FAIR Euro-nough

The February 2025 update from FAIR

Dear reader

Today’s news is a watershed moment for OB 2024 idea Fair Oaks (ticker FAIR). It might appear to be a “Grand Reset” from a high-octane, USD-hedged CLO Equity play to a more stable, Euro-denominated mezzanine "Income" play. But there’s more to the story than that.

When you combine today’s announcement with the December–February data, the picture shows FAIR pivoting from a high-yield equity fund running hard to stand still to a higher-quality, more defensive, Euro-centric debt for the short term.

Faced with February’s data and the deterioration disclosed post period it is a sensible precautionary move. But that’s not the extent of it.

This is a precautionary and not a forced move. Cash yields actually improved slightly in February to 31.9%.

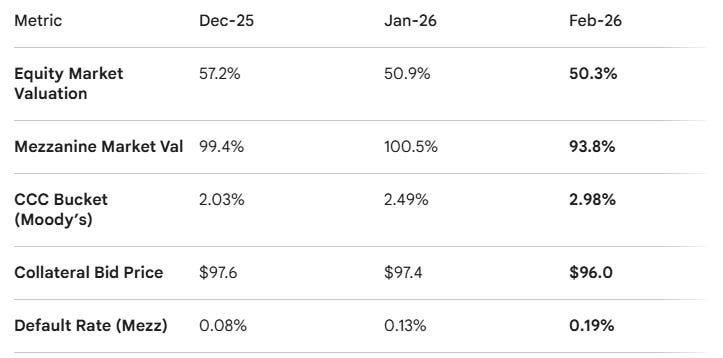

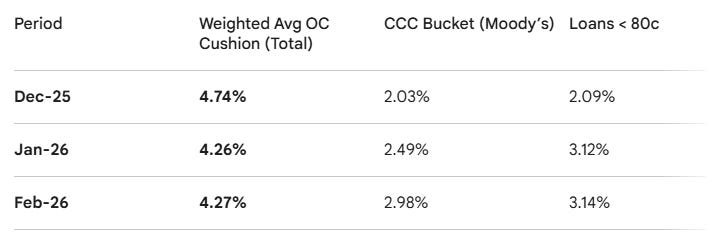

Also assets still exceed liabilities by 4.27% (the avg OC test) as at end of Feb, and the CCC bucket at 2.98% shows it is 4.52% away from the 7.5% tipping point where CLO equity cash gets diverted. Data as of March 10th show some further deterioration in sentiment - as one might expect.

Post period, we learn, the bid loan price reduced to 94.4c by March 10th reflecting deteriorating trader sentiment of 0.8c. A lower payout helps weaponise cash by preserving cash for reinvesting at the bottom.

Particularly since there are strong Funds like FOAKS 6X SUB which have a <80c of just 2.77%, a % CCC of zero, a strong OC cushion of 5.08% yet a reinvestment window until 2030. An ace up FAIR’s sleeve.

1. The “Dividend Cut” - and the upside

The Old Way: You were getting 2 US cents per quarter (8 cents/year). On a $0.45 share, that was a 17.8% yield.

The New Way: They are targeting 1.00 EUR cent per quarter (4 cents/year).

The Math: 4 Euro cents is roughly 4.3 US cents.

The Impact: Your base dividend is being slashed by 45% (from 8 cents to 4.3 cents).

The Logic: They are moving from a Fixed High Yield to a Base + Bonus model. They expect a total return of 12.5% implying a potential 2.5% bonus to the base dividend - depending on market conditions.

The Pain: The Board admits that the old 17%+ yield was “constraining flexibility.” In plain English: they were paying out more than the portfolio was safely generating. By lowering the base, they can re-invest in cheaper loans (down to 94.4c as at March 10th) rather than draining cash to hit an unsustainable target.

The Gain: With loan prices dropping to 94.4c, Fair Oaks is “ramping up” its European warehouse facility at a discount. When they eventually issue the new CLO, the “arbitrage” (the profit for the equity holders) will be much higher because they bought the underlying assets whilst they were on sale.

2. The 1-for-10 Consolidation (The “Penny Stock” Exit)

The Board is tired of being a “cents” stock.

The Action: 1,000 shares at $0.42 will become 100 shares at $4.20 (then converted to Euros, so roughly €3.95).

The Insight: This is designed to attract institutional investors who are forbidden from buying stocks priced under €1.00, $1.00 or £1.00. It’s a move to improve “market perception,” but it doesn’t change the underlying value—it just makes the chart look more expensive.

3. The facelift to Europe (93% of Portfolio)

The December–February data showed the US Equity (ALLEG) was struggling with a tighter arbitrage.

The Strategic Move: They are killing the US Warehouse and moving almost entirely to Europe.

Why? Europe has lower Software exposure (10%) compared to the US (16%).

The Benefit: By stopping the USD hedging, they save 40 basis points (0.40%) a year in costs. In the CLO world, 40bps is a lot of “free” money that goes straight to the NAV.

4. The “Software Scare” and Iran Conflict (The Real-Time Hit)

February: Average loan prices fell to 94.6c (US) and 95.2c (Europe).

March 10 (Post-Iran Strike): European prices fell further to 94.4c.

The “Rolling Over” confirmed: The “Iran Conflict” isn’t just a headline; it physically knocked another 0.8c off the value of the loans in the first 10 days of March.

Verdict

The move to Euros and Europe makes sense.

The move to conserve cash makes this appear like its moving away from being a “high-octane equity fund” to a more stable, Euro-denominated debt fund, hunkering down for a geopolitical storm. But that’s not the whole story.

It’s true you will get a lower dividend every quarter in the short run, but the “NAV floor” should be much more stable because they are moving away from the more volatile Equity tranches and into safer Mezzanine debt.

Besides, conserving cash for the anticipated fire sale that’s coming is smart, and with the leveraged nature of CLO equity (10X leverage) even fractions of cents on the dollar reinvested advantageously into loans could translate into much larger NAV rewards on the other side of the current conflict and current difficulties, for the patient investor.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Thanks for your analysis, Oak. I hold this in reasonable size and am down 10%. I guess nearly 18% yield was just too good.

I do hope that they use any surplus income for buybacks rather than special dividends. Special divis don't show up on most investment platforms so they don't help market the trust.

Will be a similar type of investment to CVC Growth and Income which yields around 8%.

I've taken a big haircut so patience not forefront here! A couple of years down the line imagine income investors will be rewarded. Entry point here is probably good but for me not so much!

They are still buying back stock though so they think its cheap.