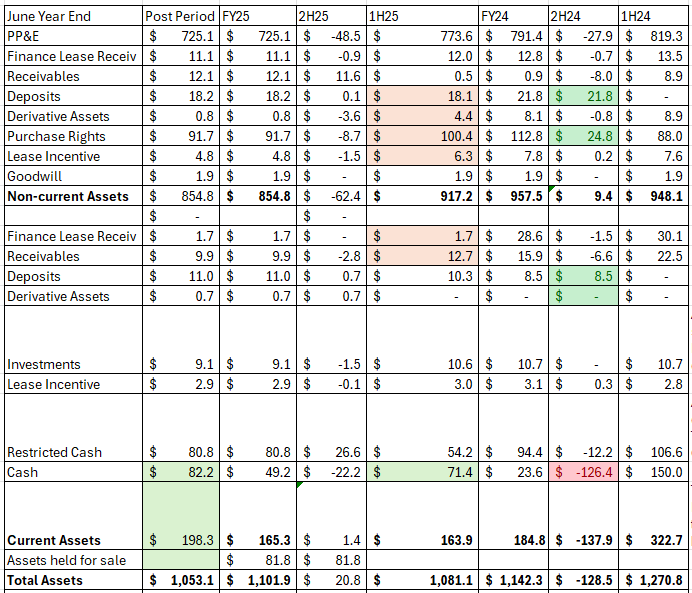

4.5 The current net present value of the AVAP fleet post sale of the 777-ER is $82m ahead of the current balance sheet, we are told. That puts the current (estimated) shareholder’s equity at $328.8m.

That equates to a 55.5% discount and £2.02 per share of discount to the net assets at today’s £1.62 per share. That’s a growing NAV too.

Factor in a $1.75m gain per aircraft (as was achieved in FY25 on two new ATRs) for the 34 aircraft that AVAP has rights to buy at a discount and that adds $60m to the NAV or a further 66p per share on top of the Purchase Rights.

That $1.75m gain per aircraft in FY2025 was on top of the $3.13m Purchase Rights per aircraft in 2024. So AVAP are buying ATRs at $4.88m below the 2024 market price of around $24m.

But AVAP lost money in FY25. What of that?

While the unwind of the discount is the way to account for the remaining value reducing the Purchase Rights for the remaining 34 aircraft so the -$21.6m reduction and “hit” to profit means each are worth $2.7m not $3.13m per aircraft the question you need to ask yourself is this: Would an ATR-72 600 sell for more or less in 2025 than in 2024? Even if the answer is “the same” then the gain on a disposal would be $2.18m instead of $1.75m.

In other words that loss in FY25 is no loss - actually. Not long term. Not when the world ASK (available seat kilometres) is going to more than double in the next 20 years.

Consider places like India where 300m ADDITIONAL Indians will access air travel by 2030. Look at their plans to expand airport access and operations.Vast.

Consider, too, that the ATR Evo is now only 3 years away from 1st service and that that aircraft is a game changer with its dramatically lower running costs and better eco credentials and compliance of noise and emissions. AVAP has the “right” to acquire those as part of its purchase rights too.

#5 Takeover

I don’t see that it is “inevitable” or that shareholders will be forced to accept a takeover. What nonsense.

It’s true that AVAP is a niche player and that there are larger competitors. So what? It’s further true that there are a limited number of opportunities to acquire second-hand aircraft. I’m encouraged that AVAP have a good track record in their buys and sells. They also have the inside track on the ATRs and this market alone can yield growing profits. 34 aircraft over the next 9 years is $646m of purchases or $71.8m per year. That’s before any further Purchase Rights being granted, or opportunities to get involved with other new aircraft. Plenty to go after.

In my opinion investors in this OB25 for 25 idea could profit over the long term. This idea is up 2.5% ITD. At 162p a share it appears to offer great value once you get behind and understand the numbers.

Regards

The Oak Bloke

Disclaimers:

This is not advice - you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Disclosures:

I have no commercial connection nor receive any remuneration from any company I write about. Beware of those who do. I may (and do) write about stocks I hold and believe in i.e. I am talking my own book. I ask readers who enjoy and profit from my work to support Emmaus. Many already have.

Hi OB. Great article, with your usual thorough look at the numbers. It will be interesting to see the coupon they end up paying when they refi their existing 8.25% notes. Although credit market conditions are very receptive to new issues right now, the benchmark in the US dollar high yield market for a B2 rated unsecured bond is between 6.75 to 7%.

Welcome back Mr Oak. SQZ - wow, THX wow….