BETR LINV-ing ahead?

A comparison of the UK Lend Invest and the US Better Home and Finance

Dear reader,

Today’s picture imagines Mortgage advisors from the UK and US.

Uncle Sam and his hat, along with Uncle Derek who’s using Auntie Mabel’s hat by the looks of things.

-

Today I’m looking to compare:

US-listed BETR (as at 30/06/24) - Net Assets $44m; Market Cap $283.5m

UK-listed LINV (as at 31/03/24) - Net Assets £59.3m; Market Cap £39.5m

Both are technology plays on the mortgage market, speeding up the process using “proprietary tools” and both have evolved from holding capital and using that for mortgages “on balance sheet” to instead working with finance partners and acting as a broker. BETR calls this “warehousing” and LINV “syndication”. BETR appear to have a broader “buy”, “refi” (same or higher remortgage), “cash out” (lower remortgage), and “HELOC” (equity release). They also offer “Title and Settlement” (conveyancing) and “Insurance”. They also over in the UK offer Buy to Let Mortgages. LINV meanwhile focus solely on residential, Buy-to-Let and short-term (Bridge) mortgages.

-

Analysis of BETR

Overview

BETR say in their 2023 annual report “We were formed in 2014, commenced operation in April 2015, and have experienced net losses and negative cash flows from operations for the majority of our operating history….. 2020 was the only year that we achieved an operating profit, but that year was followed with a net loss of $301.1 million for the year ended December 31, 2021 and a net loss of $888.8 million for the year ended December 31, 2022, as well as a net loss of $536.4 million for the year ended December 31, 2023.”

BETR go on to say Financial performance deteriorated due to:

• persistent elevated interest rates, which have the effect of reducing industry mortgage origination volume, increasing competition for customers, and reducing revenue (although I notice at a much improved sales margin 2.03% compared to 0.89%)

• continued investments in the business (including investments to expand product offerings);

• reputational damage associated with negative media coverage following a series of workforce reductions that began in December 2021 and litigation, including litigation with a former employee - which has since been settled in BETR’s favour.

• outsized costs relative to our Funded Loan Volume and revenue resulting from changes in the macroeconomic environment

-

Moving to 1Q24 and 2Q24 the broader approach of BETR doesn’t appear better, at least for now.

Mortgage platform revenue and expense lost money in 2022, 2023, 1Q24 and 2Q24 even at a gross profit level.

So did “Title and Settlement” for BETR in 2022 and 2023 and 1Q24. The volume worryingly reduces in Q2 by about a quarter (from Q1) and is around 70% lower than 2022. Not even achieving a gross profit raises some serious questions.

On a positive, BETR say in their provisional 2Q24 report (which came out 7th August):

Funded loan volume of $962 million, an increase of 45% from Q1’24, across 2,995 Total Loans

Purchase loan volume grew 50% quarter-over-quarter and comprised 83% of Funded loan volume; HELOC loan volume (which includes home equity lines of credit and closed-end second lien loans) grew 76% quarter-over-quarter and comprised 9% of Funded loan volume; and refinance loan volume declined 5% quarter-over-quarter and comprised the remainder of Funded loan volume

D2C business grew 86% quarter-over-quarter and comprised 70% of Funded loan volume, with B2B comprising the remainder

But funded loans were $11bn in 2022 so while $962m for 2Q24 is “up” it is actually down by 60% too. These “amazing” growth percentages of progress are partial reversions to previous normal levels such as in 2022, and the presentation makes it appear very different than the long-term picture tells. I would describe it as sneaky.

BETR appears to be supported by $514m of Convertible Loans from Softbank. But with only $44m of net equity and a quarterly loss of $42m (in 2Q24) this is months away from turning negative. The convertible carries just a 1% annual interest cost but comes due in 2028. At today’s $0.41 share price if Softbank elected to do so they would receive 1.25bn shares which with 3.3bn shares existing would own 27% of BETR. If the share price between now and 2028 were to drop to say $0.10 then Softbank’s ownership would be 60%.

Positives

Tinman - the software platform appears to be a valuable piece of IP and know how and attracting investment and a SPAC during 2023 during a time of investment drought is impressive in itself. The Smart Money is pointing to this being a great investment.

There is circa $500m liquidity which gives some breathing room

BETR Conclusion

Falling rates could lead to improved levels of mortgages it’s true. Is US real estate certainly on the up? That remains quite unclear.

If growth and market share showed signs of improvement then this could be exciting. As it is, I haven’t found any evidence to that. So the potential upside isn’t clear.

There is liquidity of some $500m too. But, for me, the risks here are substantial. Zooming back out to 2014 there’s been a decade of losses 9 years out of 10. Spectacular losses too.

Softbank’s “support” is also a threat. If you are surrendering 27% - 60% of the company (or more or less depending on the future share price) then Softbank have rights over potential a half of your future upside and assets.

I would also question the sheer breadth of the model. Trying to be a mortgage broker a real estate (conveyancer), an insurer, a surveyor (via Better Inspect), and to do so in both the US and UK all seems like over reach. Observing that these services are being sold at a loss there are alarm bells ringing too.

The UK operation is 20% of the whole business and mainly represented via Birmingham Bank. There is no disclosure or discussion of how well that is or isn’t performing. The UK web site states it is focused on Buy to Let lending and ISA savings (at around 2.5% the rates are ok but not market leading), but doesn’t speak to TinMan or approvals in a day so one has to think the UK are running on a legacy system not Tinman - but this isn’t clear.

I would love to have applied for both a Tinman and LendInvest mortgage to “battle test” both systems but it wasn’t apparent how to with Tinman - whereas the LendInvest below gives you a good idea of the platform itself.

My conclusion would be to steer clear or at least wait until there’s a clearer and more positive picture (of both BETR and the US macro)

LendInvest

LendInvest plc (AIM: LINV), a UK mortgage platform, reported its full-year results ending March 31, 2024.

Key financials include:

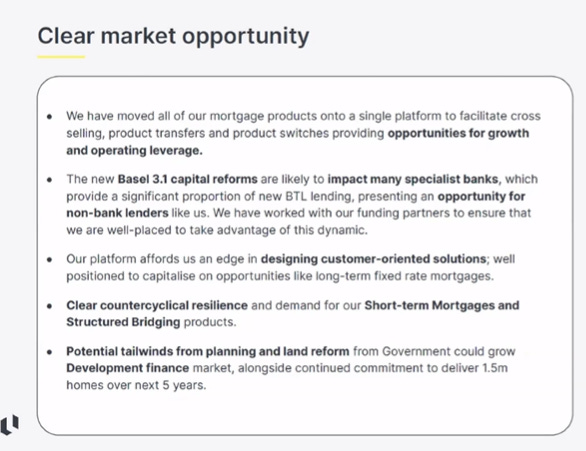

Platform Assets under Management (AuM) grew 8% to £2.8bn, driven by a 13% increase in Buy-to-Let (BTL) and bridge mortgages.

Funds under Management (FuM) increased 14% to £4.1bn.

New lending decreased by 11% to £0.89bn.

Net Fee Income rose by 42% to £15.9m, while Net Operating Income declined by 57% to £23.5m, reflecting the move to third party “off balance sheet” loans.

Debt reduced by £645m (56%) consequently, and the leverage ratio reduced by 39%.

Total operating expenses increased by 26% to £50.8m.

Adjusted EBITDA shifted from £14.3m profit to a £15.1m loss.

PBT loss -£27.3m, and PAT -£20.1m.

Strategic highlights include launching a new Mortgages Portal, diversifying funding sources, and reducing debt by 56%. CEO Rod Lockhart emphasised a return to profitability in FY2025.

LINV is also a story of losses but only for the past year - prior to this it paid a high dividend and was profitable. We also see an improvement in 2H24 vs 1H24 where losses reduce 52% half to half.

Future growth in off balance sheet lending is a focus. LINV is profitable at a gross profit level and there are a number of one off factors in FY2024 through derivatives and hedge accounting (£4m), derecognition losses (£1.0m) professional costs (£1.1m), and a 15% reduction of headcount with a (£1.6m) restructure cost leading to cutting admin expenses by over £4m a year going forwards. That’s £11.7m of non-repeating costs. If you further accept that impairments of £8.4m were exceptional then the FY2024 underlying loss shrinks considerably to sub -£6m. 2H24 impairments were -£1.3m for example.

Moreover, if the collapse of Credit Suisse had not occurred perhaps the -£10.6m loss on the £250m portfolio would have not occurred.

Maybe, just maybe, FY2024 could have delivered a profit.

Getting into the weeds of the reasons for the -£27.3m loss makes me feel better about the FY2024 performance.

But what of the future?

2025-2027 Forecast

Based on a AuM growing by similar amounts over each of the coming three years, and also that 1Q25 lending (to 30th June 2024) is 20% higher than the average for FY2024, along with the interest rate cut in August.

LINV’s historic focus was BTL and bridge lending while in FY2024 it entered specialist residential mortgages for mortgages for people with multiple incomes, self employed, variable income etc

The growing UK Rental Market

Hatchett Harry once famously said “Well if ya go’ i’, ya go’ i’”. Renters, meanwhile, need i’! 227,000 more rental properties a year to be precise, say USwitch. So as those with weak hands exit, remaining landlords getting larger and more “professional” but also new entrants are joining. Judging by the ongoing popularity of books like Rich Dad, Poor Dad and enduring popularity of programmes like Home under the Hammer I’d say there’s plenty of BTL Landlords joining. Landlords require BTL mortgages and Bridging Loans.

With a new government I do not see this demand drying up or declining. Planning and land reform could grow development finance; along the commitment to build 1.5m new homes over 5 years.

Value of Technology

There have been several Strategic Achievements at LINV over the past year:

1. Launch of the LendInvest Mortgages Portal: A significant operational leap forward, providing seamless access to our entire product range and facilitating easier transitions for brokers and clients.

2. New Product Transfer Process: Introduced a streamlined process allowing brokers to easily switch products at maturity, enhancing customer retention and satisfaction.

3. Expansion of Funding Partnerships: BNP Paribas was added to the financing syndicate.

The current market cap considers zero value to the value of the IP. When you contrast LINV with for example Cushon which sold to Natwest on a £169m valuation for what arguably is a far simpler platform. Would the likes of Santander, Lloyds or another snap up LendInvest at some point? Banks and BS’s differ the co-op says 30 mins, Natwest reckon 10, Lloyds 20, some saying 30 minutes, Barclays 15 but David Wilson Homes suggests you need 3-6 hours to complete a mortage application vs LINV’s 5 minutes.

The productivity of the platform for brokers, enabling them to process 100 applications per month per underwriter must surely be an attraction. There are 5,593 UK mortgage brokers so LINV’s network of 4,400 is nearly 80% coverage of the UK. Of course a broker might work with multiple platforms and also it also depends on customers choosing LINV however, very often a digital marketplace is an ecosystem where more brokers attracts more buyers in a virtuous (or vicious) circle.

Combining this productivity with the ability to transfer and manage multiple products and evolving products give a smoother customer journey.

£60m has been spent over 15 years on the LINV platform and up to 12 changes are made (on average) per day.

Conclusion

To conclude, when considering home or away, there is US style and UK substance, there is US broad and UK focus, there’s US loss and UK profit

Even between two businesses engaged in very similar endeavours, I find there’s a clear winner with much less risk, with brighter prospects, yet is priced at a small fraction and at a discount to both its assets and forecast forward Price Earnings.

I take my hat off to Uncle Derek, which considering Mabel’s montrosity might prove a God send to what I conclude is my favourite Uncle. (Sorry Uncle Sam)

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

Thank you for that analysis - first class! It really focused well on the most important financial metrics as well as what can be reasonably predicted.

LINV ends up looking like an amazing bargain and BETR is really a lot of style with lots of rust under the hood.