EST is EST

Copper and Gold Explorer East Star Resources considered

Dear reader,

EST is a copper prospector based in Kazakastan. A place where you get to drive Soviet-era vans as you transport your trench samples containing Copper, Zinc, Lead and Gold and dream of instead driving Clint Eastwood to an airbase where a pair of Mach 6 aircraft lie waiting.

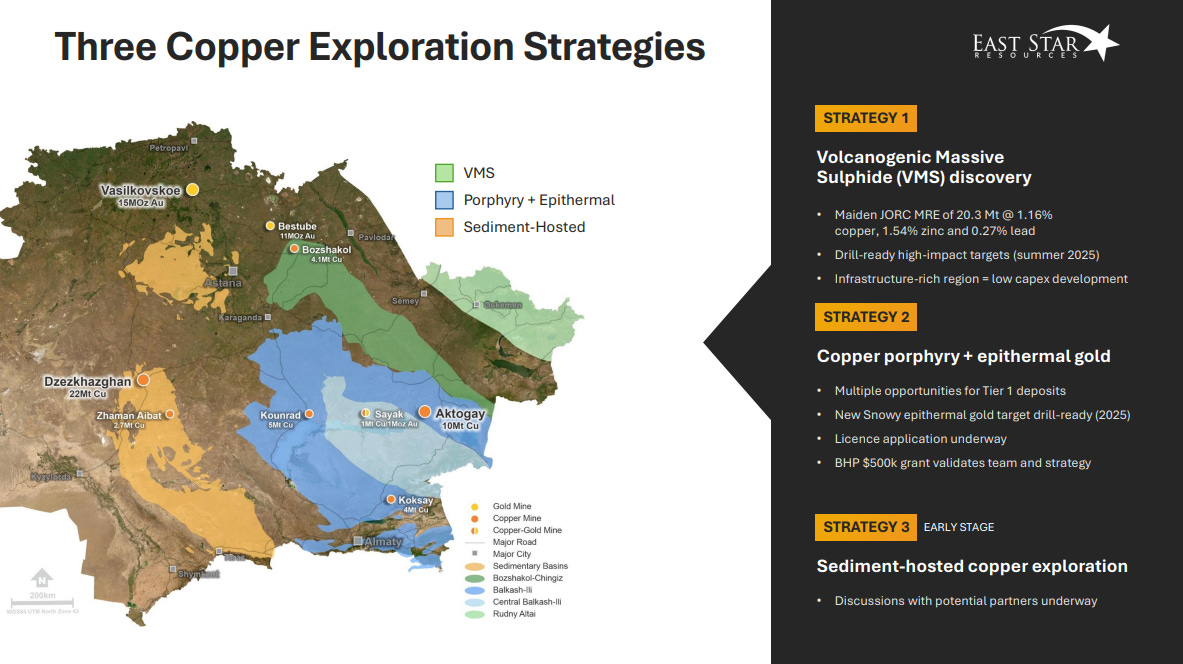

East Star's management are based permanently in Kazakhstan, supported by local expertise. The Company is pursuing three exploration strategies:

Strategy 1: Verkhuba: A Volcanogenic Massive Sulphide (VMS) discovery with a maiden JORC MRE of 20.3Mt at 1.16% copper, 1.54% zinc and 0.27% lead, in an infrastructure-rich region, amenable to a low capex development. That’s >230Kt of contained copper worth $2.2bn, >300Kt Zinc worth $0.9bn and Lead $0.1bn (at today’s prices).

Strategy 2: Copper porphyry and epithermal gold exploration targets in the Mozs, with multiple opportunities for Tier 1 deposits, supported by an initial $500k grant from BHP Xplor in 2024.

Strategy 3: Sediment-hosted copper exploration with Getech where the initial targeting strategy is at no cost to East Star.

#1 Strategy 1: Verkhuba: $2.2bn contained materials

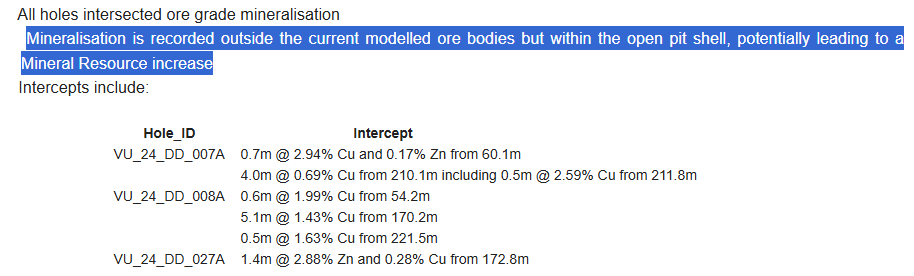

The point is EST is seeking to upgrade the MRE through infill drilling. It updated the market in February on 238 drill results as below. These results inform further drilling this summer.

It plans to drill in Talovskoye in May. The rock chip samples are pretty exciting.

Last April EST initiated a formal process for sale including a data room for a potential JV, farm-out, or sale of Verkhuba. It claims to have “significant interest”.

EST can add significantly more value to the asset and attract additional interest by advancing the resource, metallurgical test work, mine planning, and approvals, demonstrating its low cost development potential and so is progressing the project.

#2 Strategy 2 Gold

Many Gold shares has increased. But plenty haven’t. This is one. Possibly because people think of it as Copper only (I did).

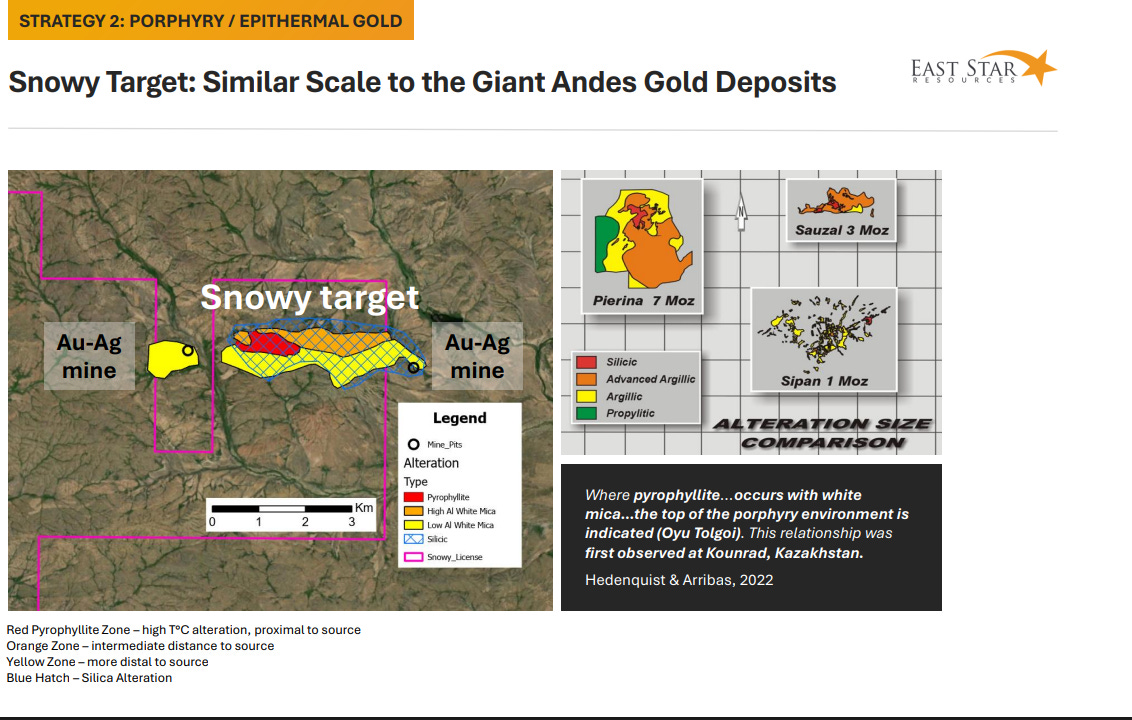

But what if Kazakhstan has geology like the Andes? Silver and Gold like at Hochschild, now a £1.6bn market cap, that you can buy for 363X less than HOC?

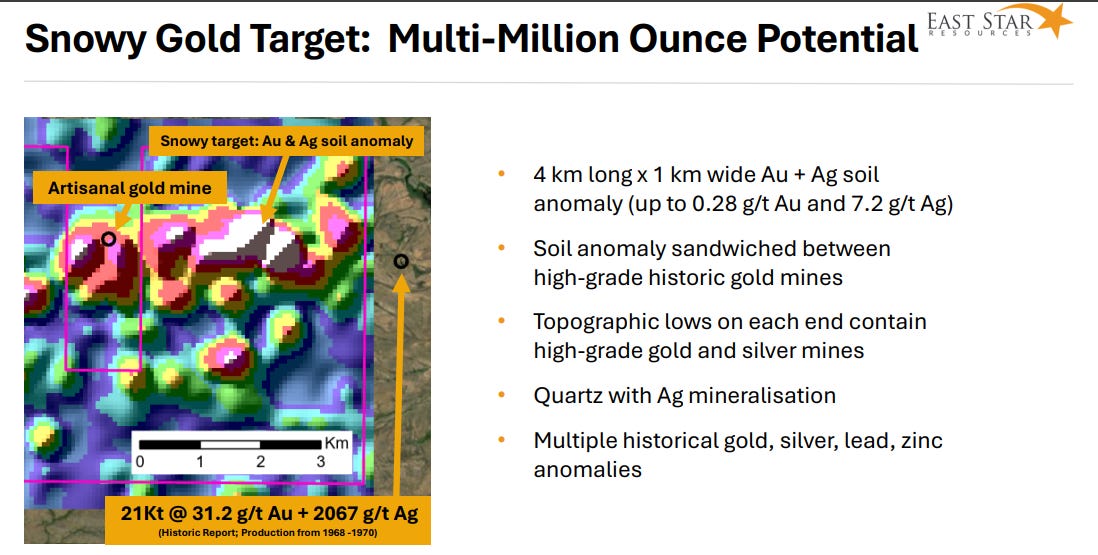

It’s very early stage and far from being a producing mine like HOC but consider this “historic report” reference. 21Kt at 31.2g/t Gold and 2067g/t Silver. Wait what?

That is $2.16bn of gold at $3300/oz. $1.43bn of silver at $33/oz. Theoretically.

$3.5bn that you get for free (if you say Verkhuba covers the market cap).

Drill testing is planned in 2025, and EST plan to acquire additional licences, highly prospective for porphyry andepithermal gold deposits.

So far EST has carried out extensive soil sampling and spectral analysis of 2,800 samples taken from the Ayagoz and Snowy licences. We were really impressed with the speed and quality of the work our team and contractors had completed. When combined with the geochemistry results, EST will have a detailed map of the area, inferring the depth of the porphyry target. The soils will also assist with the assessment of the historical artisanal gold mines around Snowy and their potential to contain larger epithermal gold deposits. The geochemical results from these two programmes will dictate the follow-on work programme and provide information that will assist in targeting throughout the rest of this proven mineral belt.

#3 Strategy 3

In February 2024, EST announced that it had entered into a joint venture agreement with Getech, a worldleading locator of subsurface resources, to explore for sediment-hosted copper deposits in Kazakhstan, which already hosts one of the world’s largest such deposits in Dzhezkazgan (22Mt contained copper). The JV is being conducted through a wholly owned East Star subsidiary established specifically for this purpose.

At no upfront cost to EST this is a “free carry” third geological strand to East Star's copper exploration strategy in addition to Strategy #1 and #2. The Getech partnership combines proprietary datasets and basin analysis capabilities with EST’s sediment-hosted copper exploration expertise and capabilities. The results of analysis are pending. Once completed, fieldwork will be undertaken by the Company before any initial licence applications are made.

#4 Keeping the Lights On

Including exploration, the Plc requires -£0.5m to -£0.75m per year. It has no income as such other than grant income (from BHP in 2024). £0.4m of net cash as at last June was unlikely to last.

Last October it raised £1.16m for ~100m shares diluting by ~33% and so today there are 397,515,919 shares, and approximately £0.9m of cash remaining - so enough to last until 2026. Directors participated and bought £80k of shares. That might not sound much but consider that’s equivalent of 6 months of *all* Directors salaries (based on average remuneration of £45k!). Directors own nearly 24% of shares. They are not working at EST for the salary.

With a £4.4m market cap stripping out cash, you’re buying this for £3.5m. Just based on a Verkhuba valuation consider a recent sale of a Copper Mine: Nussir (part of Baker Steel). Nussir is a 200Kt Copper project (14kt for 14 years) at a 1.14% grade, in Norway (not the cheapest jurisdiction to mine in). Valued and sold at $55.3m.

Verkhuba at 230Kt contained is 15% more resource at a slightly higher 1.16% copper, plus has 1.54% zinc and 0.27% lead adding around 40% additional revenue. On that basis $55m x 140% x 115% would not be unreasonable…. before the upgraded MRE. That’s an $88.55m or £67.1m

That places zero value on Strategy #2, Snowy, zero value on Strategy #3.

Places zero on the lower costs and therefore favourable economics at Verkhuba, the ready infrastructure, roads, smelter etc nor does it factor in the forthcoming (potential) upgrades to the MRE at Verkhuba, nor the growing interest in Copper which is higher than last year when Nussir was sold. EST’s market cap net of cash of £3.5m implies a 94.8% discount to fair value….. just for Verkhuba. Just for now.

Conclusion

Execute Strategy #1 and use the cash to progress Strategy #2 and #3. With BHP already deeply involved, BHP are an obvious target to buy Verkhuba. 0.23Mt is perhaps too modest to be of interest. CAML is another operator in the region and a possible buyer, but these two are not the only ones. It’s not inconceivable there could be competition to scoop up this asset.

Stocko calls this a sucker (4/100). I hold EST and I’m quietly excited about it.

I suspect the real suckers will be those who’ve bought the likes of HOC at a £1.6bn valuation (rated 76 and a high flyer) and not realised that at its current price and prospects, EST could be est-eal.

Regards

The Oak Bloke

Disclaimers:

This is not advice - you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Capital raise:

https://www.londonstockexchange.com/news-article/EST/proposed-subscription-wrap-retail-offer/17070528

Up 60% in 5 days!