BELL-weather

Trading update from Belluscura & comparing POC Suppliers

Dear reader,

Interesting to see an update today from the OB’s 2024 ideas from laggard Belluscura titled “Strong Sales Momentum & Updated Trading Outlook”

I see Belluscura now boast 80 DMEs stocking their products across the US.

Interesting too to see the chattersphere burbling that:

Belluscura is the poster child for over-promising under-delivering management. Their product is not particularly unique and can be obtained from numerous other sources, yet management have tried to create the impression that their product is ground-breaking and unique. The reality is that this is a low margin commodity product that will never generate adequate profits to justify being listing.

Leaving aside the poor grammar and concentrating on the claims, let’s consider the truth of this. It’s true that there are other oxygen devices. Some of these are from huge competitors. But numerous? No. This market is supplied by an oligopoly of several large names with 2 upstarts. Let’s consider the most credible large name first. Philips. That’s a name one or two of you may have heard of. Discov-R at $3,295 is about 10% cheaper than this Philips but does BELL have to rely on price leadership to compete?

No, BELL’s product is lighter as well as cheaper, with a much longer battery life. 8 Pulse modes not 6.

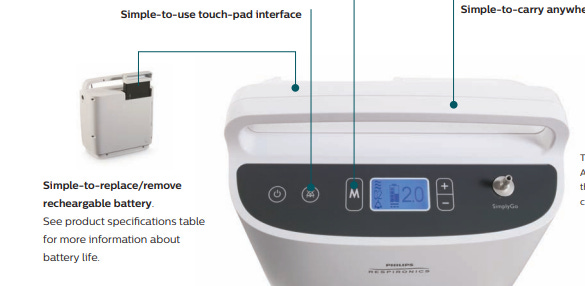

Besides BELL has an App. (Philips does not). It tracks your breath rate, oxygen usage (hours used), pulse volume, battery life and alarm history all directly from POC unit.

This is next generation compared to the Philips “simple-to-use touch-pad interface” from the last century.

Belluscura is the only oxygen concentrator to win both the 2021 Gold and 2023 Silver awards for its products at Medtrade. It presented at Medtrade 2024 and was well received by attendees.

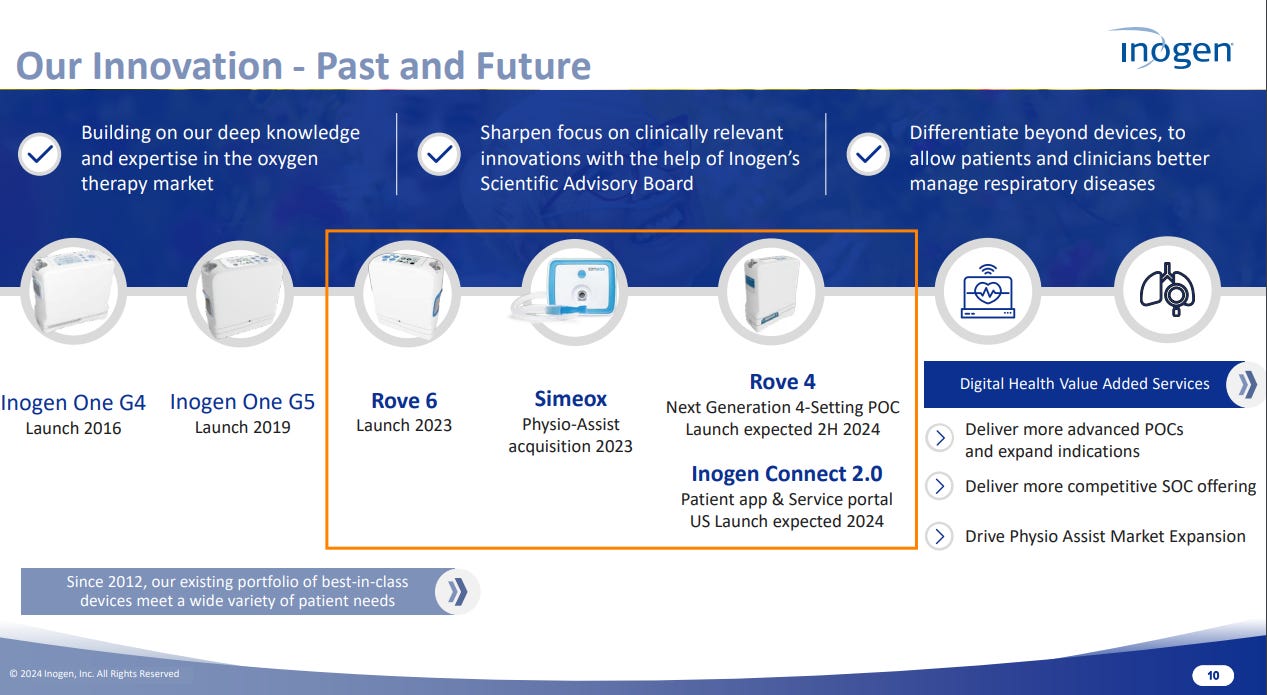

Another competitor is US listed Inogen. An upstart like Belluscura, but Inogen has a much larger market cap.

Pricing of their products is quite a bit higher (about 15% higher) but their latest products are either not released to the US market yet or are brand new to the market. On the face of it, Inogen’s products have a similar battery life and weight to BELL’s. But Inogen have no app.

The DISCOV-R is slightly heavier (1.5lbs) than Inogen’s G5, however, it generates 50% more oxygen and, most importantly, the DISCOV-R produces both pulse dose oxygen and continuous flow oxygen.

This means DISCOV-R can serve both the portable and stationary oxygen markets and treat patients that cannot utilise pulse dose oxygen. This has been referred to in previous presentations in that service providers are excited that it meets two codes. I would say it kills two birds with one stone but it’s probably not the right analogy to be using. Especially given Philips just paid out $1.1bn to settle a US lawsuit for faulty breathing devices which actually DID KILL people and damage their lungs through defective filters sadly. UK folks using Philips breathing devices have had no such compensation. But they are angry.

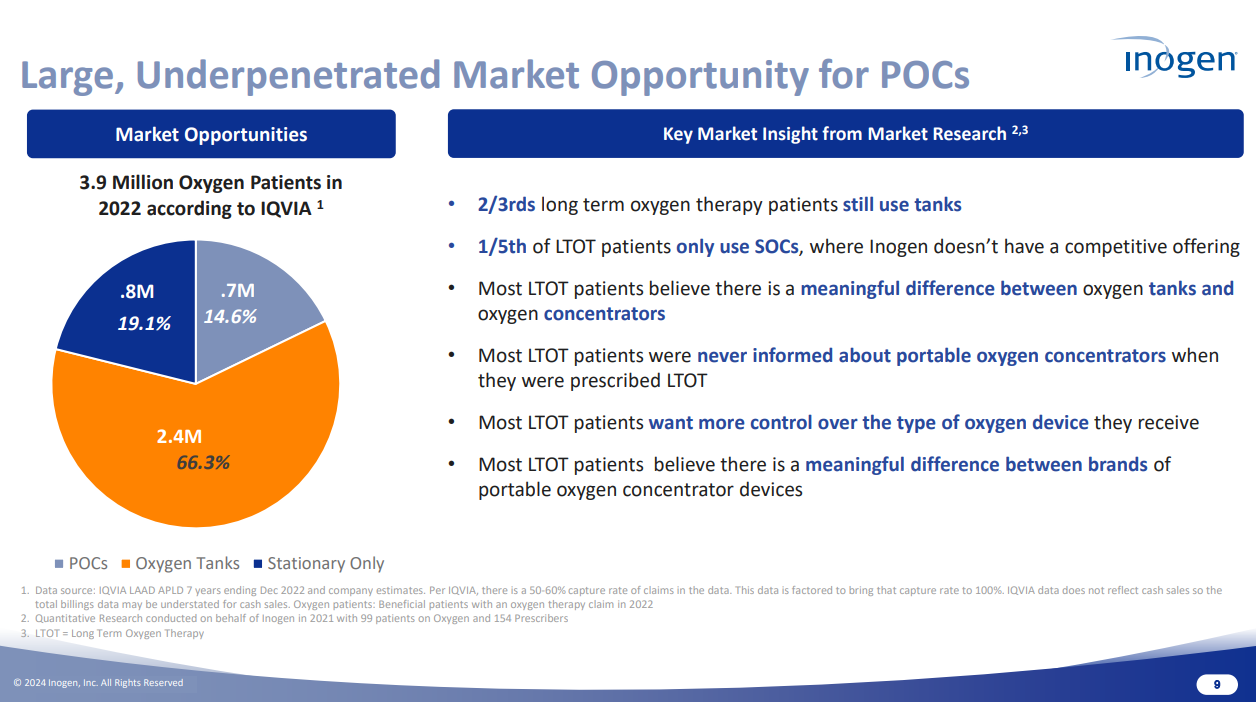

Inogen’s corporate presentation speaks to a “large, underpenetrated opportunity” i.e. the fact that there’s a somewhat competitive product to BELL really doesn’t matter. The market size is colossal and with 3.2m US patients using tanks at current collective production volumes it would take well over a decade to replace existing concentrators, let alone to service new sufferers.

Ingoen have no app but speak to “digital health value added services” which are coming in the future.

INGN has a market cap of £228m vs BELL’s £18.5m.

INGN lost -$101m in 2023, -$85.5m in 2022 and -$5.3m in 2021. Sales revenue shrank 2021-2023, as did gross profit shrink between 2021 to 2023. In 1H24 it’s lost a further -$21.5m and cash has gone from $125.5m at year end to $98m at June 30th.

So while this is a larger competitor to BELL it is not without its own issues (including survival) and has enough cash to last about another 12 months at current burn rates.

Can Inogen’s new products turnaround its fortunes? Analysts are not hopeful and have an aggregate price target of $10 i.e. at minus 20% and see further losses of around $42m-$46.30 a year in 2024 and in 2025.

The grass is not always greener they say.

Competition

So yes there are competitors and yes there are some of those beginning to catch up on BELL but it seems to me that the statement BELL sell a “low margin commodity product” is not true, and is at best ignorant. But people make these assertions all the time and it is either the case you let the doubt nibble away or you go on a quest to find the evidence to prove or disprove it. Or you can read the Oak Bloke.

So Philip’s product is tangibly inferior but they have a strong commercial footprint.

Inogen is comparable to some extent, but trails behind, and at a 40% gross margin at higher prices suffers a large disadvantage of costs versus Belluscura, who enjoy estimated 70% gross margins at a lower price point. For me, of all the “Top Trump” features lower cost of production has got to be one of the most important features.

The point is, too, there is a large addressable market and BELL are partly focused on the USA where there are 3.9m where at least 80% are using an outdated means of treatment, probably at higher cost.

Plus BELL have a large footprint into the Chinese and SE Asian market (which Inogen do not according to their web site)

BELL update (Everything in Italics is direct from the RNS)

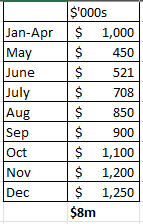

"Belluscura achieved record sales for the month of July with revenues of $708,000. This follows the previous monthly high set in June of $521,000. The Company expects strong sales to continue with the broader market acceptance of the X-PLOR® and the upcoming full release of its new patented DISCOV-R™ device.”

NB: This sales number for July is ahead of my profit model for 3Q24, which bodes well.

DISCOV-R

“Demand for the new DISCOV-R™ portable oxygen concentrator, which was introduced to the US market via a soft launch in June 2024, has been strong, with every unit manufactured in June and July being sold.

The full commercial launch of the DISCOV-R™ remains planned for the middle of Q4.”

Updated Trading Outlook

“As the Group approaches the full commercial launch of the DISCOV-R™ in two months' time, the Board has re-assessed the trading outlook for the final months of 2024.

2 months time means end of October.

The Board anticipates that revenue for FY24 will be approximately $8 to $10 million (2023: $825,409) depending on timing of the full commercial launch of the DISCOV-R. and that the Company will be EBITDA positive for Q1 FY25.”

The Company expects annualised run rate revenue of $14 million to $16 million by the end of year.

The revenue profile which fits both $8m 2024 sales and $14m run rate at the end of the year is this. (I’m using the low end of estimates).

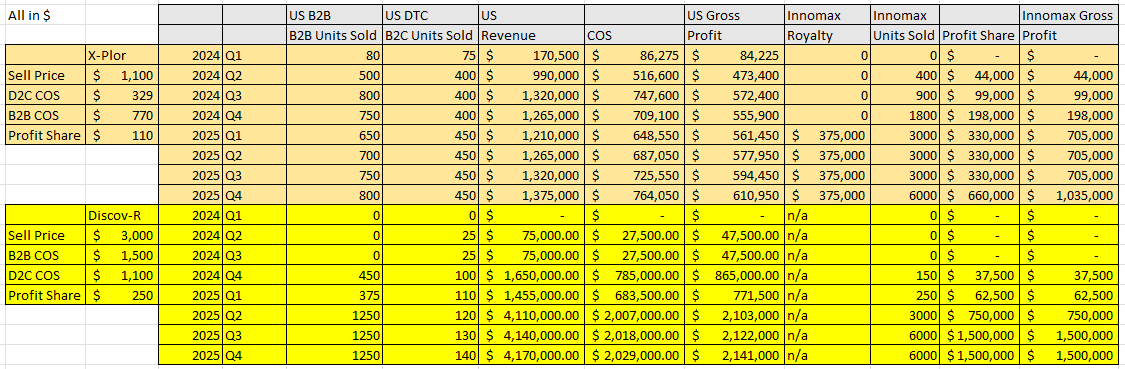

The Innomax royalty agreement adds $1m-$2m to this from 2025 (I’ve modelled $1.5m)

The sales model which then fits the revenue looks like this. At fairly modest growth (slower than current growth) model delivers a $24m turnover for 2025 and EBITDA of $16.4m (and Net Profit of $4m)

If you think my numbers are “far too high” they are probably far too low. By comparison, Inogen’s sale of unit numbers are 150k per year and I am forecasting 9,350 units (a mix of X-Plor and Discov-R) will be sold by BELL in 2025 and that’s both in the US and via Innomax in Asia. Bear in mind initial orders were 6,500 when they announced Discov-R. So 9,350 is almost certainly too low and too conservative.

Sales by Product, by Channel, by Continent, by Quarter

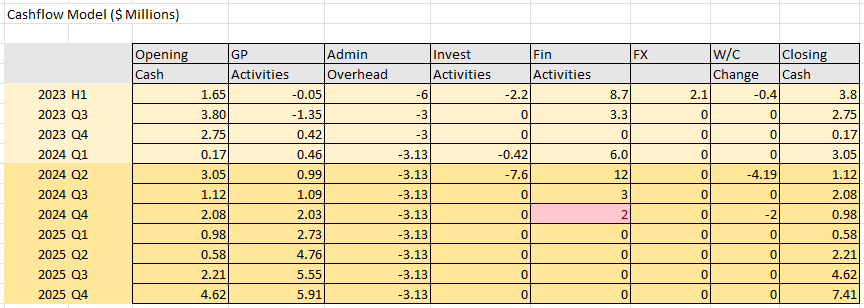

Liquidity

As reported in the 2023 Annual Report to support expansion plans for future development the Group regularly reviews its financing arrangements and cash flows to ensure there is sufficient funding in place for working capital.

Feeding in the sales data into my cash model we see any increase to working capital requires an increase to funding. I’m working on the basis that $2m provides additional working capital to fund a 50% run rate expansion in 2025, which within 6 months can be repaid through cash generation.

In my last update I said there was everything to play for in the 2nd half and that remains true.

If my model is correct and bear in mind my model fits the parameters of the RNS. Sales of $8m in 2024 and $24m in 2025, with an EBITDA of $3m and $16.4m (net profit $4m) then BELL is valued at a P/E of 8.4 while Inogen have a P/E of -9 (using 1H24’s numbers).

If we use an Adjusted EBITDA instead (a P/EBITDA if you will), and using a highly selective 2Q24 number for Inogen of $1,258,000 (its only period of positive EBITDA you see) for Inogen annualised that’s $5m EBITDA but on a $300m market cap that’s a P/EBITDA of 60 versus BELL’s $33.3m market cap and $3m 2024 EBITDA is a P/EBITDA of 11, dropping to 2 in FY2025.

So BELL is somewhere between 5X and 30X cheaper than its closest rival Inogen, although you are also comparing to a larger competitor with a bigger cash pile but larger cash burn and higher production costs.

-

When the detractors have to resort to inventing stories about the (lack of) uniqueness or (lack of) capability of BELL’s products which don’t stand up to research then you probably know you’ve hit upon hidden value.

The growing sales evidences that these products meet a need. The pre-orders and the deal with Innomax is significant. Think about it. Would a company like Innomax commit to a $27.5m royalty plus the build out of manufacturing without serious amounts of due diligence? Innomax are a subsidiary of FoxConn and these are a multi billion dollar firm which are famous for manufacturing iPhones in China.

All in all, today’s chunky price rise doesn’t even start to capture the value of the opportunity here. Could some further dilution occur? Hopefully not, but perhaps. How much dilution? Possibly a few million more is needed. $2m in my model. That’s about 6%-10% of today’s market cap. Or will we see some trade finance step in from one or more of the large chains who’re keen to get selling Discov-R? I’d like to think that debt or finance is more likely at this advanced stage.

We are now tantalisingly close to commerical success, and in the coming months with everything to play for BELL-ies can feel pleased about today’s update. The knock on effect of the TMTA acquisition knocked on to the plans and the sales forecasts and people are pointing to that for a reason for this share’s “continued failure”.

But today’s news of continued sales growth is a real positive and the continued upwards trajectory shows the level of risk is in steady decline.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".