Fixin' PXEN

Updates from Prospex Energy

Dear reader

PXEN is a market Cap of just £16.7m so just €19m.

It’ll all be over real soon soothed Trump earlier this week. And soothed is the right word. The markets magicked away the high oil price, high gas prices, and calm returned. It was frankly near miraculous.

It didn’t last.

It’s beyond the scope to know the duration of the current war and therefore of current prices. There’s plenty of pontificators attempting that already, and I’ve been consistently taking the view that hedging on either outcome and positioning is everything. But regardless, expect challenges in European Natural Gas.

Why?

Europe (incl. UK/Norway) even after years of building out green energy consumes ~17.5 EJ of gas per year. Europe produces ~8.8 EJ of gas and imports ~8.7 EJ.

Oooooh we’re halfway there, oooooh livin’ on a prayer.

PXEN explores and develops European shallow, onshore natural gas projects, as well as produces natural gas and operates nat gas plant in Spain for sale and for the generation of electricity, as well as sale of nat gas in Italy.

PXEN’s focus is Spain, Italy but also Poland. It holds interests in:

Tarba including El Romeral Project (100%)

Tesorillo Project (100%)

Selva Malvezzi (37%)

The Viura gas field. (7.24%)

Polish Applications (100%)

SPAIN #1 - El Romeral 100% owned

There are three producing wells acquired April 2025 although these are near end of life (there was an estimated 0.43 bcf remaining). Applications to permit five further wells remain underway (EIA documentation is awaiting final approval - expected 2Q26) where there’s an average size of 3.6 bcf per well and a 75% chance of success. So a low cost way to grow production.

Overall there are potentially 153.9 bcf unrisked and 119.1 bcf risked of prospective gas resources at El Romeral, or 37.5 bcf on a low-end risked basis.

At €9.2m per bcf, 37.5 bcf is potentially worth €344m of revenue (at yesterday’s TTF prices).

At today’s €15.2m per bcf, 37.5 bcf is potentially worth €570m of revenue or the upper end 153.9 bcf risked could be €2.33bn revenue.

Wait what?

But Romeral might burn it instead.

Wait, really what?!

El Romeral has a rented 8.1MW gas-to-power generation plant as pictured along with a rooftop solar array. A purchased gas-to-power generation plant is on order.

It has the option to add a 5MW array on adjacent land costing around €3m and it also has the option to tie in its gas to the national grid at a -€3m cost.

Then it wouldn’t need to burn the gas. It could sell it.

Why sell it?

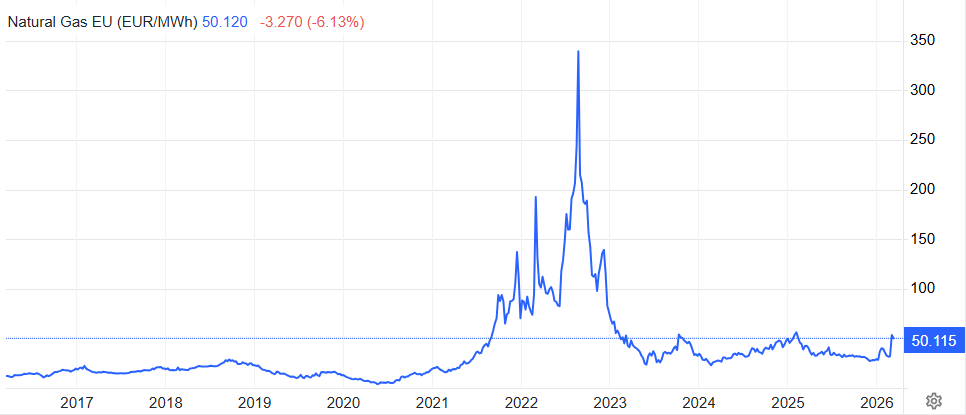

Today, TTF Natural Gas is over €50 per MWh. Let’s put that number in context to recent history. And more on that later.

Spain #2 Viura 7.24% interest

Viura was purchased in August 2024. Bad luck for PXEN continued at Viura until October 20th 2025.

Since then PXEN alongside its majority partner Heyco have enjoyed 0.2 bcf/month production so about €1.8m meaning €134k a month to PXEN and €133k a month of loan repayments. So €0.8k cash to PXEN per quarter, roughly.

PXEN will accrue 14.47% of production income while some £9m of shareholder loans are repaid to PXEN. Interest accrues at 10% meanwhile delivering a £0.9m return. Once that £9m (plus interest) is returned via the 14.47% flow of production income then the share of income drops to 7.24% based on Prospex owning 7.24% of the Viura field.

Reserves at Viura are 6.5bcf net to PXEN, and a drill programme is expected in 2026 with two new wells part funded by PXEN - perhaps out of the accrued income.

The increase to production of 12 mmcf/d is 3,650 Mwh per day and 30 mmcf/d is 9,117 Mwh/d. That’s €166m per year revenue so €12m to PXEN (7.24% share), so perhaps €4m post tax.

The Viura production trials are arguably the most critical operational “de-risker” for Prospex in the first half of 2026. While Selva provides the steady cash flow, Viura provides the massive scale—it’s the asset that could move PXEN from a “micro-cap” to a “mid-cap” if the model holds up.

Here is the deep dive into what partner HEYCO Energy Iberia is actually doing right now and what you should look for in the results.

2a. The Core Objective: The “Dynamic Model”

As of the March 12, 2026 RNS, HEYCO is running production trials under a range of parameters (varying flow rates and pressures).

The Goal: To populate a dynamic reservoir model.

Why this matters: Until now, Viura has been managed based on “static” data (how much gas is there). A dynamic model tells them how the gas moves. This is crucial for managing the water production that has historically hampered the field. If they can prove they can produce gas at high rates while keeping water at bay, the valuation of those 90 Bcf (gross) reserves becomes much more real to the market.

2b. The “Utrillas-B” Upside (The “Deep” Target)

The trials aren’t just about the current producing zones.

The Hidden Prize: HEYCO has plans to test the hitherto untested Utrillas-B reservoir, which sits directly below the main producing horizon.

The Impact: If the trials suggest connectivity to this lower zone, the “Gas in Place” (GIIP) numbers for Viura could see a significant upgrade in the next Competent Persons Report (CPR).

2c. Revenue Maximisation (The Daily Spread)

The operator isn’t just testing for science; they are “optimising generation activity.”

Strategy: Because Viura feeds directly into the Spanish grid, they are testing how quickly they can ramp up and down to catch the peak price windows in the Spanish market.

The Result: With Spanish gas prices currently volatile and high, a successful trial means PXEN starts seeing a much higher “realised” price per MWh than if they just flowed at a flat, constant rate.

What to listen for on March 26th (The IMC Event)

When Tom Reynolds speaks, these are the three “trial” keywords you want to hear regarding Viura:

“Interconnectivity”: If the wells are communicating across the reservoir, it means they need fewer wells to drain the gas, which lowers the future Capex.

“Water Breakthrough”: If they’ve found a pressure “sweet spot” that holds back the water, the field’s life-span (and its NPV) effectively doubles.

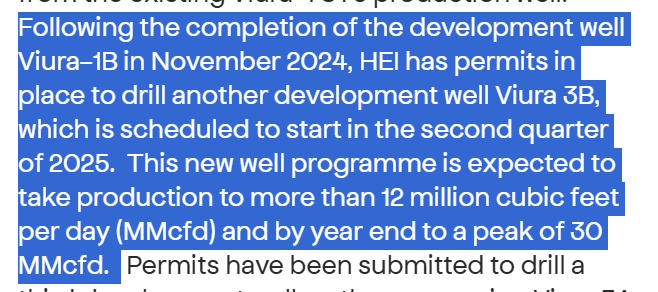

“Viura-3B Timing”: If the trials are going well, they should be able to confirm the spud date for the Viura-3B development well.

To put it in perspective: Viura has an estimated 105 Bcf of total reserves, and so far, only about 16 Bcf has been produced. The trials are the key to unlocking the remaining 89 Bcf. 7.24% implies a 6.44 bcf share to PXEN. At €130/MWh that’s €254m of potential revenue. At today’s prices, that is a staggering amount of value for a company with a sub-£20m market cap.

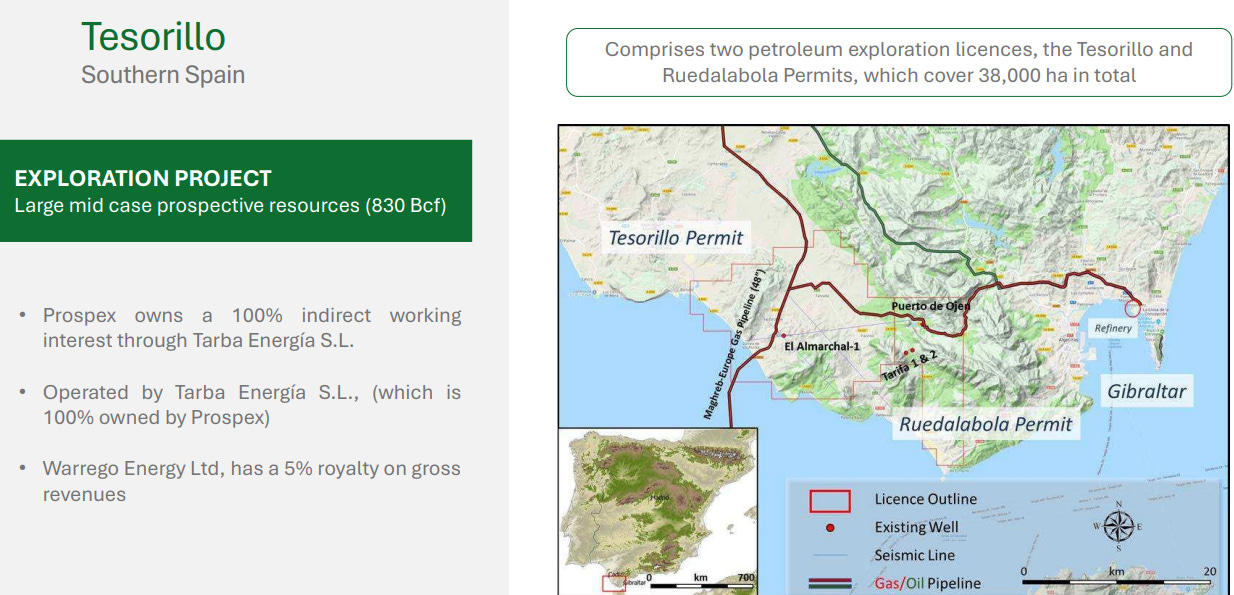

Spain #3 Tesorillo

Acquired in April 2025 as part of Romeral this is a potential bonanza.

While early stage, Tesorillo has a prospective 830bcf of gas. Will PXEN get its suspension lifted here? This resource could be worth €830m at a €1/mcf at an NPV10. Or €2,288m based on its high case resources of 2288bcf. That’s many many times today’s €16.7m share price for PXEN?

As pictured the main gas pipeline from Morocco runs over this permit enabling a future tie back for production.

Next step is an environmental permit to begin appraisals.

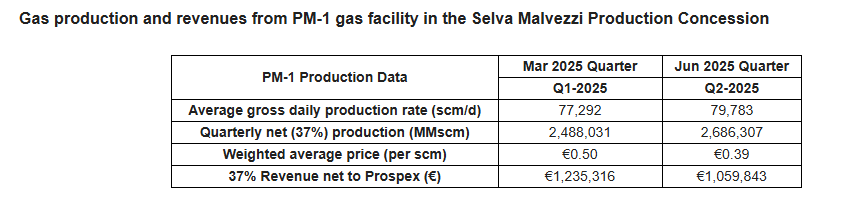

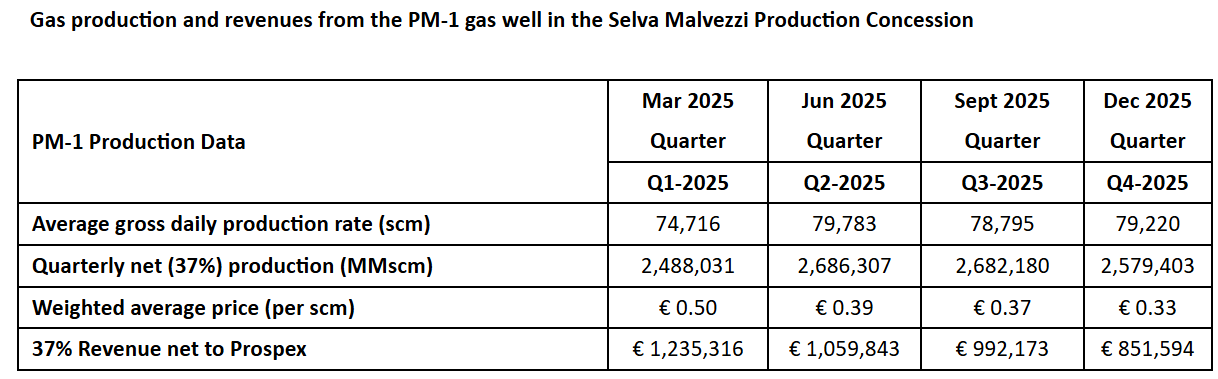

ITALY #1 - Selva Malvezzi

This “bad-mannered Jungle” as the name means in Italian has been steadily producing although falling gas prices in 2025 has tempered returns.

Things change in 2026.

This producing gas asset is 37% owned by PXEN and generated €4m revenue net to PXEN in 2025 and €2.6m of after tax cash flows.

In 1H25 based on the numbers supplied from the 63% partner A$76m market cap Po Valley Energy the net profit accruing to PXEN was €1.03m also.

Gas prices fell away in 2H25 to €32.71/MWh, it’s true, although that’s up over 50% today. (Italy trades nat gas at €0.30 to €0.50 per MWh higher than the TTF)

A helpful way to think about Selva is the cost of production based on 75-80 mcm/day is about -€650k per quarter. Pro rata it was -€1.3m in 1H25 based on the above.

That implies that net profit from Selva in 3Q25 was €0.35m and a further €0.2m is likely in 4Q25.

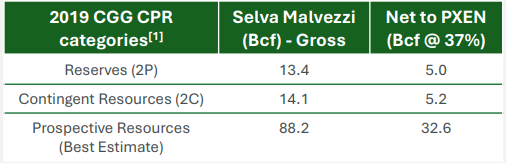

At PXEN goes into 2026 there are 5bcf of net reserves and 32.6bcf of net prospective resources at Selva. Four wells have been applied for permitting, and the results from a 3D geophysical survey is due “in due course”.

The 63% partner PVE.AX is a £41m market cap and owns 63% of Selva Malvezzi, while PXEN.LON owns 37%. Based on Selva being PVE.AX’s primary asset then pro Rata to PVE.AX’s market cap PXEN “should” be (on a read across) a market cap of £23.9m.

But PXEN isn’t. It’s a £16.7m market cap and a circa £15m EV (i.e. it has net cash).

It is true that PVE.AX also owns a gas prospect called Teodorico with prospective 15.9 bcf (so about 20% of the size of Selva Malvezzi). But PXEN has other assets too. Viura (cash-generating), Romeral (cash-generating) and Tesorillo (early stage).

The 50% upside arbitrage here is obvious - but overlooked.

POLAND #1 - Early Stage

The move into Poland is into a third European nation. It leverages Poland’s proven resources, favourable regulatory environment and cost-effective opportunities to develop gas assets.

Prospex has identified two promising onshore licence areas that align with its rigorous investment criteria, namely:

– Proven gas production

– High prospectivity within targeted geological horizons

– Significant potential for unlocking new reserves

– Near-term production potential, with a timeline of 2–3 years

Why Poland?

– Low Geological Risk: Single-event depositional reservoirs reduce exploration uncertainties.

– Cost-Effective Drilling: Shallow, young reservoirs minimise operational costs.

– Favourable Business Climate: Poland’s fiscal regime supports natural gas investment and energy security goals.

-Strategic Experience: Prospex’s leadership team brings prior exploration success and familiarity with Poland’s geology and regulatory framework, gained during operations in 2016.

Electricity

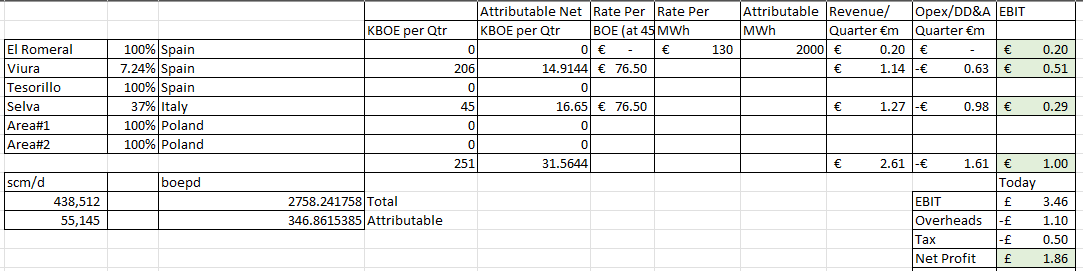

I recently reviewed a broker guess who risked each well and so on. You can get to a higher risked NAV that way.

But let’s just consider here and now. Some assumptions made are different in reality.

The value of electricity for example.

€100 Euros/MWH is assumed, and only 2GWh of power sold per quarter I thought that was very low. Spanish electricity oscillates wildly during a day but 130 Euros/MWh seems a reasonable number for selective sales (typically the evenings).

There are reasons to think El Romeral could produce more that assumed, and at a higher price.

Using €130 Euros/MWH electricity prices and converting €/MWH to €/BOE prices gives us €76.50 currently gives us a 2026 £1.86m net profit (1m Euros/Quarter operating profit); and around £2.75m of cash flow in 2026.

Add to this the £1.6m fundraise this week too. That removes the CLN £1.3m debt overhang.

2026 upsides:

Raise: An oversubscribed raise of £1.6m this week with strong institutional support and a 1 year lock in gives a fully funded buffer.

Selva: 3D seismic results are due 2Q26. Drill programme early 2027?

El Romeral awaits the Spanish MITECO EIA. Energy security pivot could thaw the delay especially as Prospex is positioning this as “low carbon” vs US LNG. Drill programme late 2026 or early 2027 too?

Viura: A Catalyst is operator HEYCO is running production trials to build a new dynamic reservoir model. If these trials prove the reservoir is larger or more connected than previously thought (which recent flow tests hinted at), it turns Viura from a “legacy asset” into a high-impact development project for 2027.

Tesorillo: awaiting environmental permits.

Polish Onshore Gas Permits. Poland has some of the most favourable gas infrastructure and pricing in Europe. Entry here would diversify PXEN away from purely Mediterranean risk and provide a third "leg" to the stool.

The immediate and current read across from ASX:PVE seems the best evidence to me.

PXE is delivering an estimated 8.3X PE where there’s a path to a PE of 1X - 3X with even a moderate amount of luck on the drilling programmes. Given a supposed 75% chance of success for each drill, then you could say extreme amounts of bad luck would be required to not achieve it.

Conclusion

Valued with a seemingly large level of discount vs its co-owner of Selva, delays and bad luck has meant this trades at an ultra low price - up just 15% since November and my “PXEN shovels” article. Four months later and all assets are producing and the new MD is a “do it” guy building his lists of to dos and speaks to being very focused on shareholder value.

Even with a modicum of luck, and being the owner of strategic assets PXEN is well placed to benefit from the current war - or peace.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Very insightful post again Oak. Good that you picked up on some areas of the business and opportunities before it that are lost in most commentary.

The Risk/Reward on Prospex now looks very favourable indeed.

Nice, thank you. Happily I bought PXEN what, six months ago in (~un)happy anticipaaaa... Maybe an article covering similar / contenders from 2024-26 in context of now would be timely?