Can you be crazy on RESI?

An apparent 36% and hidden 61.1% discount for doing good

Residential Secure Income plc (Ticker: RESI) is a REIT focused on secure, inflation-linked returns in two sub-sectors of UK residential housing

Independent retirement rentals (given our aging demographics, 2/3 of portfolio)

Shared ownership, affordable homes. (1/3 of portfolio)

So a long-term private sector landlord.

Its tasty discount, its strong dividend, its inflation-linked rents, its appreciating property, massive demand due to the need for affordable homes and retirement living, what could possibly be not to like?

Safe as Houses? (The bear case)

Losses for a start. But let’s examine these losses, RESI tells us its “adjusted EPRA earnings” were a profit. Is the loss theoretical? Or real?

They lost money in FY23 and in the FY24 interims. £44m is about half of today’s market cap. Ouch!

A market cap which was at least double back in 2021 and early 2022.

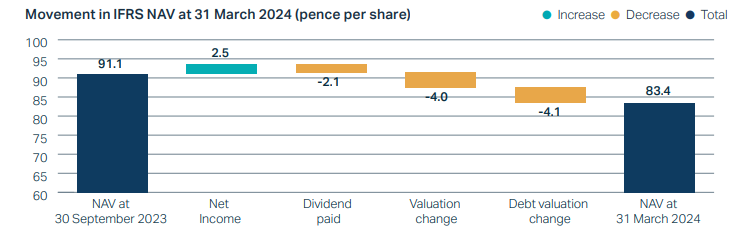

Moreover there have been dividend cuts or “rebased” as RESI say. They’re cuts cry the harrumphers. Meanwhile the NAV is falling, as pictured, making it appear the houses are crumbling away to zero.

So it would be easy to conclude that RESI is rubbish.

But is it?

These losses are based on two separate measures “Fair Value of Property” and “Fair Value of Debt”. The former is due to a discount increase from 4.9% to 5.1% and latter due to a notional improvement in the credit worthiness of the USS (the lender) which is reflected in a reduction of the credit spread to 1.25% (from 1.47%).

This followed a 0.8% increase in discount rate in FY2023 from 4.1% to 4.9%, equal to a whopping £39.6m loss or about 1/2 its market cap today…..Ouch!

Now eagle-eyed readers will know that I take a dim view of this discount rate methodology, arguing that the true value of assets rather depends on their capability to generate increasing returns over time but also that the assets themselves are deemed valuable. The discount rate “noise” will revert as interest rates change.

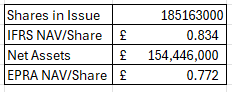

Currently on a NAV of EPRA 77.2p or IFRS 83.4p depending on your view of part of the debt. On an EPRA basis the debt is valued at “amortised cost” which leaves the remaining assets valued at 77.2p per share while IFRS’ fair value basis is 83.4p. According to Deloitte and the rules of IFRS9 if the assets are “held for sale” then “fair value” should apply (83.4p), or if the assets are held for income then “amortised cost” should apply (77.2p). In other words, if RESI shut up shop tomorrow there’s a 6.2p per share uplift as all the assets come up for sale. As it is staircasing and disposals are two ways this “transformation” occurs.

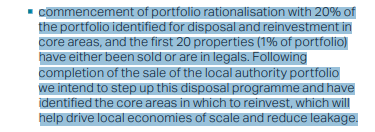

It is also the case that there’s a £20m sale of assets ongoing as part of an exit from Local Authority business (housing homeless folk). There are two remaining assets in legals which “should” complete in H2. The variable debt relating to this and is due end of 2024 therefore there is a qualified point of “going concern” as a result. RESI say they fully expect the sale to conclude and the debt to be repaid, and that alternative funding options exist if not. You could argue this to be an Achilles heel so it’s something to be comfortable with - or not.

Otherwise, debt is on 20 year average terms with extremely favourable and low rates of 3.5% fixed until 2043, and RPI + 0.5% (up to a capped 5.5%) over 40 years.

Quality Assets

I also took note of the substantially better average EPC of RESI’s properties. These will be 100% C and above by 2025. By comparison the wider market are not even 50% C or above.

The extremely high levels of occupancy reflect the quality and competitive nature of these properties also. ReSI is the UK’s largest provider of private independent retirement rental homes - with a guaranteed LIFETIME TENANCY. The UK population is rapidly ageing, with the demographic over 65 expected to increase by almost 50% by 2060.

Social isolation can have a material impact on the health of the elderly, driving demand for independent retirement accommodation where residents can enjoy the benefits of living and socialising with other like-minded individuals. 81% of RESI’s residents have been equally or more socially active since moving in.

There will be huge growth in this sector of the market, and with that a great opportunity for ReSI to take advantage of its market leadership position.

Hidden Value

There are subtle clues which aren’t apparent (other than to eagle-eyed readers of course). So let’s examine those. First we see a small but growing “Staircasing”. This is the concept that someone in shared ownership wants to buy RESI out and own the whole asset outright. The percentage of shared homes owned by their residents has grown to 38% from 37% in 2024. Sales of equity from RESI to resident are done at market rates. This is significant because none of this value is in RESI’s price. 1% of shared of 1/3 of £346m is £1.14m. A £0.168m profit suggests a 1/7 upside, which is equal to £16.3m.

But the upside value is actually plain to see in the accounts. It’s the reversionary surplus. A whopping £81.1m pounds…. nearly the entire market cap of £88m.

This means if RESI shut up shop tomorrow and sold off its assets the value of those assets is higher than the book value…. a lot higher. (As valued by Savils)

But the “if only” is happening. RESI tell us in the interims that 20% of the portfolio is being disposed of.

20% of the portfolio would be around £69m with 20% hidden value being another £15m so that’s £84m of property realisations, which is £4m shy of the entire market cap.

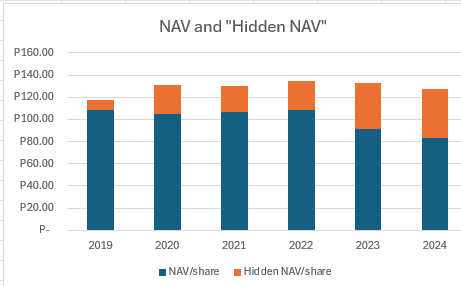

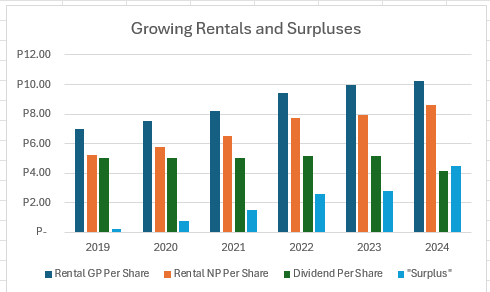

2019 - 2024 accounts (NB the final column 2024 is only to March 2024)

Where will that £84m cash go once realised? There’d be no point paying down debt, so further purchases of property could happen and a special dividend could happen or buy backs - or all three. What if £84m was entirely paid to shareholders? That’s over 45p a share! I expect the bulk will go towards new property but even 10% of the the cash equals 4.5p or around 10% of today’s share price.

Would losing 20% of the rental yield affect future dividends? No. There is a huge cushion in the rental vs the dividend. Would the 20% disposals be from Retirement Living or Shared Ownership? RESI don’t specify, although it could be the former in order to grow the proportion of shared ownership. The staircasing and ability to achieve realisations is attractive. But both verticals have huge growth potential so it’s a pity to be reducing either.

The charts show the “risk” of RESI and the harrumphers selling up clearly have not understood the value of the portfolio, in my opinion. If we see the data graphically we see a/ the portfolio’s true value is far more resilient than the accounts with apparent losses describe b/ that the degree of hidden value is growing - i.e. there’s a disconnect between the book and actual value of assets. But that disconnect will get “connected again” through both staircasing (shared owners owning more) and disposals. And indeed as discount rates reverse - will we see a rate cut soon? It appears likely.

I said in my criticism of discount rates, that apart from the security and growth of the value of the assets, the second factor is the security and growth of the underlying income (and net earnings) of assets are what also matters. This graph clearly shows that there is a growing income stream for RESI and no sign of this diminishing despite covid, record inflation, supply chain, war etc etc - if anything the portfolio is counter cyclical and defensive (inflation-linked returns).

May I point out the dividends which are a “deduction” from the NAV are also a return to shareholders. 29.44p over the past 6 years (on a share you can buy for 49.3p today). So a 10% average dividend return, where the rebased dividend is 8.3% and contains plenty of wriggle room for special dividends.

After all, 77.9p per share is hidden according to the numbers. That’s a 61.1% discount to the reversionary NAV.

Fund charges have also been reduced and are now 1% of the average of 50% of NAV and 50% of the market cap. So a £1.2m charge by my reckoning.

To conclude, the accounts can lead you to believe one thing but the underlying data are much more positive. The value of 20 year fixed rates and inflation-linked debt and the leverage that gives in today’s higher interest rate world is totally ignored. Moreover, disposals and staircasing, along with inflation-linked rent increases and low levels of void make this an exceptionally good play on UK property - but specifically on two areas of growth and need: Quality retirement living at reasonable rates and shared ownership affordable property. You can probably tell I really like this idea, since it ticks boxes on cash generation, lower levels of risk, with hidden assets and a chunky return, and positive macros… while delivering a moral “good” too.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

EPRA NAV does not include the fair value of the debt

There's only realisable value in the debt if it can be sold, and theres usually (though not always) a chance of control covenant that prevents that, so 77p is the more relevant NAV

There is not £81m of hidden value that can be monitised

The reversionary surplus comes from life time tenants dying (so PV that back and account for property Capex) and from staircassing, very few shared ownership tenants ever staircase - so you just won't access the reversion (ok you do at the end of the lease - that's in 240 years)

You simply cannot sell assets and access "hidden" value

RESI will not be realising anything close of their current market cap