3p conversion price for both Orion’s convertible as well as the shares for SPR

So the Refinance has been agreed. The sale of Vanchem and mokopane and consolidation of Vametco.

So referring to my prior posts the terms are more advantageous than the 1.5p scenario but not as generous as the 6p scenario either. Even so, I estimate net assets at 5.15p a share following dilution.

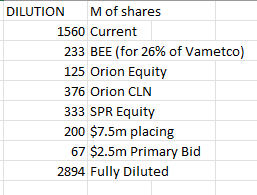

Shares on a fully diluted basis go from 1.56bn to 2.89bn - assuming all CLNs are converted, and all placings happen in full. I’ve said 3p for the Primary Bid raise although one wonders whether people will buy shares at 3p when the open market price is 2.5p today.

On a cash flow basis BMN now appears to no longer face a cliff edge:

$53.1m of funds where today’s RNS sets out $43.5m use of funds. So put another way selling CellCube is optional.

There’s lots to feel happy about and the doomsayers once again are confounded and Craig Coltman yet again delivers.

Guidance for 2024 up 15% too.

The stars are aligning….