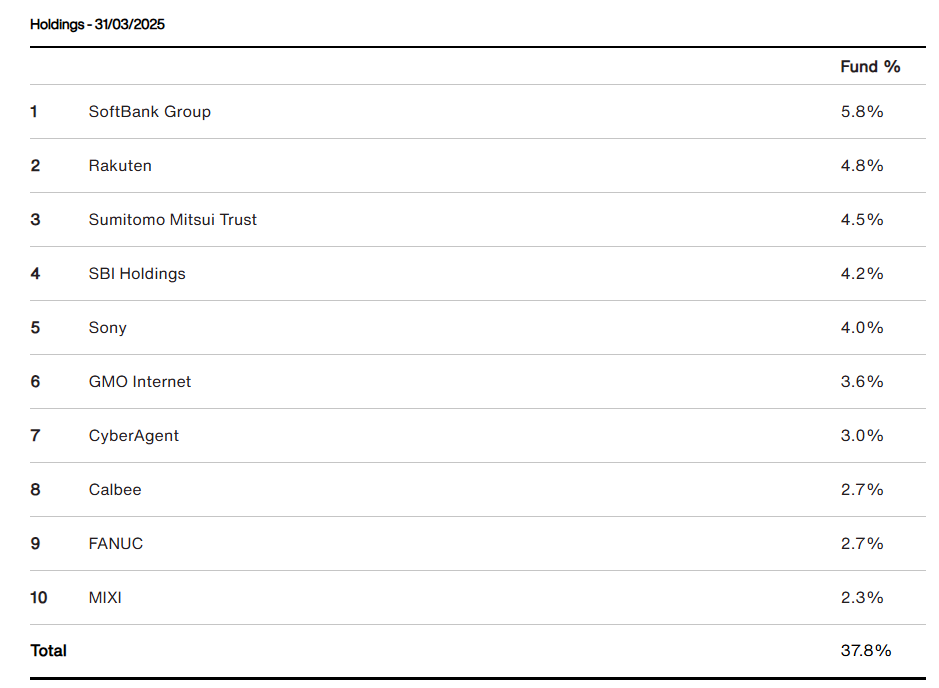

BGFD by the tariffs?

Some shocks for some holdings - Japan is on sale

Dear reader,

How did the big brother to Japanese Smaller, the Japanese Trust ticker BGFD do?

The March update tells us:

On the face you’d think nothing to see here.

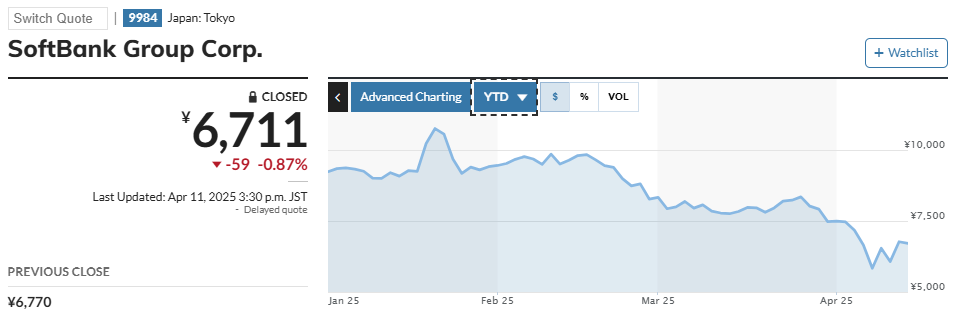

Digging in we see vast drops of some holdings. Softbank down a third.

Much of this drop is due to a drop in its (listed) Arm Holding

Failing to meet High Expectations

Arm is closely associated with the AI boom. Despite strong quarterly results in Q3 2025 (ended December 31, 2024) with revenue up 19% to $983 million and EPS of $0.39 (beating estimates), the company’s guidance has underwhelmed. For fiscal Q4 2025, Arm its forecast only aligned with and didn’t exceed analyst estimates of $1.22 billion. Earlier in 2024 (e.g., fiscal Q1 and Q4), similar “in-line” guidance led to sell-offs, as investors expected more aggressive growth given Arm’s high valuation (forward P/E around 71.1 times, far above the semiconductor industry’s 33.6).

Arm’s business model—licensing chip designs and earning royalties—yields steady but not explosive growth, unlike chipmakers like Nvidia. Arm is reliant on slower-growing markets like smartphones (99% market share but flat growth). The market’s reaction seems like a correction to unrealistic expectations.

2. SoftBank’s Leverage

Arm is majority-owned (90%) by SoftBank, which has been on a borrowing spree to fund AI and tech investments, including a $500 billion US “Stargate Project” and a $40 billion OpenAI stake announced in March 2025. Some market observers speculate that SoftBank’s high leverage could pressure a sell off of Arm’s stock if margins were called. Besides Arm’s low free float (10%) amplifies volatility, as small share movements cause outsized price swings. However, no evidence suggests SoftBank is liquidating Arm shares, so this factor may be more perceptual than substantive.

3. Market and Sector Dynamics

The semiconductor sector faced headwinds in early 2025, with Arm’s head of IR noting a slowdown in chip sales for networking equipment, particularly 5G infrastructure, due to paused rollouts. This impacts Arm’s royalty revenue, as fewer devices shipped means lower income. The 5G pause is temporary, but it highlights Arm’s sensitivity to end-market demand. Arm’s long-term growth is in cloud (v9 adoption) and automotive (energy-efficient chips).

4. Impact of Trump Administration Policies

The Trump administration’s tax cuts and tariffs, announced in 2025, have mixed implications for Arm. The corporate tax rate cut from 21% to 20% (or 15% for US manufacturers) and TCJA extensions could benefit Arm’s US operations and clients like Apple, potentially increasing demand for Arm-based chips. The “no tax on tips” and “no tax on overtime” policies boost consumer spending, supporting smartphone and IoT device sales. However, proposed tariffs—10% on all imports, 60% on Chinese goods—raise concerns. Arm’s supply chain, reliant on Asian manufacturing (e.g., TSMC in Taiwan), could face higher costs, squeezing margins for clients and slowing chip shipments, which directly hit Arm’s royalties.

5. Legal and Competitive Risks

Arm faced a setback in December 2024, losing a Delaware court case against Qualcomm over royalty rates, which could limit its ability to raise prices for v9 technology. This may have dented confidence in Arm’s pricing power, a key growth driver. Competition from RISC-V, an open-source architecture, also looms, though Arm’s entrenched ecosystem (99% smartphone share) mitigates this near-term.

Other SoftBank News:

March 2025: SoftBank Corp. announced the development of a Large Telecom Model (LTM) to advance cellular network operations, leveraging AI for efficiency and reliability. This aligns with their broader AI-driven infrastructure push.

March 2025: Demonstrated a “Remote Autonomous Driving Support System” integrated with Traffic AI, aimed at enhancing safety in autonomous vehicles. This reflects SoftBank’s investment in 5G and AI convergence.

March 2025: Reported increased mobile payment usage among employees due to smooth transaction and bill-splitting features via PayPay, reinforcing its fintech ecosystem.

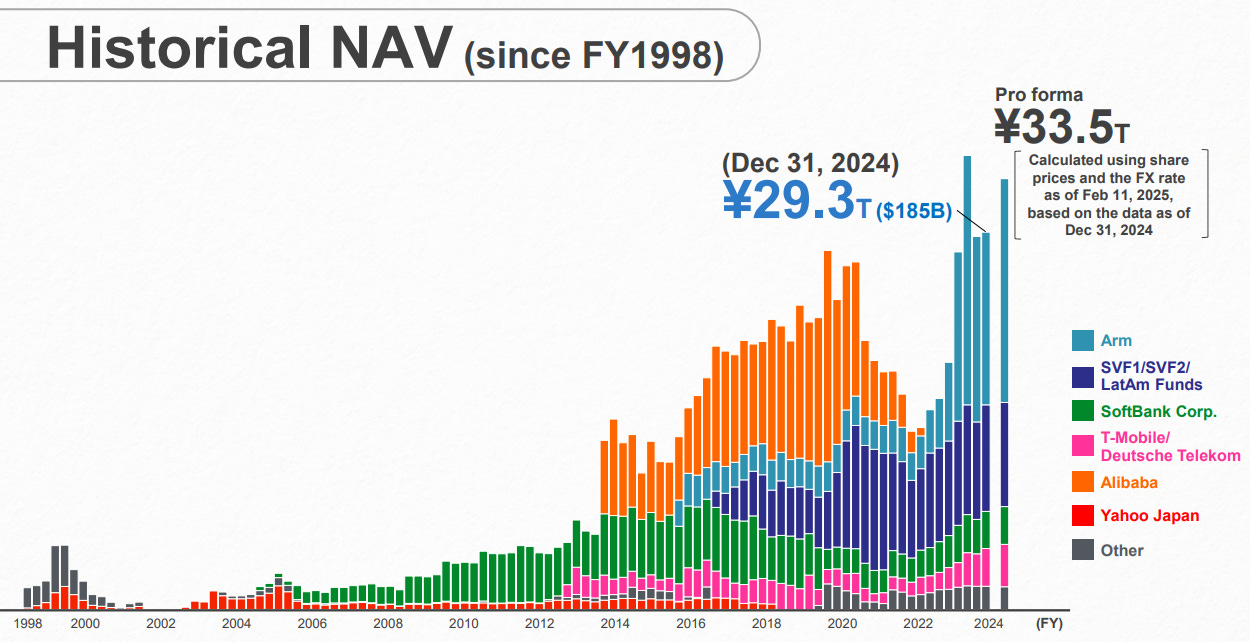

General Context: SoftBank Group’s $500 billion investment in the US “Stargate Project” with OpenAI and Oracle (January 2025) continues to dominate its narrative, with a follow-on $40 billion OpenAI investment announced on 31 March 2025 ($30 billion net after syndication). This has bolstered its AI focus but drawn scrutiny for high debt levels (Loan-to-Value managed below 25%).

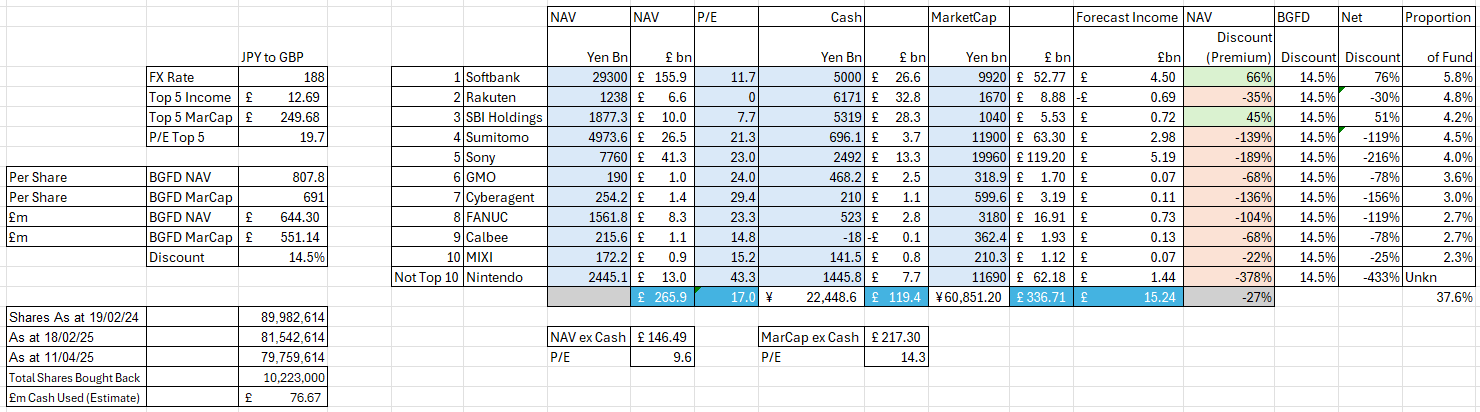

The Discount to NAV is now an extraordinary 66% (as at 11/04/25 and based on the 31/12/24 NAV), and including BGFD’s 14.5% discount gets you to a vast 76% discount to the look through NAV.

Softbank trades on a P/E of 11.7X based on an annualisation of its 9m25 profits.

#2 Rakuten

Down a sixth since my article “BGFD Wives Part 1”

Rakuten foresaw even stronger growth in 2025 vs 2024. 26.7% of UK retail sales are online; in Japan it’s just 8.9% - but growing. Rakuten are approximately the “Amazon/Klarna/Netflix/Revolut” of Japan.

#3 SBI Holdings

Down a quarter since my article.

On a P/E of 7.7X and a 45% discount to NAV it looks incredibly cheap.

SBI or Shinsei Bank is an internet-focused offering online brokerage, internet banking, online life insurance and venture capital. To a Brit that might not sound unusual - in Japan it is.

It is closely linked to cryptocurrency so recent falls in price and popularity might be weighing on it…. but 25% down seems excessive.

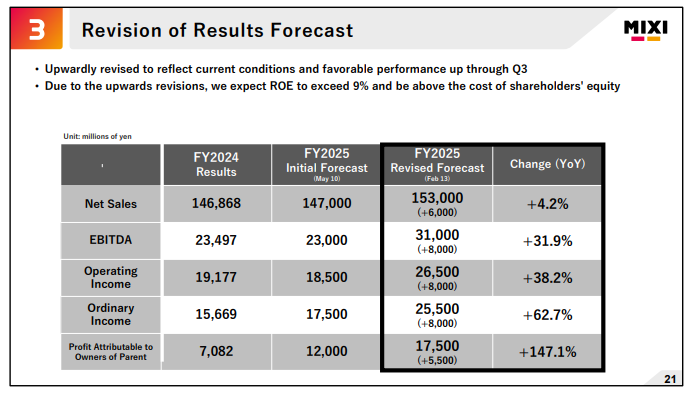

#10 MIXI

Wanna bet you’ll like Mixi?

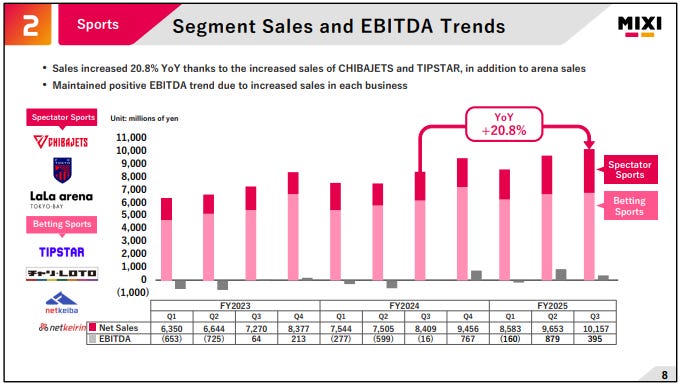

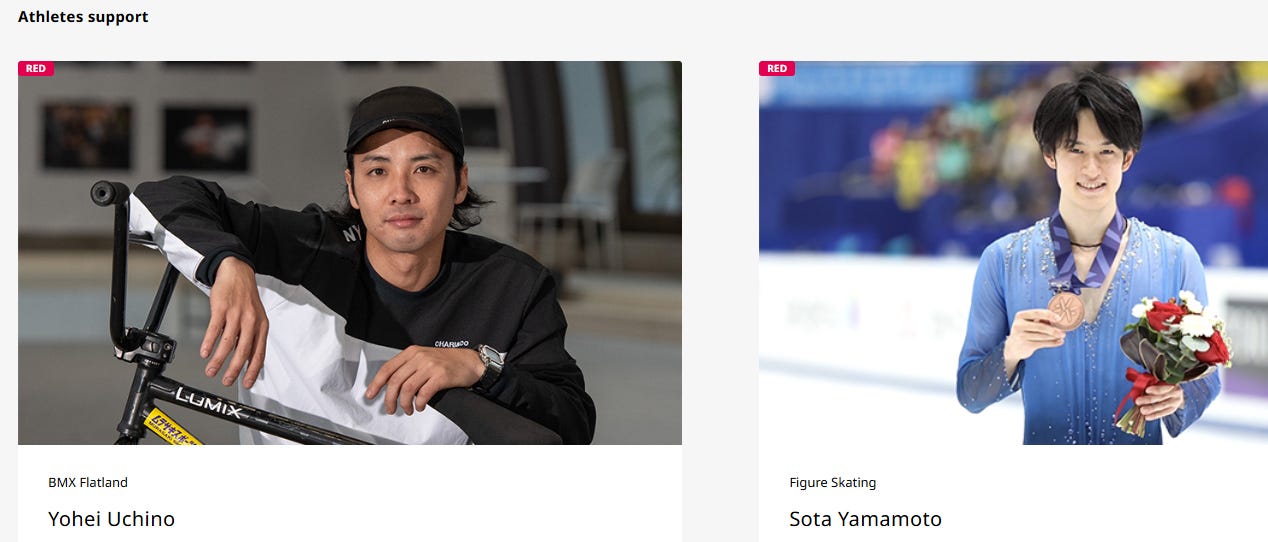

Its Sports betting segment covers Horse Racing, Basketball, Baseball, Football, Auto Race and bizarrely BMX racing and Figure Skating.

It also appears to sell tickets and merch, for a Basketball Team and a Football Club.

Mixi sponsors these two well-known faces in those two sports.

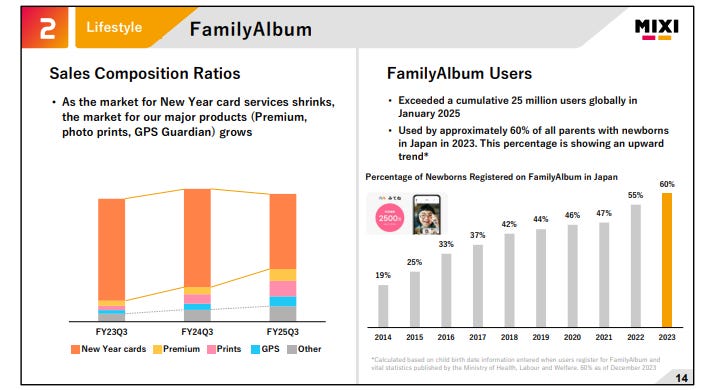

Its second “Lifestyle” segment is a “Moonpig” type business called “Family Album” which the majority of Japanese use (25m users) - it’s “the thing to do”.

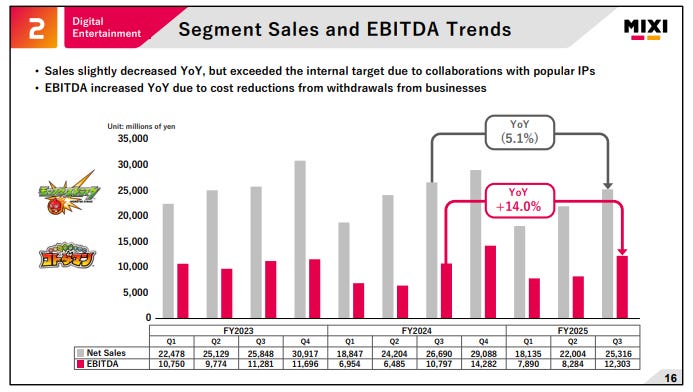

Its third segment is digital entertainment and this is a gaming emporium where friends can play games together killing monsters, care for virtual pets and other stuff…. 63 million users. Japanese plus versions were introduced for Taiwan, Hongkong and Macau.

As you’d expect Mixi are leveraging the IP to offer a diverse media mix, including merchandise, in-person events, video and anime distribution, and collaborations with other companies' IPs and across industries.

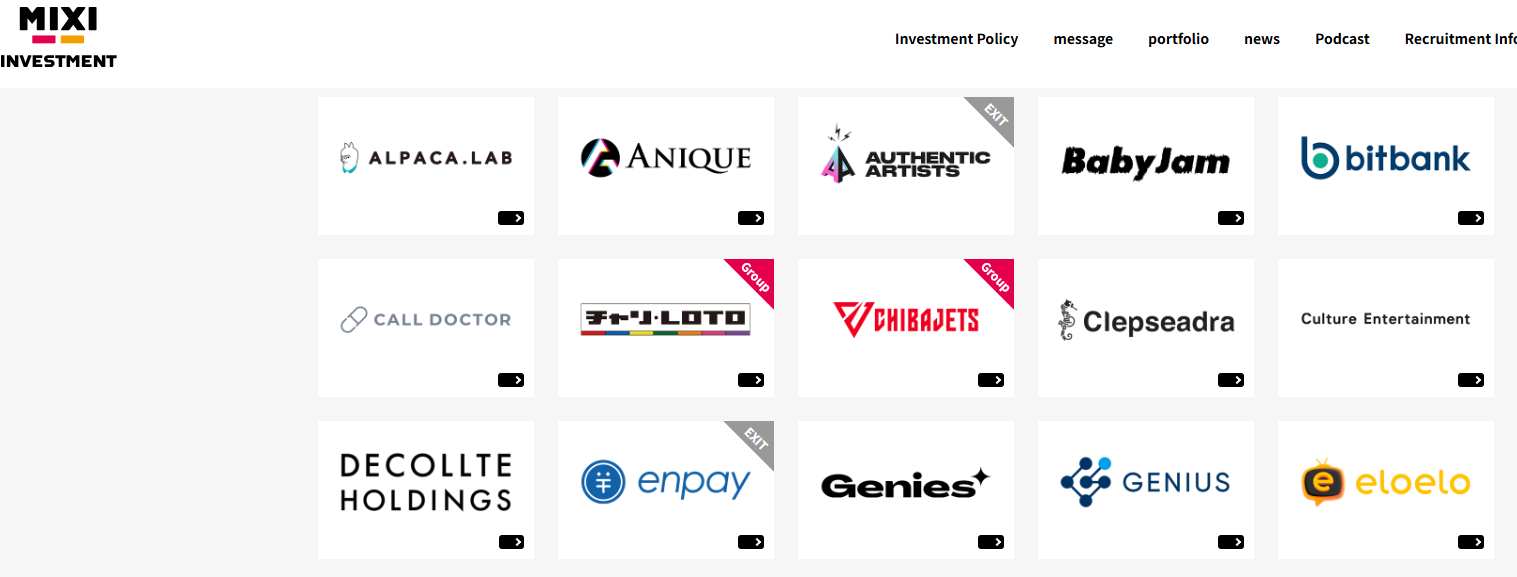

Investment Segment

Mixi bizarrely is also an investment broker in the TSE Growth Market - kind of like AIM. Decollte Holdings for example is a wedding dress business turning over £40m a year according to their IR material.

Particularly liked this Mount Fuji cloaked in clouds wedding pic.

So Mixi is kind of a “Ticketmaster” cum “William Hill” cum “Peel Hunt” cum “Moonpig” cum “Electronic Arts” cum “Prepaid Card business”. I’m sure you agree that that is a highly unusual combination. A real “Mixi”.

Yes, but does it generate profits?

Yes is the short answer. £93m is the FY25 forecast profit, on a £1.12bn market cap so a 12.4X P/E. It has a strong history of buy backs too.

Conclusion

Based on the MarCap the top 5 deliver a 19.7X P/E. If you strip out the cash from the marcap at the top 10 you then get a 14.3X P/E. Based on the underlying NAV minus cash you get to a P/E of 9.6X. For world-class companies 14.3X is a bargain, in my opinion.

Then consider the growth they are exhibiting, and sectors they cover spanning Financial Services, Tech, Robotics and Consumer Goods.

Then consider the Trust had 90m shares 14 months ago and today it’s less than 80m. The buy backs are boosting the NAV.

Of course the likes of Sony, Fanuc, Nintendo are going to be caught up in Lib day tariffs to some extent.

Softbank is investing $100bn in the USA (and was the poster child for Trump in my prior article) so I believe the CEO could pick up the phone to Trump - exclusions will almost certainly be made.

Other holdings like Rakuten, SBI, Sumitomo, GMO, Cyberagent and MIXI have limited exposure, if any, to tariffs.

Japan is likely to emerge a winner from the US/China spat since it is a close ally to the USA and a bulwark in Asia, while maintains a close economic relationship with China - that got closer this week.

PS Inflation finally arrived to McDonald’s Japan. 650 yen finally rises to 680 yen. Meanwhile the FX rate has fallen a little from 195 to 188 yen to the GBP.

This means a Japanese Big Mac Meal is £3.62. The UK Big Mac Meal is £8.49

That gives you a further reason why buying Japanese makes a lot of sense. Japanese interest rates are likely to rise to counter inflation (including the rising cost of Big Macs) while cuts are likely to the UK rate. Any strengthening of the yen would deliver a positive FX rerate for the GBP value of Japanese holdings too.

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

BGFD are generally blue chip holdings but risk exists everywhere. And as I always say Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Oh well, I bought JPJP which has fared a little worse than BGFD or JFJ over the last month.

Can Japan raise interest rates? They have massive debts, 263% of GDP.