Bringing cadence to cadence

Positive updates

Dear reader,

My first article back in August 2023 as “The Oak Bloke” was Cadence (LON:KDNC).

Comparing last August to today an utter decimation of Lithium and Rare Earth plays. (who’d have thought - so much for energy transition and shortages!)

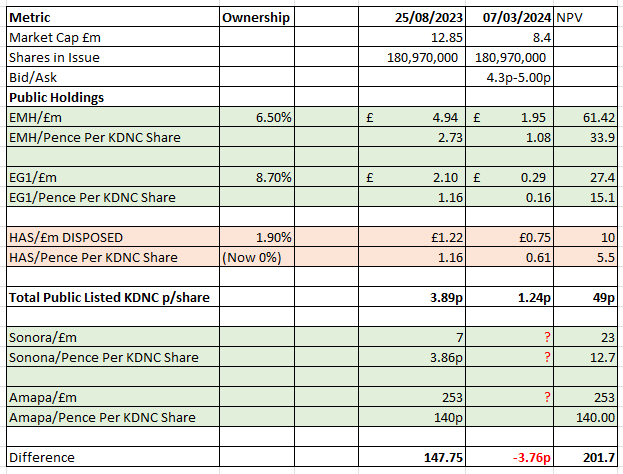

This charts set out the movement from August to today.

KDNC announce disposal of Hastings (HAS) freeing up an estimated £0.75m towards progressing Amapa.

Today KDNC announce several positives:

Both EMH (European Metal Holdings) and EG1 (Evergreen) are themselves progressing their projects. EMH has a 36.7% IRR and a 51% partner in CEZ the state power utility and backing from the European Bank of Reconstruction and Development while EG1 is earlier stage but with cash for a long runway. The DFS is imminent and the FID due in 2024. While the entire lithium juniors are down, the medium-long term growth of lithium demand remains undimmed.

Moreover EMH’s NPV is at conservative commodity price estimates. For example EMH's PFS put Lithium Hydroxide at US$10,000/tonne and Carbonate at $12,000/tonne. Even with today’s low prices they are not THAT low!

Also of note is EMH’s simplified flowsheet. WHI said "At the full 20% reduction, this increases our NPV10 for the project as envisaged currently by EMH of $149m to $1,217m using our new long-term lithium carbonate price of $15,000/t, and by $300m to $3,655m for our expanded case (whereby EMH doubles production from year 6)." That would imply a 6.5% of EMH @ US$3.6bn NPV x 49% is worth £90.25m/49.88p or an extra 15.94p a share.

Further investments made in Amapa should move KDNC’s ownership from 32.6% to 35%

The Amapa project has unannounced but referenced capital savings it will announce in its March update.

The Amapa product will be a higher value 67% FE ore worth $10/tonne more. This leads to the NPV of $949m up towards $1.2bn. On a 35% holding this equates to a £77m uplift from the prior £253 valuation to £330m.

KDNC has reduced its costs by cancelling its dual listing with Aquis.

>50% resource upside via Tucano which is adjacent to Amapa and where gold mining has recommenced but where KDNC has mining rights to the Iron Ore. There is an opportunity to improve the economics of the overall project further than my estimate of $1.2bn.

Tucano is one of the areas. There is also the "Great Panther" area which could contain further orebodies. A doubling of ore is not impossible. 50-100p?/KDNC share.

What premium value is there for safe jurisdiction assets? Who controls 80% of lithium refining and battery production. Not the West. Where's EMH located? The West. A few dozen miles from Bavaria's and Czechia's EV production. EG1 is in Australia. Sonora is proximate to US/Mexican EV production. Given the geopolitical tensions assets in friendly jurisdictions usually come at a premium – and not at a 98% discount.

8. EG1 – there's a further A$3.47m of shares due to KDNC on completion of certain performance milestones. Assuming this occurs this would have the effect of diluting existing EG1 shareholders by 24.6% and would increase KDNC's holding from 8.7% to 33.3%. EG1 is a A$46.17m market cap so a third would be worth £7.77m (£5.67m more).... at today's prices. Going back to the NPV of £570m that 33% would be worth £188.1m – or an increase from £0.27 to £1.04/per KDNC share.

Conclusion:

25% of the buy price of KDNC is covered by publicly listed holdings, leaving 75% of 3.75p

There are further reasons why Amapa offers even greater upside, even while on the face of it this shows a deterioration since August and of course selling Hastings at a profit relative to the original cost but at a colossal 91% discount to its NPV points to the dual aspects of opportunity and risk around cash here.

But with an MoU in place for Debt Finance being managed by Tianjin Cement Industry Design & Research Institute Co., Ltd ("TCIDR") and has received expressions of interest, and in discussion, the DFS and then the FID are getting closer.

Even considering risk, and ignoring any upside to publicly listed holdings upsides, the 98.2%+ discount on Amapa/Sonora makes no sense.

Today’s news makes the upside even more compelling if it can get there.

This is not advice

Oak