Bosched? Or couldn't Ceres less?

What does the Bosch news mean for CWR?

Dear reader

“Everyone has a plan, until they get punched in the face” Tyson

“What do tigers dream of when they take their little tiger snooze? Do they dream of mauling zebras, or Halle Berry in her Catwoman suit? Don't you worry your pretty striped head, we're gonna get you back to Tyson and your cozy tiger bed. And then we're gonna find our best friend Doug, and then we're gonna give him a best friend hug. Doug, Doug, oh, Doug, Dougie, Dougie, Doug, Doug! But if he's been murdered by crystal meth tweakers” A song by Dr Stu (he’s not a Doctor he’s a Dentist) Price, The Hangover

On the 20th Feb Ceres Power (CWR) announced that Bobby Bosch has decided to go another way. As a CWR shareholder I was curious to find out more. The market has reacted with a more than -50% fall of CWR. That’s quite a reaction.

Does that make CWR a bargain? Or is it Bosched?

Part 1 - What Bosch Say

Bosch’s home page features the below interesting picture featuring these characters. It took me a good few seconds to work it out. I finally realised these are characters interacting with Bosch appliances. All I can say is watch out Skeletor, HeMan has nailed Murtaugh’s technique from the Lethal Weapon series.

After some time looking I find Bosch describe their efforts in green hydrogen research here.

It says “Bosch initially focused on developing a 1.25 MW PEM electrolysis stack. At the same time, a “smart electrolysis module” is being developed. It combines the PEM electrolysis stack with a control unit, power electronics and sensors.

Bosch will work with partners during development, initially supplying the PEM electrolysis stack and, downstream, the smart electrolysis module to manufacturers of large-scale hydrogen production facilities and industrial service providers. The results of Bosch's electrolysis research have paved the way for this market entry and continue to play a role in the development and production of the components.”

It then goes on to describe its work with SOFC and its partner Ceres! That’s still on the Bosch Global website as at 3rd March 2025 11 days after it ended that relationship. Whoopsie.

The Press Release

I then find their press release.

Stuttgart, Germany – Bosch is realigning its operations and investments relating to stationary hydrogen technologies. In the future, the supplier of technology will focus more on technologies for hydrogen production and the supply of electrolysis components, above all PEM (proton-exchange membrane) electrolysis stacks. In light of this, its operations relating to the industrialisation and preparation for production of decentralised power-supply systems based on solid-oxide fuel cells (SOFC) will be discontinued. Work to explore the possibilities of solid-oxide technology will continue within the company’s corporate research unit. The company also remains highly committed to mobile applications of H2 in fuel cells and hydrogen engines.

OB - Part of this badly worded press release is Bosch say they will focus on hydrogen production. Both SOEC and PEM fuel cells are both forms of hydrogen production! What I believe they attempt to mean is focus on hydrogen production for mobility. SOEC requires heat so it is impractical to have “oven-temperature” facilities at every fuel station. A PEM Fuel Cell doesn’t require heat so is suitable for refuelling Hydrogen Fuel Cell vehicle (FCEVs). But more than this Bosch are interested in the Tier 1 component supply into FCEVs - which after all is its largest traditional market.

Over the past ten years, Bosch has worked with partners to develop solid-oxide fuel-cell technology for decentralized power-supply systems. These achieved a high level of technical maturity, which was demonstrated in more than 100 pilot systems. Recently, however, the market has not developed as expected. On the one hand, the market is especially demanding higher-output systems with carbon capture, and this makes the conditions for economical operation significantly tougher. On the other hand, the conversion of hydrogen into electricity is not yet being given the necessary priority in Europe, and especially in Germany. This means that further engineering effort will be required in the years ahead, and this will significantly reduce commercial viability.

OB - Again “the market” is referred to vaguely. What they mean is the STATIONARY MARKET. Stationary is providing fuel for things that don’t move e.g. A Factory as opposed to things that move i.e. the MOBILITY MARKET. Trucks, Cars and so on, the components that go into them and the facilities that refuel them..

“For us as a company, volatile market developments mean that we have to consolidate our efforts and focus our portfolio. We see hydrogen as an important source of energy for decarbonizing the energy system. For the green production of hydrogen, large numbers of electrolysis plants with high-performance stacks will have to be set up worldwide. With its expertise, Bosch has huge business opportunities here. And it is on those opportunities that we will focus.”

Dr. Thomas Pauer, the president of Bosch Power Solutions

OB - Volatile Market Developments aren’t defined but are likely to mean the collapse of the prior government in Germany (who were strong Hydrogen backers), the collapse of the Democrats in the USA, the collapse of Justin Trudeau. But more than this the focus on Stationary vs Mobility Government Support Changes are a major source of what has made it “volatile” - see later.

Hydrogen remains a strategic growth area for Bosch. By 2030, Bosch hydrogen technology may generate sales revenue running into billions of euros. Above all, the market for H2 production is stirring. Worldwide, hydrogen electrolysis will reach an installed capacity of between 100 and 170 gigawatts by 2030. By the end of the decade, the global electrolysis market is expected to have a volume of as much as 37 billion euros. Bosch is on track to debut its electrolysis stack this year.

OB - This final paragraph “remains… a growth area” felt a total contradiction to the earlier points of the “volatile market” and “the market has not developed”. But when you read it along the lines of how I’m interpreting it (Stationary vs Mobility) then it makes perfect sense.

Part 2: Why Bosch Ended Its Relationship with Ceres Power

Bosch and Ceres Power, a UK-based developer of solid oxide electrochemical technology, collaborated from August 2018 until Feb 2025 on SOFC systems for stationary power generation. Let’s consider why this relationship concluded:

Part 2.1. Bosch Reasons Mobility

Bosch is reknown for its Tier 1 status for Automotive.

Bosch is already mass-producing fuel cells for transport at factories in Germany and China, and also plans to produce hydrogen engines for trucks. Mobility is Bosch’s largest segment (by far) and Ceres isn’t ever going to be used for mobility.

Overview of Changes in Western Government Support for Mobility

Government support for mobile and stationary power applications has evolved significantly in recent years, driven by decarbonisation goals, energy security, and technological maturity. While both areas have received attention, the balance has shifted, with mobile power (especially hydrogen for transport) gaining momentum over stationary power (like SOFCs) due to market demand, policy priorities, and infrastructure needs. Here’s what’s changed:

1. Increased Focus on Power for Mobility Support (Hydrogen for Transport)

Policy Shift: Governments have ramped up support for mobile power, particularly hydrogen fuel cells and electric vehicles (EVs), as part of transport decarbonisation. This reflects a push to reduce emissions from road, rail, and shipping, sectors harder to electrify directly.

EU Examples:

REPowerEU (2022): Targets 10 million tonnes of green hydrogen production and 10 million tonnes imported by 2030, with €3 billion allocated for hydrogen infrastructure, much of it mobile-focused (e.g., refuelling stations). The Hydrogen Valleys initiative supports transport applications alongside industrial uses.

Fit for 55 Package (2021–2023): Mandates zero-emission vehicles, boosting hydrogen fuel cell deployment with subsidies and tax incentives (e.g., €1.5 billion in Germany for H₂ trucks by 2024).

US Examples:

Bipartisan Infrastructure Law (BIL, 2021): allocates $8 billion for Regional Clean Hydrogen Hubs, with significant emphasis on hydrogen for heavy-duty transport (e.g., trucks, buses). The Inflation Reduction Act (IRA, 2022) offers a $3/kg hydrogen production tax credit, indirectly benefiting mobile applications by scaling supply.

DOE Funding: $7 billion (announced 2023) for hydrogen hubs includes mobile-focused projects, like California’s ARCHES hub targeting zero-emission transport.

UK Examples:

Hydrogen Strategy (2021, updated 2023): £240 million for hydrogen production, with £100 million in 2024 for transport trials (e.g., Teesside hydrogen buses). The Zero Emission Road Freight programme funds H₂ trucks, contrasting with less focus on stationary power.

Trend: Mobile power support has surged since 2021, driven by COP26 commitments and net-zero transport goals, outpacing stationary power in funding priority.

2. Power for Stationary Support: Steady but Losing Ground

Historical Context: Stationary power, including SOFCs and grid backup systems, saw strong support in the 2010s for decentralised energy and resilience (e.g., US DOE’s Fuel Cell Technologies Office funded SOFC demos). However, focus has waned relative to mobile applications.

EU Examples:

Horizon Europe (2021–2027): €1 billion for clean hydrogen, but stationary SOFC projects (e.g., CHP) receive less than 20% of this, with most going to electrolysis and transport. The Fuel Cells and Hydrogen Joint Undertaking (FCH JU, phased out 2021) once backed SOFCs heavily, but its successor prioritises H₂ production.

Germany: €9 billion hydrogen strategy (2020) focuses on electrolysis over stationary fuel cells, though CHP subsidies persist (€0.04/kWh for micro-CHP, down from earlier peaks).

US Examples:

IRA and BIL (2021–2022): $10.5 billion via the Grid Resilience and Innovation Partnerships (GRIP) programme supports stationary grid tech, but hydrogen production overshadows fuel cell power generation. SOFC funding (e.g., $30 million in 2020) has stagnated, with no major new grants by 2025.

State-Level: California’s Self-Generation Incentive Program (SGIP) still funds stationary fuel cells (~$250/kW), but EV and H₂ transport incentives dwarf this ($1 billion+ since 2022).

UK Examples:

Energy Security Strategy (2022): Doubles hydrogen production goals to 10 GW by 2030, but stationary power (e.g., SOFC microgrids) gets minimal mention compared to £500 million for H₂ transport and industrial use.

Trend: Stationary power support remains, especially for grid resilience, but it’s less dynamic, with policies pivoting to hydrogen supply over on-site generation.

3. Drivers of the Shift

Decarbonisation Priority: Transport accounts for ~30% of global CO₂ emissions (IEA, 2023), dwarfing stationary power’s share outside centralised plants. Governments prioritise mobile hydrogen to hit 2030 targets (e.g., EU’s 55% emissions cut).

Market Volatility: Bosch’s 20 February 2025 press release cites “volatile market developments” for dropping SOFCs—stationary power demand (e.g., microgrids) grew slower than expected (~5% CAGR vs. 20%+ for H₂ transport, per BloombergNEF 2024).

Infrastructure Investment: Mobile power needs refuelling networks (e.g., EU’s 600 H₂ stations by 2030), driving bigger, more immediate funding than stationary systems, which rely on niche or existing grid integration.

Tech Maturity: PEM electrolysis is mature and scalable (e.g., Bosch’s 1.25 MW stacks), while SOFCs remain costlier (~€2,000/kW) and less versatile, reducing government enthusiasm.

4. Quantitative Changes (Recent Years)

EU: Hydrogen funding rose from €1.5 billion (2014–2020, FCH JU) to €5.4 billion (2021–2027, Clean Hydrogen Partnership), with ~60% now mobile-focused vs. 40% stationary in prior cycles.

US: BIL/IRA allocate $15 billion+ to hydrogen since 2021, with ~70% supporting production and transport vs. ~10% for stationary fuel cells (DOE estimates, 2024).

UK: Hydrogen Transport Hub funding tripled from £33 million (2021) to £100 million (2024), while stationary CHP subsidies stayed flat at ~£50 million annually.

Part 2.2. Bosch Reasons: Chemicals or Protons

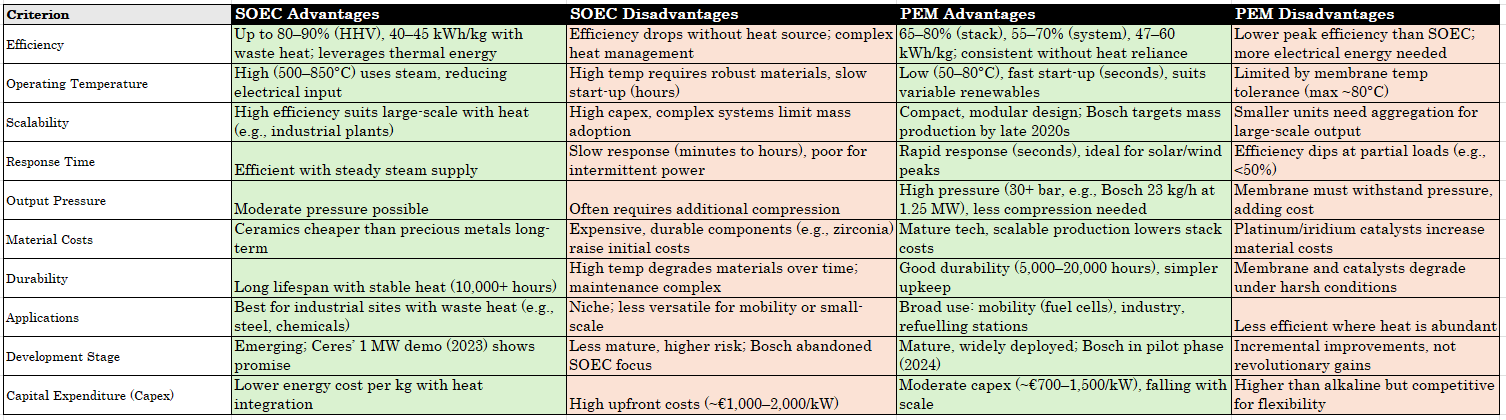

Bosch is pursuing PEM (Protons) instead of SOEC (Chemicals). Considering the types of business it is focused on PEM is the obvious choice. It’s actually a bit surprising they spent an estimated €500 million on SOEC in the first place. Hedging their bets perhaps. Meanwhile CWR has been a beneficiary to that spend of course.

PEM is a proton exchange membrane. Essentially it is using electricity to split atoms rather than using chemistry. PEM electrolysis uses a solid polymer electrolyte membrane to separate the hydrogen and oxygen gases. This membrane allows for high proton conductivity, a key process in the creation of green hydrogen, while preventing the mixing of gases.

PEM Electrolysers are well suited to sit alongside Renewables, for example, which need fast response. SOEC doesn’t work that way.

This chart sets out the pros and cons of both technologies:

The Bosch representative in this video focuses on transport and on green energy (i.e. from renewables). He’s talking about markets that need PEM.

Part 2.3. Bosch Reasons: Cost Concerns

I’ve read a line of thinking on Twitter about how Bosch “ran away from SOFC” due to its Levelised Cost of Energy (LCOE) didn’t meet expectations relative to licensing costs or market uptake. There’s no evidence provided to back up that view.

The evidence is that Bosch’s PEM consumes 52KWh of electricity to produce 1Kg of hydrogen while SOEC consumes just 37KWh.

Yes the LCOE is also the licence cost (a few percent?) and the capex cost (about a 30% one-off cost difference per KW), but we see leadership of cost from Ceres, and this October 2024 white paper illustrates progress (with more to come in 2025) so I find this line of thinking unlikely.

4.Philosophically different “Centralised” vs “Decentralised”

As well as power for Stationary vs for Mobility there is also the other use case of “Centralised” and “Decentralised”.

PEM electrolysers exist essentially as part of an energy producer’s arsenal. They support the energy producer intermittently in storing and utilising energy.

SOFC electrolysers exist essentially as part of an energy consumer’s arsenal. They support the energy consumer in achieving “off grid” or supports a plan B for when/if the energy producer lets you down. SOFC tend to be part of a continuous industrial process rather than intermittent. Particularly for an industrial process involving heat.

The customers and sales channels for each of the above are very different. It’s been suggested that Bosch lacked the channels to sell SOFC.

Part 3: What about CWR? What about its future success?

So I’ve explained Bosch but presumably you aren’t an investor in Bosch, but either an existing or potential investor in CWR. Or a detractor I suppose.

What does CWR’s future look like?

1. Mobility is growing faster - but Stationary is growing too

PEM is unlikely to supplant SOFC in Stationary applications where it doesn’t have the advantage and is unlikely to achieve one even with scale and experience curve. Meanwhile the latest stats show 25% growth from 2023 to 2024 and a more than tripling in the next 10 years.

2. Hydrogen growing for Mobility is good for Stationary too

This isn’t a zero sum game, and let’s not forget mobility is 30% of emissions, and theoretically the easier 30%. 70% of emissions is the more challenging Stationary applications (Cement, Steel etc etc)

Will Government Support switch to Stationary? It seems once Mobility is sufficiently seeded COP number whatever at some point will move to addressing the Stationary market.

3. Other Technology can negate some of SOEC weaknesses

It was interesting to listen to Prof. Richard Hulf the Hydrogen Expert (of HGEN). One of the comments he made was how BESS is being alongside Electrolysers. Think about it. SOEC is a slow response but BESS isn’t. BESS can be a buffer in this scenario. So you get the efficiency of SOEC alongside the near instantaneous response of BESS.

Part 4: Considering Ceres’ Other Partnerships

Ceres operates an asset-light, licensing model, developing electrochemical technologies (SOFCs for power generation and solid oxide electrolysis cells [SOECs] for hydrogen production) and partnering with global firms to scale these solutions. Beyond Bosch, its key partnerships include:

Delta Electronics (Taiwan):

Details: A major manufacturing partner since 2023, Delta licenses Ceres’ SOFC and hydrogen tech. A £43 million deal (announced September 2024) delivered £20.2 million in H1 2024 fees, with £22 million more expected, targeting STATIONARY industrial and data centre applications.

Scope: Delta, a thermal power and electronics giant, uses Ceres’ tech for power modules, with a 250 kW system tested in 2024.

Denso Corporation (Japan):

Details: A 2023 manufacturing licence agreement with this automotive parts leader focuses on SOFCs for industrial power. Denso’s scale and expertise bolster Ceres’ reach in Japan, a key stationary power market.

Scope: Part of Ceres’ three manufacturing partners (with Delta and Doosan), Denso aims for multi-kilowatt systems (Ceres earnings call, September 2024).

Doosan (South Korea):

Details: A long-standing partner, Doosan licenses Ceres’ SOFC tech, scaling to 600 kW modules for stationary power (e.g., utilities, buildings). Active since at least 2018, it’s a cornerstone of Ceres’ revenue.

Scope: Focuses on South Korea’s 700 MW stationary fuel cell market, with growth plans to 1 GW by 2040.

Thermax (India):

Details: A 2024 partnership licences Ceres’ tech for industrial decarbonisation in India, targeting steel and ammonia sectors (Ceres earnings call, September 2024).

Scope: Addresses India’s emerging hydrogen market, with pilot deployments planned.

Shell:

Details: A system partner since 2023, Shell collaborates on a 1 MW SOEC demonstrator (commissioning 2024–2025) for green hydrogen, scalable to multi-MW modules (Proactive Investors, November 2024).

Scope: Focuses on hydrogen production, not stationary power, aligning with Bosch’s new PEM direction.

Weichai Power (China):

Details: Licences SOFC tech for power generation, scaling to 75 kW modules for megawatt applications (Ceres earnings call, September 2024).

Scope: Targets China’s industrial and transport sectors, though stationary power is secondary to mobile uses.

Will These Partnerships Survive the Bosch News?

To assess survival, we need to consider the impact of Bosch’s exit on Ceres’ financial health, market confidence, and partner dynamics:

1. Financial Impact

Ceres’ Position: H1 2024 revenue doubled to £28.5 million (from £11.7 million in H1 2023), with a £13.8 million operating loss (down from £28.3 million), per The Times. Cash reserves stood at £126 million (as at 30 June 2024), bolstered by Delta’s £43 million deal. Full-year 2024 revenue is projected at £50–60 million (Ceres earnings call).

Bosch Effect: Bosch’s exit doesn’t alter Ceres’ 2025 consensus expectations (Ceres RNS, 20 February 2025), as it was a manufacturing partner, not a revenue driver in 2024. However, future royalties (e.g., £23 million from 2021–2023) are lost, impacting 2026+ forecasts (according to Panmure Liberum).

Survival Odds: Ceres’ £102 million cash pile (according to Jefferies, 20 February 2025) and new licensing deals (e.g., Delta, Thermax) provide a buffer. Partners aren’t immediately threatened financially, but long-term growth relies on replacing Bosch’s royalty stream.

2. Market Confidence and Perception

Share Price Drop: Ceres’ stock fell 55% (to ~70p) post-Bosch news, from 150p. Analysts like Berenberg cut targets (650p to 340p) but remain bullish, citing other partnerships.

Analyst Views: Citi (21 February 2025) calls the reaction “knee-jerk,” noting Bosch’s exit as a one-off strategic shift, not a Ceres failure. Jefferies (20 February 2025) maintains a Buy rating (265p target), highlighting Delta and Shell as growth drivers.

Partner Risk: Bosch’s divestment of its 17.44% stake creates a “negative overhang” (Panmure Liberum), potentially spooking partners if market confidence wanes further. However, Ceres’ CEO Phil Caldwell (RNS, 20 February 2025) frames it as Bosch’s strategic pivot, not a tech rejection, which partners like Delta and Denso seem to accept.

3. Partner-Specific Resilience:

Delta Electronics: Strong, with £43 million committed and 250 kW systems in testing. Taiwan’s industrial focus and Delta’s scale insulate it from Bosch’s stationary power exit. Likely to survive.

Denso: Robust, leveraging Japan’s mature SOFC market (400,000 Ene-Farm units). Denso’s automotive expertise diversifies its use beyond Bosch’s scope. High survival chance.

Doosan: Stable, with South Korea’s 700 MW stationary base and long-term collaboration. Bosch’s exit doesn’t disrupt Doosan’s utility focus. Very likely to endure.

Thermax: Early-stage but promising, targeting India’s decarbonisation boom. Bosch’s news may delay confidence, but Thermax’s niche (e.g., steel) supports survival.

Shell: Unaffected, as it’s SOEC-focused (hydrogen production), aligning with Bosch’s new PEM direction. Strong survival odds.

Weichai: Mixed, on one hand China’s stationary power is lagging mobility (<50 MW) on the other Weichai have succeeded in delivering their 1st SOFC-based CHP system in Western China. Weichai’s transport focus may shift priority, but the partnership is likely to persist short-term.

4. Bosch’s Exit as a Precedent

Why Bosch Left: Cited “volatile market developments” and a shift to PEM electrolysis for “higher-output systems with carbon capture” (press release). This reflects a broader market pivot to hydrogen production over stationary power, not a Ceres-specific issue.

Partner Reaction: Delta, Denso, and Doosan focus on SOFCs for power, while Shell and Thermax align with SOECs for hydrogen production—diverse goals reduce contagion risk. Bosch’s 17% stake sale (orderly, per RNS) won’t directly force partners out, though a buyer’s identity could sway sentiment.

Conclusion: Survival Likelihood

Ceres’ other partnerships are likely to survive the Bosch news in the near term (2025–2026), with caveats:

Strengths: Financial stability (£126m cash), recent revenue growth (£28.5m H1 2024), and diversified partners (Delta, Shell) cushion the blow. Bosch’s exit is framed as a strategic realignment, not a Ceres failure, supported by analyst optimism (Citi, Jefferies).

Risks: Lost SOFC royalties and a 50% share drop could erode confidence if Ceres doesn’t secure new deals or a strong Bosch stake buyer. Stationary power’s slower growth (5% CAGR vs. 20% for H₂ production, BloombergNEF) may pressure SOFC-focused partners (e.g., Doosan, Denso) long-term.

Verdict: Delta, Denso, Doosan, and Shell are robust; Thermax and Weichai are less certain but viable. Survival hinges on Ceres maintaining momentum with SOEC (e.g., Shell’s 1 MW SOEC success) and market recovery post-Bosch overhang. Plus new partnerships.

Linde is very much focused on the Stationary market but is unlikely to require SOFC. SOEC is another matter. It is the largest hydrogen producer and distributor in the world. So while the partnership and the 1 MW SOEC demonstrator with Linde was via Bosch it will be interesting to see if a new partnership is formed between Ceres and Linde. It is almost certainly under discussion. What will happen to the CWR share price if a Linde partnership is announced?

Part 5: BUT SHOW ME THE MONEY!

Ceres’ Revenue Model and Bosch’s Role

Ceres Power operates an asset-light, licensing-based business model, generating revenue through:

Licence Fees: Upfront payments from partners for using Ceres’ SOFC and SOEC technology.

Engineering Services: Development and support contracts.

Royalty Payments: Ongoing fees tied to partners’ production or sales of Ceres-based systems.

Hardware Sales: Minor, as Ceres focuses on tech licensing, not mass manufacturing.

Bosch was one of Ceres’ key manufacturing partners since August 2018, collaborating on SOFC systems for decentralised power supply. Bosch’s contributions included licence fees, engineering contracts, and potential royalties as the partnership progressed towards industrialisation.

Available Financial Data for Ceres:

H1 2024 (1 January–30 June 2024): Revenue doubled to £28.5 million from £11.7 million in H1 2023, driven by licence agreements, notably with Delta Electronics (£20.2 million received, £22 million more expected from a £43 million deal), per Ceres’ earnings call (September 2024) and The Times (20 February 2025).

Full-Year 2023: Revenue was £22.3 million (Ceres Annual Report), up from £22 million in 2022, with operating losses narrowing from £51 million to £46 million.

Full-Year 2024 Forecast: Projected at £50–60 million (Ceres RNS and earnings call, September 2024), reflecting Delta’s contribution and ongoing deals with Doosan, Denso, and others.

Cash Position: £126 million as of 30 June 2024 (Investors’ Chronicle), providing a buffer post-Bosch.

Bosch’s Revenue Contribution

Bosch’s exact revenue share isn’t broken out in CWR’s reports, as they aggregate income across partners (e.g., Bosch, Delta, Doosan). However, we can estimate based on historical agreements and recent statements:

1. Historical Payments

2018–2020 Agreements: Bosch initially took a 3.9% stake in Ceres for £9 million in 2018, increasing to 18% by 2020 with further investments (~£60–90 million total, per analyst estimates from Berenberg and Proactive Investors). These were equity investments, not direct revenue, but tied to collaboration.

2021 Milestone: A £23 million SOFC deal (Ceres announcement, 2021) covered licence fees and engineering services from 2021–2023, with Bosch paying for development and pre-commercial stacks. This wasn’t annual but phased revenue.

2. Recent Revenue (2023–2024)

Minimal in 2024: Bosch’s contribution to Ceres’ £28.5 million H1 2024 revenue appears negligible. Ceres’ earnings call (September 2024) and RNS (20 February 2025) highlight Delta (£20.2 million) as the primary driver, with Doosan, Denso, and Shell also active. Bosch isn’t flagged as a significant 2024 revenue source, suggesting its payments tapered off post-2023 as industrialisation stalled.

2023 Estimate: In FY 2023 (£22.3 million total), Bosch likely contributed a portion of the £23 million deal’s tail end (e.g., £5–10 million), alongside Doosan and early Delta fees. Assuming £5 million (conservative), Bosch was ~22% of 2023 revenue (£5m / £22.3m).

3. Post-Bosch Impact

2025 Outlook: Ceres’ RNS (20 February 2025) states Bosch’s exit doesn’t alter 2025 consensus expectations (£50–60 million revenue), implying Bosch wasn’t a major revenue contributor in 2024 or planned for 2025. Lost future royalties (e.g., £5–10 million annually by 2026, according to analyst guesses) affect long-term growth, not immediate income.

Analyst Insights: Panmure Liberum (20 February 2025) notes Bosch’s royalties were “not yet material” in 2024, with Delta, Doosan, and Shell filling the gap. Jefferies (20 February 2025) estimates Bosch’s exit cuts 2026+ revenue by 10–15%, but doesn’t affect either 2024 or 2025.

Proportion Calculation

2024 (H1): Bosch’s share was likely <5% of £28.5 million (e.g., £1–2 million max from residual engineering work), as Delta dominated (£20.2m). Full-year £50–60 million projection reinforces this, with Bosch near zero.

2023: More significant, potentially 20–30% (£4.5–6.7 million of £22.3 million), based on the £23 million deal’s tail end spread over 2021–2023.

Historical Peak (2021–2022): If £23 million was evenly split (£7–8 million/year), Bosch could have been 30–40% of revenue (£22m total in 2022), though Doosan and others diluted this.

Bosch’s Revenue Proportion

2024: Negligible (<5%, ~£1–2 million of £50–60 million projected), as Bosch’s active revenue faded before the exit, overshadowed by Delta (£43m deal).

2023: Moderate (20–30%, ~£4.5–6.7 million of £22.3 million), reflecting late-stage SOFC collaboration payments.

Pre-2023: Higher (30–40% in 2021–2022), when Bosch was a core partner alongside Doosan.

Bosch was a significant revenue source in earlier years (2021–2023), peaking at maybe a third of Ceres’ income, but its proportion dropped sharply by 2024 as Delta and others took over. The 20 February 2025 exit doesn’t disrupt current revenue (Ceres’ £102m cash and £50–60m 2024 forecast hold), but future royalties are lost, impacting 2026+ growth. This aligns with Bosch’s “non-core financial investment” stance and Ceres’ pivot to other partners (e.g., Delta, Shell).

Conclusion

At 70p, CWR is at a £136m market cap, and includes £102m cash (75% of market cap). So you are paying just 17.5p per share or £34m net of est. cash for world class technology with world-class partners whose collective market cap are over £300bn, and who are going after markets worth many billions of pounds per year. CWR a business which grew its order book by £110m in 2024, grew revenue 150% to £55m-£60m, that enjoys a gross margin of 78%-80% and whose costs decreased 15% going forward.

It’s true that about £10m per year of revenue (£8m EBITDA) has been lost from 2026, from Bosch pulling out. Consider that that -£10m annual loss is just one third of the growth CWR achieved in 2025, or one eleventh of its order book.

Where Cash Flow Forecasts placed the cash low point at £68m in 2026 prior to turning positive. So replacing an estimated -£8m loss of cash flow through Bosch perhaps puts back CWR turning FCF positive by a year? Reduces the cash low point to £50m perhaps?

When you look at it, the price falling over 50% to 70p is more than a little bit mental.

Make your own decisions, but for me it was an easy one to make.

Regards

The Oak Bloke.

Disclaimers:

This is not advice, you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

https://www.yorkshirepost.co.uk/business/bp-axes-teesworks-green-hydrogen-project-5019862

I agree, but look long term and the performance of CWR is similar to INRG. Is CWR up there with the best of the index, or is Hydrogen not the growth sector / solution to decarbonisation we all thought?

Personally, I am considering doubling down on this as my average is around 110p. Results are due out in a few weeks, question is to top up now or after then with more information to hand.