CMC X

What's the story behind the triple bagger?

Dear reader

The first item on CMC’s investor’s page that catches my eye is earnings per share fell from 24.6p in 2022 to 16.7p in 2024. and 16.7p puts it on a P/E of 20, at current prices.

So let’s zoom out and we see 105p at 31/12/23 was a ~80% fall from its price in 2021. So this is an overdone fall from grace thesis. Great spot by Mr Scott.

The descent in 2023 doesn’t appear justified, and even with earnings falling to 14p a share (at a ~£1 share price) that left it at a P/E of 7 at 31/12/23.

Which is as cheap as TP ICAP is today as it happens.

As at 31/3/24 CMC had £717m of assets, including a mere £29m of intangibles and £29m of property which gives this £659m of liquifiable assets and £688m of tangible assets. While liabilities totalled £313.4m giving net assets of £403.5m and net tangible assets of £374.5m. The market cap is now 3.2X its working capital after being less than 1X at the start of the year (which was also Mr Scott’s value thesis)

Count their ‘eds

CMC has a headcount of 1,175 and had employee costs of £118m which is almost precisely £100k employee costs on average. That’s actually quite low compared to TCAP where employee costs are £1.4bn. But £1.15bn are broker costs. 2,467 brokers earn on average £467k per year. Excluding those the remainder earn £92.5k on average. But what about HL for example? Is that a better comparator? HL generate £750m of sales so about 2.5X more than CMC - but deliver that with 2,404 people costing £200m, which is just £80k on average. Put another way HL generates £4.2m of sales per £1m of employees, and TCAP generates £5.2m while CMC generates only £2.8m, per £1m of employee costs.

Given that CMC now want to compete against the likes of HL the comparison is interesting. CMC appears less efficient than its peers based on employee costs so the cost cutting announced sounds like it is needed.

Sales and marketing spend is broadly similar between HL and CMC but of course HL is largely defending its (large) market share while CMC is attacking.

Interest Income

What struck me, particularly, was the huge disparity between the CMC and TCAP business models. TCAP doesn’t hold and manage client funds while CMC does. It earned a net £33m interest income of which £24m was from income on client funds.

But then HL’s accounts made me take a breath. Their interest income from clients is £266m makes the £24m income from CMC pale. HL appears to have a natural £242m income advantage over a newcomer. The difference is greater when you consider only £9.4m of the £24m is “Investing” (vs Trading) funds….. so the difference between them is 30X more than CMC!

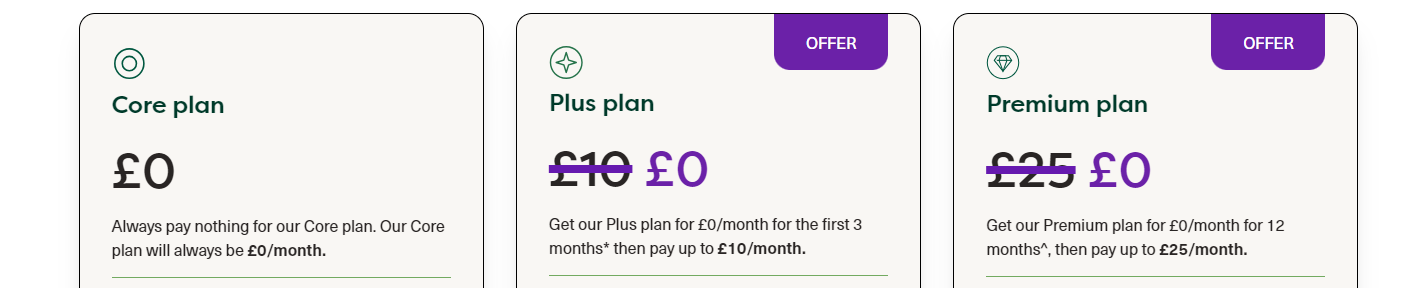

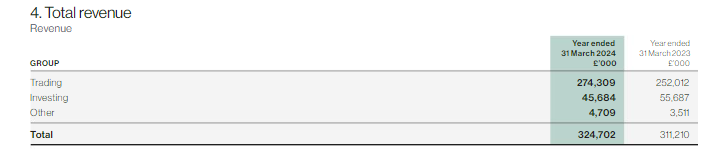

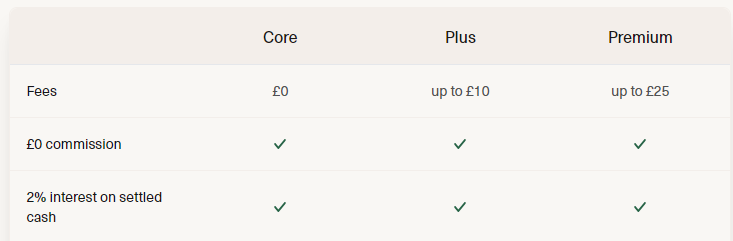

Also it’s noticeable that CMC’s investing revenue fell nearly 20% in FY24. There is no explanation given for this in the annual report, but I think this is because (looking at their web site) CMC offer a flat rate, no commissions and an introductory 12 months…. FOR FREE! See below.

It’s great that they are being so aggressive to win new customers (I’m a bit tempted to take 12 months for free, and I’m sure other readers would be too) but how exactly do you grow profits when you are giving away your service??! Zero commission too.

As a potential investor I’d be concerned about the FY2025 results. Will punters remain after 12 months or will you get “tarting” as punters move on to the next special offer. (The Oak Bloke has earned several thousand pounds moving from one Broker to another over the years, taking advantage of such incentives). Will a loss leader be a short term loss and a long term gain - or just a short term loss?

Investing revenue is down nearly 20% year on year.

Confusingly (least I think so) CMC markets (the “trading” arm) has no links or reference to CMC Invest (the “investing” arm). The web design in my opinion is odd, and I’d have concerns about something as basic and simple as this. £35m spent per year on sales and marketing and the UX experts haven’t thought about this. Poor.

Revolut

The partnership news last month led to an 80p jump to 332p of CMC’s share price. Not surprising, because Revolut has 40m (and growing) users.

CMC said Revolut customers would initially be offered foreign exchange, index, commodities, treasuries and equity CFD.

Of course Revolut has offered US share services, Precious Metals and Commodities since 2018 via DriveWealth and European Bonds via GTN earlier this year, so this partnership isn’t either exclusive nor new. Nor a new area for Revolut, but it is said Revolut may extend the relationship with CMC. It isn’t clear whether CMC replaces DriveWealth for overlapping services (commodities) or GTN for Treasuries (Bonds), or whether the agreement will apply only to certain territories? For example DriveWealth (an American provider) perhaps cover that territory and CMC perhaps covers Europe. Also what is not clear is what sort of deal has been struck in terms of revenue share and profit.

Being a simplistic soul, the 2024 net profit of circa £45m needs to grow by around £15m (i.e. 1/3) from this Revolut deal to support the recent 1/3 rise in stock price.

It is speculative at this stage whether this can and will materialise - or when. In fact nothing of the sort IS forecast.

Outlook FY2025 “Higher fiscal operating income”

I notice there are forecasts for FY2025 of £320m-£360m net operating income. This “higher forecast” is between 3% lower and 8% higher than FY2024 (y/e 31/3/24). So not higher perhaps.

The RNS also speaks to a 52% jump in adjusted profit of £80m. But there is no “adjusted profit” in the annual report or on the CMC web site, nor any mention of an £80m adjusted profit anywhere. It’s very frustrating and again why is no one doing due diligence to say the “adjustment” is X,Y and Z. Poor. Actual PBT increased 21% and actual Net Profit by 13% so where is there a 52% “jump”?!

I then had a re-read and made a jump of my own. The 52% appears to refer to the outlook news where a £320-£325m outcome would be £95m and £95m forecast profit for FY2025 is around 50% higher than £63.33m FY2024. Extremely poorly worded and presented and muddles the past and future accidentally or otherwise.

The outlook goes on to speak of a forecast cost base of £225m excluding non-reccurring charges and variable remuneration. But has anyone stopped to think what were the FY24 non-recurring charges and variable remuneration?!

The answer is £30m (£12.3m impairment charge & £17.7m variable remuneration). So costs in FY2025 could be possibly £225m + £30m = £255m and possibly more (since they speak of cutting costs and reorganising - those usually drive non-recurring costs, don’t they reader).

The outlook also speaks to further technological upgrades planned for FY25. CMC’s IT costs increased 18% in FY2024 to nearly £40m. Upgrades drive non-recurring costs too, as does partnerships which drives increased usage.

So a possible £320m revenue and £255m costs results in a PBT of £65m (which is just £1.7m more than FY24) and at £3.35 a share a P/E of 20 in FY24 that remains a P/E of 20 in FY25.

Or when that becomes clear the P/E returns on the disappointment to say a more reasonable P/E of 10 which would mean CMC would halve in price in the next 12 months.

Conclusion

That possible halving of the share price is purely based on interpreting their own forecast numbers, nothing more. I don’t know that that will happen, and I would hope it didn’t. But I struggle to see it rising much from here, unless and until Revolut drives serious volumes of new customers profitably (i.e not for free for 12 months - but then why use Revolut and not the free “Powered By” option?).

I appreciate I said CMC seemed expensive a month ago, before the Revolut news. Then it rose some more.

But I do think this share has been packaged up and presented in a very flattering light. There are some serious questions shareholders should be asking here. The Revolut partnership news gives it a giddy je ne sais quoi while it’s not clear what actual profit this will deliver, and how it fits with other existing share services delivered by Revolut’s partners for up to 6 years.

It’s not clear what, if any, IT costs will need to be spent to support any kind of ramp up of volumes. I know to keep availability at 99.95% isn’t cheap, and the cost can be non-linear as volumes rise.

The very aggressive pricing of its Invest services is either too good to be true and there are some hidden charges - or it is too good to be true…. for customers. But only good for patient investors, who don’t mind short term pain for long term gain….. assuming those customers remain loyal after their free 12 months.

Comparisons to peers like Hargreaves Lansdown illustrate to me that carving out a larger “invest” business isn’t going to be as straight forward as perhaps some imagine. Incumbents in a market do have advantages and war chests too.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

It seems that all the brokers that allow crypto trading are making money from this bull market. IBKR is up 40% in 3 months, Robinhood up 70%, Schwab up 20%.

I think the UK listed ones like IG, CMC and Plus 500 will also be doing well.

What do you think about its competitor Plus500 (PLUS.L). Plus is growing much faster and paying nice dividends and buybacks.