ENRG is shocking!

VH Global Energy - approaching realisation

Dear reader

ENRG’s new investment objective is to realise all existing assets in the Portfolio in an orderly manner…. to achieve a balance between returning cash to Shareholders promptly and maximising value.

1. THE MOMENT OF REALISATION

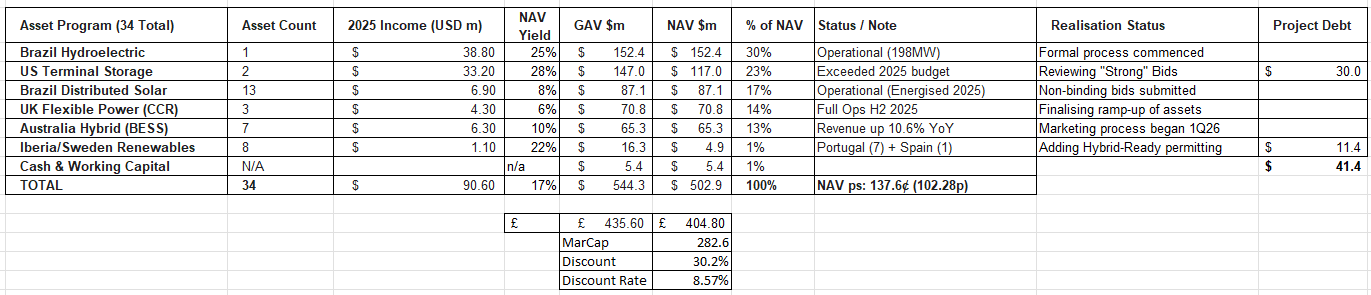

The Pivot: Following a 2025 mandate change, ENRG is a Liquidating Trust focused on maximising the value of its 34 assets for an orderly exit.

The Discount Arbitrage: With a share price of ~72.2p and a NAV of 102.3p, the market is pricing the portfolio at a ~30% discount. Management’s goal is to prove the 102.3p valuation through asset sales at or above book value.

Inflation Linkage: Over 90% of the underlying revenues across the 34 assets remain inflation-linked, protecting the NAV floor during the sale process.

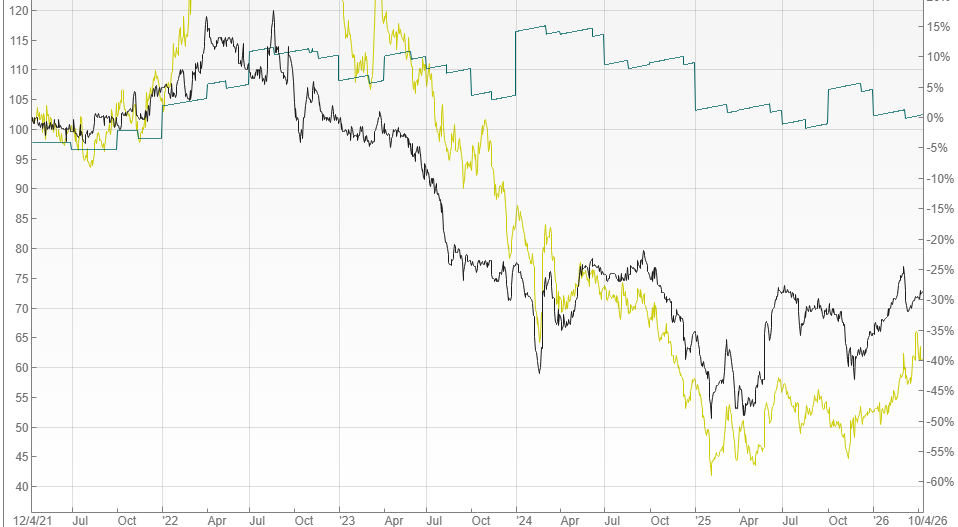

Comparing the share price in black vs NAV in blue the share trades at a -30% discount, and that discount appears to be closing.

2. THE 34 ASSETS

A. Brazil Distributed Solar Program (18 Assets)

16% of NAV

Asset Count: 13 distinct solar PV sites (grouped in the 2025/26 accounts) and planning for 5 more.

Capacity: ~75MW total.

Customer: 13 of the 18 are operational in long-term 20-year contracts with corporate and industrial users.

Analysis: These are high-yield, stable assets but are sensitive to BRL/GBP currency fluctuations.

B. Australia Solar & BESS Program (7 Assets)

Asset Count: 7 hybrid solar-plus-storage sites across NSW, QLD, and SA.

Capacity: 37MW Solar / 60MWh Battery Storage.

Role: These are “Merchant Plus” assets. They generate revenue through both power generation and Frequency Control Ancillary Services (FCAS).

Realisation Potential: High. Australian BESS assets are currently in high demand from domestic infrastructure funds.

C. Portugal Solar PV Program (7 Assets)

Asset Count: 7 solar PV sites.

Capacity: ~9.8MW total.

Status: All sites reached operational status in 1H26.

Role: Euro-denominated yield with minimal regulatory risk.

D. UK Flexible Power with CCR (1 Asset)

Asset Count: 1 integrated complex (often cited as one asset due to the single grid connection at the CCR site).

Details: Gas-fired peaking engines integrated with Carbon Capture and Reuse (CCR).

Role: Provides government-backed Capacity Market payments. This is the portfolio’s “Income Bedrock.”

E. US Terminal Storage (2 Assets)

Asset Count: 2 strategic liquid storage terminals (Texas).

Role: These are the “Crown Jewels” for near-term exit. They are non-renewable but “transition-essential” assets that generate massive dollar-denominated cash flow.

F. Brazil Hydroelectric (1 Asset)

Asset Count: 1 large-scale 198MW facility.

Analysis: This single asset accounts for ~28% of the NAV. The concession renewal (expected mid-2026) is the most significant single-asset event for the share price.

G. Spanish Solar PV (1 Asset)

Asset Count: 1 major site.

Capacity: 10.3MW.

Status: Operational.

3. PEER COMPARISON: THE “DE-LEVERAGED” ADVANTAGE

ENRG only has 7.6% leverage, and only at project level.

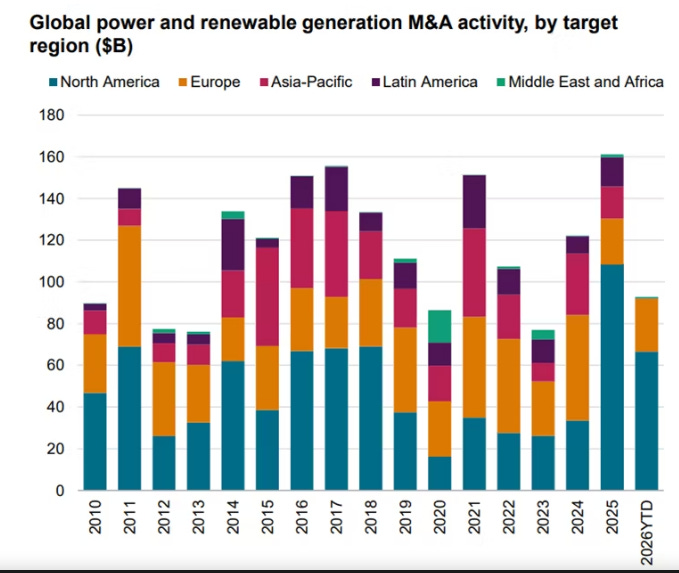

In this respect ENRG’s 34-asset portfolio is well positioned. Everything is at least partially operational. Existing bids for some assets are described as “strong”, particularly for its large Hydroelectric and US Terminal Storage facilities.

With a harsh discount rate of 8.57% applied to the assets there’s a good chance that the realisation price will be at least at the NAV price, but there’s hope for a premium - and a 30% margin of safety (in the discount to NAV) too.

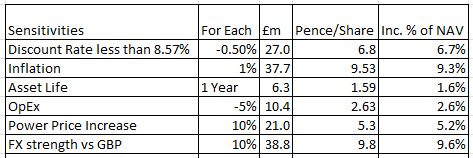

The six sensitivities to the NAV itself could be at worst neutral, but it’s likely that in 2026 power prices are tending higher, FX will be stronger vs GBP, inflation will be higher, with limited downside from higher discount rates and higher opex.

These are the potential upsides to NAV valaution:

4. FINANCIAL PROJECTIONS & CASH RETURN

The fund is paying a 5.8p per year dividend, which at a 73p buy is a 7.9% yield.

The B Share Scheme is authorised for capital returns of up to £450m (160% of the current share price), the financial trajectory is now focused on capital return rather than preserving the dividend or EPS growth.

5. INVESTMENT THESIS & RISKS

The Bull Case: You are buying a diversified 34-asset bank for 70 cents on the dollar. Assuming ENRG sells assets at 100 cents on the dollar and hands the cash back via B Shares, the “gap” closes.

The Bear Case (Risks):

1. Brazil Concession: If the 198MW Hydro renewal fails or is delayed, NAV will take a hit.

2. BRL Volatility: 44% of GAV is in Brazil; adverse currency swings can wipe out operational gains.

3. Liquidity: As assets are sold, the trust will shrink, potentially reducing share liquidity.

Update 9th April - A Difficult Market?

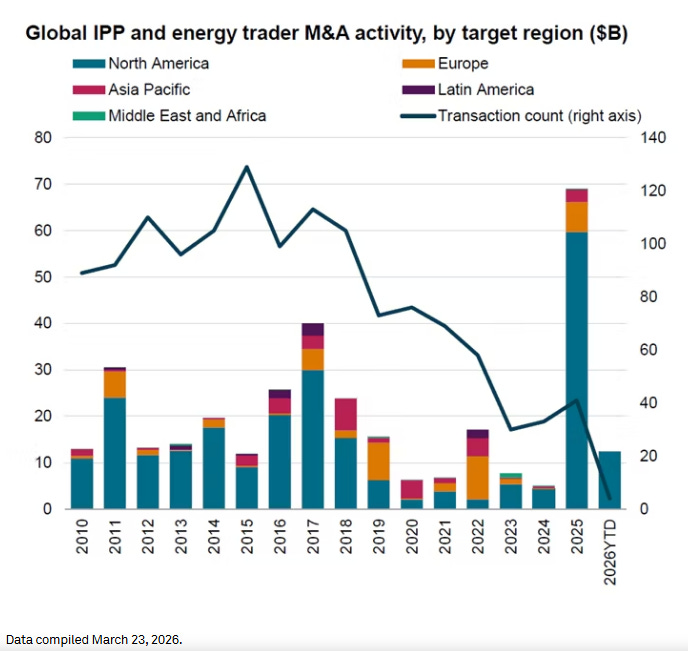

Speaking to ENRG but also SEIT since today it announced a wind down will the sale of assets be “difficult”?

According to S&P Global M&A activity is accelerating.

Conclusion:

ENRG is a high-conviction “value realisation” play in the UK infrastructure sector. The low leverage (7.6%) and 34-asset granularity provide a safety margin that make this an interesting asset realisation on favourable terms.

Regards

The Oak Bloke

Disclaimers:

This is not advice - you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Well done. Up 2% today in down market. Personally up 12%. Started buying these in December 2023 bit by bit. Tons of dividends so far. When/if the Brazil concession is sorted that will lead to decent up in the share price. Personally I would prefer if they didn't wind down or like there original spending take their time selling. Cash sat about for ages as they slowly... very slowly bought or built assets. Looked at negatively at the time but turned out they picked some great assets.

SEIT in a similar boat now!