DEC-ent offer?

DEC-ent offer?

More Financial Wizardry from this OB20 2024 share pick?

Dear reader

In the long vs short tug’o’war ‘gainst Snowy-capped nemeses and sub 5% weak-handed M&Gs how do you get more people to join you in the pull against a shorter?

Answer: get the market on board.

I think the key point and genius move today is Rusty is NOT inviting any DEC-hands to abandon ship. For those confused and wondering what’s the right thing to do - the way to think about it is this.

Assuming you bought DEC for anything over £9 (or haven’t yet averaged down to a such a price!) and I suppose plus whatever price you think it might reach by March 28th) the OB suggestion is choose to get your dividend. Don’t tender.

If of course you feel the ship is doomed but you haven’t sold here’s your chance to part sell at a higher than market price.

If you are a new DEC holder i.e. your buy is £9 or below (like my sister is) or you’ve averaged down then you have a chance to bank some profit.

But the tender is especially aimed to if you are not a DEC shareholder, yet, then consider Rusty’s offer which is this:

You have 2 weeks between now and the 1st March to decide whether a guaranteed boost to your return for investing and to tie up your capital for 28 days from 1st March is worth the risk. i.e. The risk that the share falls below £9.00/share.

If you consider the risk of it falling lower (substantial resistance below £9 has been apparent despite Institutional selling and active shorters) then your rationale is then to consider this. If the share price is flat can I get my money out and earn a return at low risk? And what if there is any kind of appreciation?

To consider the risk that “somehow” a company which is able to afford a $42m dividend and has just reported 2023 adjusted EBITDA of $545m for 2023 and a $200m SPV at 6 x EBITDA, and whose share price has plummeted by what analyst after analyst (Stifel, Berenberg, Cavendish) calls a slanted and misinformed shorting campaign based on half truths and omissions. A boosted and guaranteed return for 28 days plus whatever share price momentum occurs between now and then.

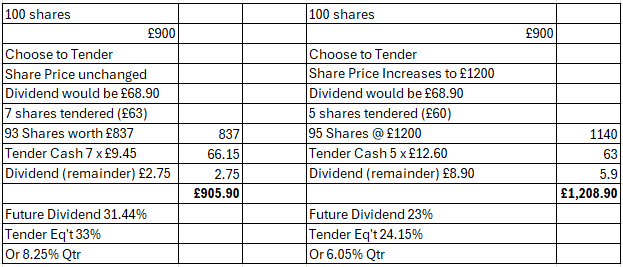

If such a person buys 100 shares today then this is what they can expect.

(I’m using an FX $:£ rate of 1.27:1)

The first scenario is a flat price. They gain a booster 1% to the value, even after receiving back £72. So it’s worth 8.25% for 28 days. At that price you could leave the rest of your capital in or take it out.

The second scenario is even more juicy. They stand to earn 34.6% where the returns are boosted by that tender.

But what’s in it for DEC-hands?

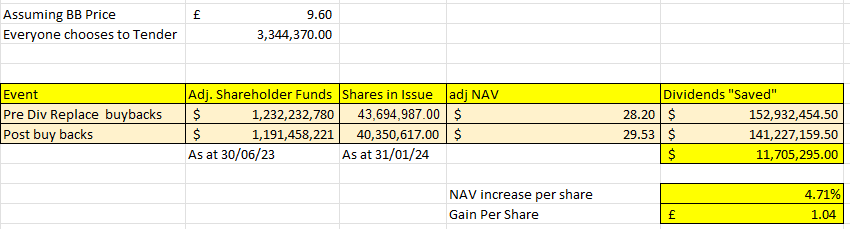

Well if 100% of people elected to tender then the accretion of value for all remaining shareholders is huge too.

The $42m buy back assuming a flat £9/share and a £9.60 buy back looks like this. A £1.04 gain per share.

Now it is wildly optimistic to expect 100% to walk the plank even with a 5% bonus treasure to ease their passing.

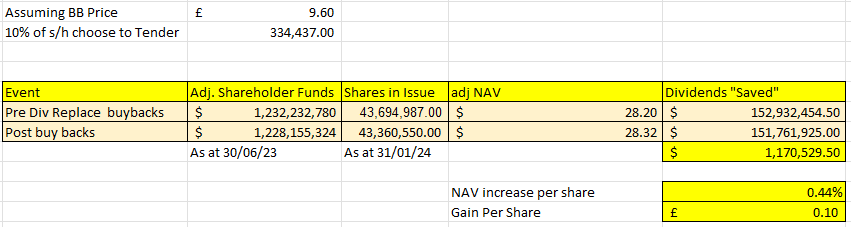

So let’s re-run that with just 10% of shareholders opting. It’s still a 1% of the share price gain in NAV and over $1.1m a year saved in dividends.

Remember too reader this tender could be EVERY QUARTER going forwards.

If it is (and why shouldn’t it be?) then for the weak-willed short termers there’s a ready way to get the cash back out reasonably fast at a premium (over a year a 1/3 of your cash even at flat prices - even if you don’t sell).

For long-term DEC hands at a 10% of shareholders opting a tender, that’s $5m of divis saved, £0.40 of NAV added per share …. PLUS 90% of shareholders received a 31% yield at today’s price.

In Decibels-and-Decimals I explored the “either/or” and asked DEC-hands to vote. Ructions ensued. Even the voting methology was called into question. It felt like Brexit encore.

But the genius which is Rusty has seen a way to give “both” - each choose - and either way no one shall lose - and indeed all shall gain - ‘cept those shorters.

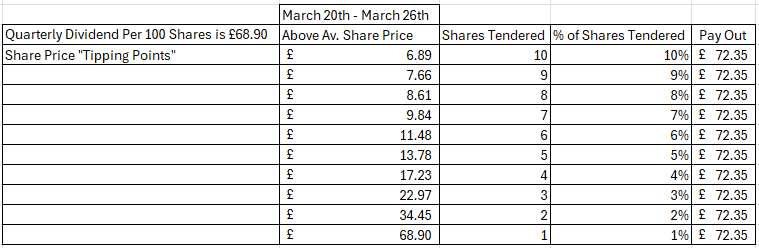

The wrong-footing of shorters is compounded by the double boost of the 2023 Annual Results arriving 19th March, as pointed out by one my readers, John Gove. The window to get on board DEC will have past for the tender offer but if you feel optimistic about the contents of said report (as well as the 2023 sustainability report) then it’s reasonable to think that for the period of time after the 19th the share price will rebound strongly. If that’s the case your tender might only be fewer shares to give up

John’s comment made me think about tipping points. Whilst £68.90 might be fanciful the idea of getting to £11.48 or £13.78 by end of March on strong results isn’t unrealistic. So if you anticipate a price rise you stand to sell 5% of your holding but gain a bonus 1% for doing so.

In other words the pay out under all these price scenarios is the same - but the shares given up differ.

If they’ve got any common sense, the shorters are already reading their opponent’s article - people like the Oak Bloke. This is a further calculation to consider whether you should decide to close the short. Will we see a strong recovery in the next 6 weeks? Does an extra 1% give it an extra tickle?

This subtle (it’s costing DEC a minimal amount an extra $4.3m if there’s 100% take up) to do this wizardry - beyond the usual dividend cost. But it’s another reason I consider DEC such a fantastic investment. But it’s just my opinion :) and this is not advice.

Oak

PS it is my understanding of another benefit to the tender is if you are subject to a 15% or 30% deduction due to the W8T, then that’s another reason to consider the tender. 33% annualised vs 21.7%.

PPS SIPP holders have a 0% deduction so long as hold with a decent broker (e.g. HL, II) and register as exempt.

The results will be good as updates throughout the year have been as expected. Exceptional leader with a great team of staff. The business is so transparent and repeatable. Hedged revenue, superior cost control , ahead of the Industry on ESG with innovative financial options. Grossly undervalued SP. Once in a lifetime yield/ investment opportunity. PI’s take the dividend. Ii’s or those wishing to sell take the offer and get out. This business isn’t complicated. It’s easy . Rinse and repeat acquiring cheap assets , smart asset management and cleaning up the mess others can’t/don’t want to do. Right Business at the Right Time. Keep going Rusty.

In the increased share price example, should it be 5 not 7 shares tendered?