DGI9 FY23 update

DGI9 FY23 update

Naughty NAV - stop growing! You're meant to be declining by 75%!

Dear reader

This week’s update from DGI9 gives us clarity on the NAV and progress - good and bad.

The BAD

The sale of “Verne Global” (book value £441m) which comprises of Verne Global London (previously Volta), Verne Global Finland (Ficolo Oy) and Verne Global Iceland has completed and now reviewed by independent auditors. (That’s good not bad, the bad is yet to come).

The sale was for £327m plus a deferred payment of £19.5m in April 2024, and a further “up to” £107m by 2026 subject to hitting undisclosed targets. That adds up to £454m. Goody, goody a 3% premium. (But that’s good too… keep reading the bad is coming next)

Sadly, the wash up of this transaction is that a series of unexpected costs due to “the complexity” and a disclosure that the earn out of “up to £107m” actually means about only getting half the earn out (i.e. £52.91m). So a loss of 12% not a gain of 3%.

NB Is this actually just a write down of £54m based on prudence and accountancy rules of anticipating the worst - because it’s based on a forecast value? Remember we saw that there were 70%-89% EBITDA growth numbers at Verne in the final update. Makes you wonder what EBITDA targets were agreed to get the full £107m - if such meteoric increases only count for half the agreed earn out…. but we still don’t know!

Anyway here are the numbers out of the update:

It’s a little disappointing but not a 75% loss (i.e. the discount to NAV). £54.5m less than £454m is a 12% loss on disposal once all the costs are taken into consideration. And the reduction in expected earn out of £54m possibly could be reversed, so a future gain. A £54m future gain would equate to a net 0% loss wouldn’t it?

The £273.5m payment substantially reduces the RCF to a much more manageable approximate £105m comprising of the prior balance of £356m owed less £273.50 repaid plus £22.3m interest accrued. The £19.5m next month takes it to about £85.5m o/s.

It’s also worth adding that some commentators called Verne “The Crown Jewels” so “bad” might also be the perceiption. Those commentators dismiss DGI9’s other assets. But I’ve written previously about why I believe that’s wrong and have substantiated that with numbers. I’ve not seen any substantiation as to quite why Verne was so good (other than that the 2023 H2 EBITDA growth was impressive, albeit from a very, very small base)

In the next section I explain why dismissing the remaining assets is a huge oversight. The supposed bad of selling Verne masks the good.

The Good

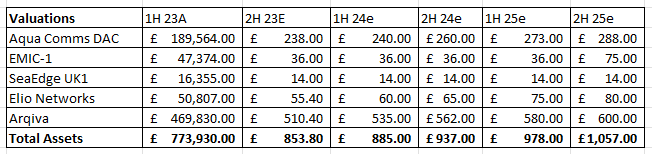

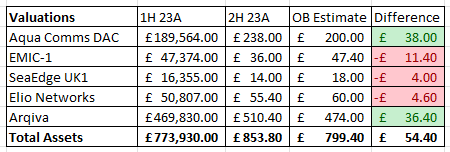

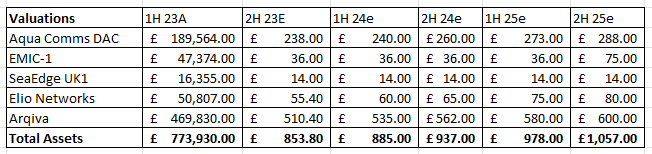

Meanwhile the portfolio has been revalued based on a sales valuation. Here are my prior estimates: (I appreciate Verne completed post period but I exclude it from the analysis for 2H 23)

This is how close I got. So while I anticipated an increase at Aqua based on what I’d read about data carriers and the value of its transatlantic cables (see my OB 136 article) I’d expected just a 5% gain. Instead we see an over 25% increase in the asset value in 2H 23. This will probably be in recognition of the new AEC-3 subsea cable and growth of traffic. We know underlying EBITDA excluding the back haul licences is very strong too.

It’s not surprising. Total international internet bandwidth demand now stands at 997 Tbps, representing a four-year CAGR of 29% worldwide. This report tells us the CAGR for connectivity with Asia and Africa (i.e. the EMIC1 cable) is 40% not 29%.

Despite this, EMIC-1, the holding for the cable linking Europe and India drops in value in 2H FY23. The value held is WIP (i.e. at a discount) and once it’s operational next year I believe we’ll see a similar uplift as we’ve seen for AEC-3 - as I anticipate in my FY24 & FY25 valuation estimates. But for now they’ve decided to reduce its value (without any explanation at this stage).

Similarly SeaEdge also reduces, even though we saw its cashflow increase by RPI (13.5%), once would think enhanced cash flows would enhance the asset not reduce it. Again no explanation for the cut, apart from “an Estate Agent gave us a quote”.

Elio increases but by a smaller amount than I’d anticipated. But a 9% increase reflects growing value - and it’s not a 75% decrease is it?

Finally Triple Point confuse the RNS quoting Arqiva net of the VLN. If you strip that out we see my assumption of a 1% increase is much higher. An 8.6% increase or £40.6m is impressive - and it’s not a 75% decrease either is it?

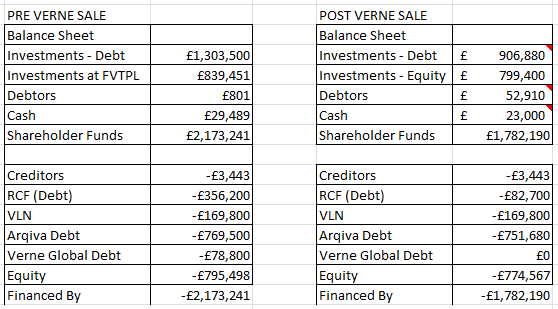

The BS

The balance sheet begins to simplify and we move far back from a “Saietta-like” debt cliff edge. The “investment - debt” is now the estimated share of debt its portfolio company Arqiva has, and this is offset by the debt at holdco (the VLN) and the opco (“Arqiva debt”). So £82.7m RCF almost equals debtors & cash while the portfolio at £799.4m vs market cap of £194m - and there’s the 75% discount I keep mentioning.

Earnings

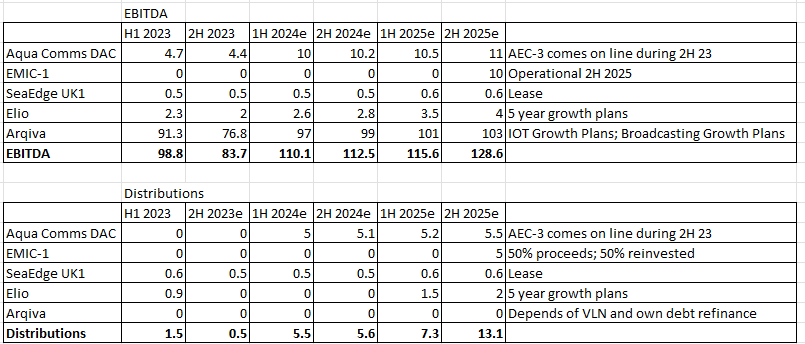

We know from the trading update the approximate EBITDA for 2H 23 which were broadly in line with my own estimates. I extrapolate the earnings out for FY24 and FY25 (whether DGI9 will sell or IPO these holdings before we get there is another matter)

Out of the earnings I also calculate the returns to DGI9. While 2023 offered very little return in distributions that changes in FY24 as the assets mature and earning 5X in FY24 and 2X in FY25. Nice!

Notice I assume Arqiva do not make any distributions and focus on paying down debt instead. There’d be more X’s than a Castlemaine Lager if Arqiva made distributions too!

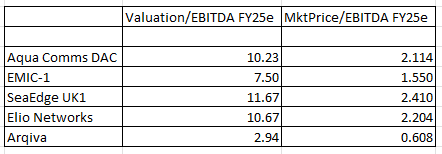

But what I find interesting is if I take the forecast EBITDA and divide that by the forecast valuation (i.e. the ROA or return on assets ratio) we see a ROA ranging from 2.94 to 11.67. I would argue that those valuations are cheap (appreciating that the ROCE for Arqiva is 8-9 due to debt).

But if I take the current market cap (£194m) and divide that in ratio to the assets e.g. Arqiva £520/£913m then in PE terms 0.6 to 2.4 is incredibly cheap.

More realisations

If the valuation for Aqua Comms, EMIC and Sea Edge are realisable based on the 2H FY25 forecast valuation then not only are investors left with Elio and Arqiva, but the NAV per share grows to £1.57, nearly double today’s NAV. 8X today’s market price.

The Risk (?)

Now that the risk of Verne has disappeared, and the debt is substantially paid down, and cash flow rising, the remaining risk is simply the ability to realise assets at sensible prices, as DGI9 continues its (unfortunate) wind down.

Conclusion

Whichever way I look at this the 75% discount is a nonsense. The fact that the share price did not budge on the news of the H2 valuation INCREASE

(NB: the valuation was based on the assets being valued for sale)

…as well as the EBITDA INCREASE announcement, as well as the succesful realisation of Verne and cash INCREASE (debt decrease) speaks to a disconnect on the price.

These assets are plays on the growth of the internet, data and AI. Is the market asleep to the fact that AI and Nvidia are shooting the lights out in its progress and financial performance? In other words these assets are backed with gusting tailwinds.

Hold on to your hat because I believe the market will come to recognise this and suddenly DGI9 will not be 75% off.

This is not advice

Oak

Does DGi9 have the "rights" to Arquiva's cashflows? I mean the rights and not, "the potential". Even as a minority shareholder? This is direct from the June 2023 update, and I have asked the chair for clarification on this: "Accrued interest must be repaid in full before distributions can be made to the Group. After the fourth anniversary of the VLN, the Group can only receive distributions if the entirety of the VLN principal and any rolled up interest has been repaid in full. The Company expects Arqiva’s future cashflows to cover D9’s VLN interest payments.""

Hello,

I hope you don't mind if I politely ask a few questions. I am a holder of DGI9 so am quite vested in the company sorting itself out and unlocking the value. However I wanted to dig into your report(s) a bit, so please see the below as constructive challenges, rather than chippy nit picking :-)

I notice you say the Verne valuation was "reviewed by independent auditors" - that seems a stretch, as the report clearly says the NAV and all valuations are "unaudited"?

I also am not 100% sure about your numbers?

1. The Verne NAV at June23 was £473m, so how do you make £454m a "3% premium"?

2. You don't seem to incorporate any Future/Present Value of the earnout. Specifically, the full earnout of £107m would discount to around £76m using DGI's 11.8% discount rate. You need to use this number to compare apples v apples and the stated NAV.

3. You seem to have missed out the £23m provision for the VAT indemnity on the Verne sale?

The SeaEdge write down was not "an estate agent gave us a quote", it was marking the asset to a real market price - IFRS13 states that you should utilise real prices where available. It seems DGI had a real price on this, perhaps this is the next asset to be sold, so was the one with the real price (versus the rest which are marked as DCF of TP's magical projections).

Can I lastly ask how you are getting your EBITDA estimates from? For example re Aqua, I don't have any visibility on the AEC-3 revenues, but will EBITDA really more than double from it going live?

Similarly how do you have Arqiva's EBITDA ramping up so sharply, given their broadcasting contracts have been renewing at lower rates? While there is growth on smart metering, it's not enough to cover the shrinking broadcasting revenues?

Thanks in advance, SP