DEC-sent predictions?

Is going short working for the shorters? Performances analysed

Dear reader

Some shares get shorted to the extent that the shorter must eventually declare their hand. This is at 0.5% of the shares in issue. In the case of DEC that means £2.63m of shares, based on Friday’s share price.

This gives, for example, DEC-hands an opportunity to examine their nemeses (no snowy pair are participating in declared shorts, mind….. perhaps they took a shine to DEC and went long instead - they managed to create a wonderful entry point after all!)

I once wrote flippantly “the shorts will melt away….”. And they didn’t. They persisted. A reader pulled me up on this and said they haven’t melted and they aren’t melting. I admitted I’d presented an opinion as a fact. But I did feel it was inevitable…. after all surely these shorters know when they are beat? Surely they need to cover their short?

Eventually.

So that got me thinking. How successful are these shorty folk anyway? With DEC? And generally. Why do they stick around? Are they profiting from their 0.5%+ shorts? Or are they averaging up to try to limit their losses, hoping, hoping (perhaps praying) for an eventual DEC-sent to breakeven their losses and to fulfil their downward desires.

LIMITS TO MY ANALYSIS

I’ve used Morningstar data and the closing price. Where shorters have added or reduced a short I’m simply capturing the event date where they had a declared short vs Friday 5th July 2024 close price. Obviously I don’t know what time they bought their short, and the precise price bought, so if there was variance within a day this analysis won’t show that. I’m including the cost of covering the dividend with DEC for obvious reasons (i.e. it’s expensive to hold a short position and then cover the dividend if the dividend is chunky). I’ve not sought to do the same courtesy for ASOS and JD Sports etc. You go and do that bit of the analysis if it matters to you.

Also some of these shorters have thousands upon thousands of disclosures. Do I have the tools (and time) to methodically work through every row of data? Do I ‘eck! So this is in some cases sampling only.

But the analysis proves interesting reader. Read on reader, read on!

Arrowstreet Capital 0.82% of DEC shorted

Arrowstreet based in Boston, MA say “We are a team of researchers, technologists, traders and professionals who have come together to design a systematic investment process that aims to add value across market cycles.”

Sounds impressive! But how do they perform?

So some wins and some losses - a big win on Ascential - 50/50 success elsewhere. A very new short on DEC, so they’ve not experienced the pain of covering dividends and seeing robust FY23 results or Q1 results. Maybe they have that experience yet to come.

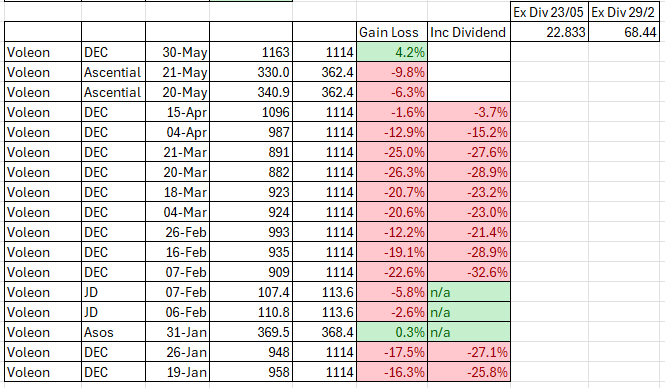

Voleon 1.41% of DEC shorted

The Voleon Group say they are “committed to the development and deployment of cutting-edge technologies in investment management. Our innovations in machine learning serve as the cornerstone for our success in applying rigorous data-driven techniques to financial markets.”

Sounds like a terrifying opponent! But how do they perform?

When we look at the numbers I think someone might be in for an almight rollicking and perhaps need to accept they made a mistake shorting DEC?

1.41% of stock shorted is £7.4m and at what looks like a 20% average loss that’s about £1.5m loss maybe? OUCH!

If DEC returned to about £9 a share they’d break even, or if they bought another £7.5m of stock they’d average up to break even at a £10 share price maybe?

Next DEC Ex Dividend is about 53 days away (29th Aug). H1 results are the same day. Have a think Voleon, is it time to melt away? Soooo long.

Other shorts appear to be losing too. For example the short made on Ascential appears to follow Arrowstreet but they arrived too late so rather than a 31% gain there’s a 6%-10% loss.

Millennium International 0.8% of DEC shorted

These say they stand for “Independent decisions, collaborative culture, united mission”.

I do wonder whether these shorters make independent decisions or whether they follow each other into shorts? There’s patterns rapidly emerging where there’s commonality of stocks being shorted. Like sharks attracted to blood - it would be natural to do so. But is such pack behaviour be definition “independent”? I think there’s the danger of an oxymoron creeping in there. Philosophy aside, these have thousands of short disclosures. I decided to pick some at random (including all the DEC ones).

Another loss for Millennium regarding DEC but these are new shorts. Otherwise again a 50/50 performance - with some notable achievements. Liontrust and Burberry appear to be “good” shorts with consistent falling share prices. Help me reader, I just referred to shorting as good. I’ll be joining the dark side if I’m not careful.

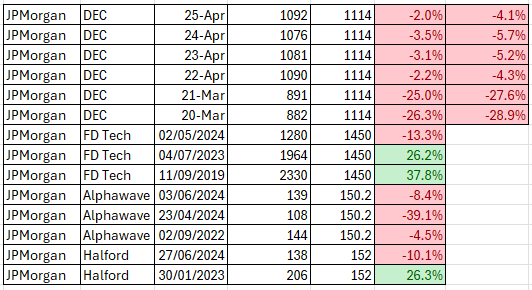

JPMorgan 1.7% of DEC shorted

No introductions here needed. Will this be a bit short or will it be “the Big Short”?

I’m going to pick their top 4 shorts (by percentage) which are FD Tech, DEC, Alphawave, Halfords. Let’s kick the tyres ha ha.

An average 15% loss on its 1.7% holding is a “mere” £1.3m loss.

The final column is the loss considering covering the dividend

As for other shorts again several thousand entries, but in my sampling it appears JPM might stick with a short for years and years, it seems, and they’ve been right 50% of the time, but do not appear scared off by losses. Will an estimated £1.3m loss melt ‘em? Possibly not.

Bridgewater Associates

Bridgewater Associates say they are “a premier asset management firm, focused on delivering unique insight and partnership for the most sophisticated global institutional investors.”

Unique? Well shorting DEC is not unique. Back to the pack theory and the oxymoron, I’m afraid.

Of course for those who don’t know the famous Ray Dalio founded Bridgewater. I would commend Dalio’s video how the economic machine works for any DEC-hand who wants to better understand economics in a highly accessible (and dare I say entertaining) way.

Bridgewater only have 1 open short - DEC - and I get a sense this is going to be another sea of red, but let’s see. What is interesting is shorts appear to be closed off more promptly - compared to JPM who persist despite losses.

Yep red. 0.92% is £4.8m of stock and an average 9.8% loss is £0.5m lost so far. Ex Dividend data in 53 days and covering yet another dividend is another £0.1m to add to their losses.

Unless they melt?

Walleye 0.79%

Roughly speaking looking at the short declaration dates Walleye is in the red by something like £0.5m as well. A 0.79% short declaration is about £4.1m of stock and whilst they shorted 4th Jan (so quite early after the short report), their subsequent buys are underwater by £1-£2 per share.

Adage 0.66%

Now this is interesting. What about shorters who shorted back in the days of pre-consolidation and when the share price was at £1.00-£1.30 (before the 20:1 consolidation). They have 40%-60% gains don’t they?

But a shorter’s gains if they didn’t close the short they have to cover the dividends - so who won in that scenario?

Adage won.

But they’ve lost a 1/3 of their gain since this year’s lows. At around £9 in February 2024 they would have booked at 42.5% gain even after paying dividends since November 2022.

Will they bank their 27.6% soon or possibly watch it dwindle to a loss?

Conclusion

Whilst, factually, the reader was correct to say shorts were not melting away, when I said they would be - and I fully expected they would.

It is my opinion that they still shall. Their persistence makes no sense when you look at the facts.

With the smart deal making acquisition of Oaktree, the refinance, the retreat of Honorable Pallome, the robust profit outcome of FY2023, the robust cash flow, the strong hedges well above the price of Henry Hub, with the enormous achievements in methane emissions, with a general acceptance by analysts that the Snowy pair’s report contained shall we say inaccuracies (decorum est loqui verum).

When you look at the shorters’ likely losses, based on declared dates, their tactic to sink DEC backfired. The question now is how many more losses do these want to endure? How long until they switch to new prey like Burberry and Liontrust who actually are falling in price?

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

Thanks for that article, Oak. BTW, according to IBKR data (which is the source of the following website), the fee to borrow stands at 8%+

This fee to borrow varies daily, is based on share price, and is calculated pro rata per day. The fee is adds to the losses in addition to Dividends and 'true losses'. https://www.iborrowdesk.com/report/DEC

Interesting article looking at the numbers. However, are shorts a human analysis of fundamentals or a bot driven analysis of historic share price which then infers a future trajectory? If the former then perhaps some melting shortly due. If the latter, then closing decisions may be lagging economic performance by a period - until algorithms work out that SP is now on a differing trajectory.

Additionally, no one likes to admit they’re wrong so that builds another lag into closing shorts - I know, I considered selling DEC at £1.40 but didn’t!

Individuals might be waiting for a balancing profit elsewhere to enable closing of a short with a profit across both trades.

A further possibility is that the shorts are a hedge for IIs with big holdings to cover downside losses.

It’s all a bit more complex than does the short make sense in isolation 😀