CHRY out for KLARNA-rity

$29m Q1 operating profit for pre-IPO holding Klarna

Dear reader

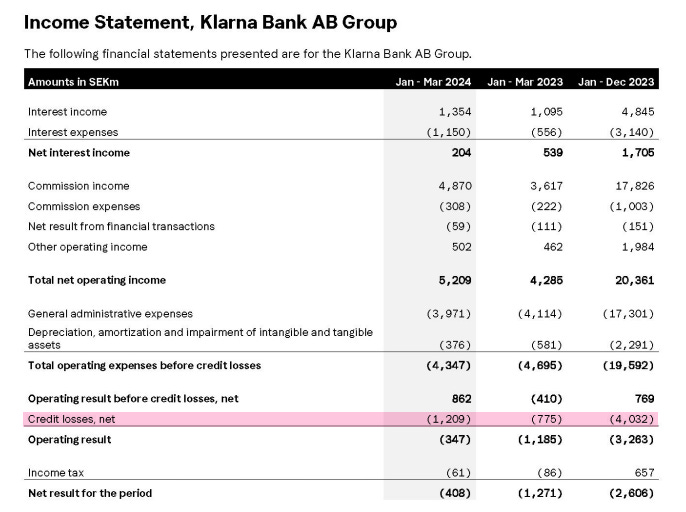

CHRY’s holding Klarna (valued 31/3/24 at £100m) announced revenue and profit progress in today’s Q1 update.

Revenue was up 29% year on year. Profits were up too. Excluding credit losses a SEK862m profit is about $29m, or a $15m loss inc. credit losses - a two thirds improvement to a year ago.

It points to USD 50m of annualised savings achieved in Q1 alone through innovations with AI. While speaking to its new US Klarna card, rapid online sign in, and its Klarna Plus subscription which attracted 70k sign ups.

But Uber aren’t the only ones - Klarna also struck a deal with travel giant Expedia/Hotels.com too.

VALUATION

CHRY owns 1.11% of Klarna so if a $20bn/£16bn price is achieved, the result for CHRY is a substantial £74.80m uplift and a £174.80m realisation.

But that’s only part of the story. You can buy CHRY for 80.6p ask. Its NAV is 147.46p.

So effectively that £100m share of Klarna you can buy for £54.7m. (due to the 45.3% discount to NAV)

So your true upside from a $20bn Klarna IPO is actually £120.1m or 2.2X times what you can buy CHRY for today.

£174.8m proceeds after keeping back £30m so there’s a £50m working capital, will be going to buy backs.

£144.8m of buy backs at 80.6p a share would buy back 179.65m shares (of 595.15m) leaving 415.5m shares.

Those remaining shareholders would have £50m cash and £758.2m of assets. That’s a NAV of 194.5p per share (a 47p per share accretion).

And Klarna’s not the only IPO brewing away at CHRY.

Graphcore, Starling are all mooted as future IPOs or buy outs.

-

Rev Beauty

There are even upsides valued at zero in the Net Asset Value figure. CHRY is pursuing legal action against Revolution Beauty. This is based on what CHRY say were inaccurate statements given prior to CHRY investing in REVB (which it did at great loss).

CHRY on 22/04 updated on its REVB claim and said “a claim of £39m, together with a claim for consequential losses of a further £6.2m. The Company considers that it has a strong case and is willing to pursue it.”

If it achieves that that’s £45.2m or an extra 7.5p per share

WeFox is “in Trouble”

The reason for a recent fall in CHRY’s share price is a boardroom battle. Sky News on the 16th May released a scoop that WeFox faced bankruptcy. Clearly that paniced markets.

The Sky News article stated WeFox circulated a letter earlier this month to its investors, but CHRY reported that in fact they’ve been in talks with WeFox for much longer. The recent appointments of a new Chief Risk Officer and new CEO replacing the founder clearly are being driven by investors. CHRY go on to state “A plan has been put in place to simplify wefox's business model to drive the company towards profitability. Following these conversations, the Investment Adviser believes there is a route to ensuring a successful outcome for wefox and Chrysalis's investment.

In recent weeks, wefox has raised approximately €20million from shareholders, to which (CHRY).. contributed €3million in support of the aforementioned strategy; the (CHRY) Investment Adviser continues to consider how best to support wefox achieve its ambitions and is confident of continued shareholder support for the company, if required.”

So CHRY reducing its holding by 1/3 suggests that there's a 1/3 chance of failure, or more likely that there’s going to be a 1/3 dilution. Because if bankruptcy were certain CHRY would have written it down to zero.

The WeFox CEO Mark Hartigan says "The opportunity to rebuild through restructuring and any optionality for the future remains dependent upon reaching [a] sustainable position by balancing cashflows with the timing of our planned disposals," Two weeks ago it appears WeFox has already disposed of its Italian business according to the Coverager - so it's already making progress it seems.

But it everything as it seems? Or is the CEO doing an “inside job” to panic the market? As revealed by Donald Pond on Pond Life - Mark Hartigan attempted to panic LV (London Victoria) into a sale back in 2021 to a PE house where he would personally benefit. The article reveals Hartigan allegedly stands to receive £20m if he can force a sale of WeFox in 2024.

So next month’s update on WeFox may contain some interesting commentary. Let Battle Commence!

Conclusion

There are multiple upsides to CHRY and while the WeFox battle is a distraction the fear of imminent bankruptcy appears to be false.

But even excluding WeFox, yes excluding 14.4% of the portfolio, the remainder is at a serious discount to NAV…. 36.7% discount to be precise.

That’s before the fact that Klarna, and others offer upside to the NAV and nearterm prospects for realisation.

The sea of green in the chart above shows uplifts while red shows downshifts. The sea of green - like that in a Swedish landscape - should provide Klarna-rity to investors that CHRY is too cheap, regardless of WeFox.

Regards,

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings even those held in VC stocks might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"