BMN 'eck!

Did Craig Coltman just pull off a coup for Bushveld?

First of all congratulations to Craig Coltman and all South Africans on a stunning world cup rugby win! Proper lekker bekig my men. A great source of optimism for South Africa.

Meanwhile today’s news from BMN has left people a little confused. The detail is a bit complicated it’s true. Here’s a cut and paste which I see others have done.

But what does it all mean?

Well you could buy the whole of BMN today for £22m. So with today’s dilution the BEE stand to gain £2.54m worth of BMN shares at today’s prices. (22/1.13 = £19.46m). Or BMN share holders lose 0.17p for each share - if BMN didn’t gain anything.

But that’s not true. BMN has gained something. Quite a lot actually.

$24.7m extra to be precise.

Bushveld Vametco Holdings has $94,998,000 of net assets. 26% of that $95 were owned by BEE. But now to be owned by BMN. So this is in addition to BMN’s $78,041,000 existing net assets as at 30/06/23. (Or BMN’s $29m tangible net assets if you’d like to argue the intangibles shouldn’t be included - although the intangibles are very tangible and in fact SPR’s purchase recently proved they were) and as I argued in my recent article 5 drivers to value)

$24.7m of extra assets! What?! That’s nearly the entire value of BMN according to the stock maket. And what’s the market reaction to this amazing news?

Not so lekker man!

If what I’m saying is true, and BEE just agreed to give away £24.7m then why on earth would they do this?

I suspect today’s “simplification” is part of the Orion deal. Why lend money to improve an asset when the asset holder owns 74% of that asset? The obvious question would be when will the other 26% holder stump up their share of Kiln 2 etc? No! Hence the simplication. Also it’s true 26% of nothing is nothing and a smaller percent of something is something…. in other words they believe. Perhaps they believe they have no other choice.

Or may they MORE than believe. Do they know?

Do they know the Orion deal WILL happen. Why do I think this? I find it very hard to believe the BEE folks would have agreed this deal today without KNOWING the terms of the Orion/SPR deal will be. Otherwise why would any sane person agree to such a deal - to willingly be part of a wipe out of ordinary shareholders (do you notice they don’t even get preference shares)?

Whilst a lot has been said about how Orion are “inevitably” going to shaft BMN, Orion live in a competitive world too. Whilst they want and expect their pound of flesh, alternative sources of funds do exist. In my article Value Trap up you snap I argued that Orion won’t want to push too hard in case they kill the Golden Goose. That still stands. But they’re not the only ones. Think about SPR’s position. If Orion’s funding collapses then the whole Vanchem deal is also in doubt - that fabulous Iron Ore Slaaaaaaag we’ve heard so much about. If pushed too hard and BMN goes bust, maybe SPR would be able to snap up 100% of Vanchem - or maybe not. I think SPR also has BIG reasons for the deal to go ahead and to keep BMN as a going concern.

Now will Orion (and SPR) still offer 6p a share? I don’t know. But stranger things have happened…… they just did over at Kavango last week. Share price for KAV is 0.6p but the investor said we’ll do the deal at 1p as agreed.

Even if Orion/SPR play hard ball and the worst happens.… In my article Specially pleasing Result I showed how the path to liquidity lay ahead like this. And maybe the BEE have done the maths and are calculating the same as the Oak Bloke. That the Orion/SPR deal leaves shareholders with a manageable debt profile and a vastly more profitable business.

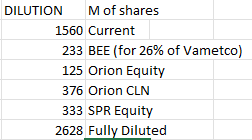

So assuming a 1.5p (today’s market price) Orion/SPR deal, and the convertible is fully converted then we are talking $30m of shares (for SPR and Orion) which is leads to ($30m/1.5p) = 163bn shares being added to the current 176.3bn = 339.3bn

Against $78m (net assets) + $24.7m (26% Vametco net assets) + $30m (Equity) = $132.7m

$132.7m/2.628bn = Results in a $0.047 or 3.7p a share NET ASSETS - so 50% over today’s share price.

I appreciate some people may still see this as being “wiped out” and their average buy price is above 3.7p.

But 3.7p/share of net assets in an increasingly profitable venture, with manageable debt (and debt profile) doesn’t mean the value is 3.7p. Once you can value BMN on an EV/EBITDA basis or P/E basis then we are back to a 7-8p valuation - without any crazy vanadium prices.

By the way, are you sharp eyed? Did you spot the other key feature in Note 32 of the 2022 accounts - and is also part of today’s news?????….

Did you spot that the 26% share of Vametco also means that BMN net earnings increase by $5.6m a year (based on 2022 net earnings - so $5,564,000 in a difficult year is a minimum)!! On a PE of 10 ($56m), today’s deal is accretive to profit (as the RNS tells us) but I don’t think the RNS explains why and how much.

Think about the BEE and do they believe - or do they know? Not just the asset value but the profits too. Giving up an asset generating $5.6m a year only happens if you know… or at least strongly belive.

That’s a strong signal to us long-suffering outsiders - a signal coming straight from the insiders.

Usual caveats apply.

Good luck, stay lekker.

Oak