Dear reader,

For 400 years glasses have hardly evolved beyond the replacement of metal with plastic and tints to glasses. That is until Smart Eyewear was born a few years back. Advances in battery and energy usage, bluetooth 5.1, induction speakers that send sound through your skull to your ears, artificial intelligence assistants like Chat GPT - none of this existed until except in science fiction.

Can Lucyd thrive in this brave new world? Lucyd released their FY23 results.

Tekcapital owns 5.2 million shares in Innovative Eyewear which is ~40% of the total issued share capital of LUCY. LUCY’s share price has dropped $0.42 to $0.29 since my Q3 update. Ouch.

At today’s market price of $0.30 that ownership is worth $1.5m/£1.2m or 0.6p/TEK share (TEK is £17.8m market cap total at today’s 9.5p ask). Because TEK has a controlling interest there’s a 15% mark up on the NAV so 0.7p/TEK share.

So let’s do a quick recap then get into the results.

Lucyd now have over 100 (36 more than last quarter) patents pending/granted including a voice to query Chat GPT interface, the best battery life, lightest weight and an ability to add prescription lenses including Blueshift, and patent-pending hinges. In some ways they have what others don’t.

Although “Smartglasses” can mean different things. Does it mean AR (Augmented Reality)? Does it mean photography? Does it mean videography? Does it mean gaming? These aspects are not part of Lucyd’s featureset. Meta and Apple both have AR glasses that are smart glasses too. The jury is out. Their AR glasses are $ thousands vs $ a few hundred for Lucyds.

My thinking is a cool pair of sunglasses for little more than the price of a nice pair of sunglasses with good audio capability and good battery life is a tick tick and a tick. I’m not a gamer and I simply don’t think Apple’s AR glasses and sunglasses shall ever be one and the same. Bit weird some people muddle them together.

Everyone loves a cool pair of shades - that’s the real world. AR glasses that’s for the Lawnmower Man.

Lucyd Product Progress in Q4:

Safety Glassses are planned for 2024

Reebok are confirmed for launch in 2024 too.

Progress with the Vryb app is planned to commercialise apps in a “patreon” way (as the Oak Bloke predicted)

Progress with accessing music and podcasts sounds interesting - I do do that now with my Lucyds.

Commercial Progress in Q4

The share price tells another tale. Thr share has dropped from $7 at IPO to $0.30 now.

Another placing may be required in 2024. Or we shall at least see participation from investors. I note TEK has underwritten to lend $1,250,000 at 10% interest via a convertible note. TEK’s 40% holding may therefore increase since this convertible can convert into LUCY stock. That might offer an intriguing upside for TEKkies to “see how it goes” and to convert if it is advantageous to do so.

Growth:

The numbers of stores and retailers stocking LUCY grew in 2023, and accelerated but better is coming in 2024. Nautica has over 80 US stores, nearly 300 International stores, and over 1,400 Nautica branded shop-in-shops worldwide. Eddie Bauer meanwhile has 370 stores and Reebok 230 (plus 20,000 concessions). The wider Authentic Brands family boasts 380,000 outlets world wide.

So 2024 retail growth should (at a pro rata rate) increase by more than 8X the 2023 levels. Extrapolating 2023 would result in 2024 delivering about 13,000 pairs of glasses at $199 so $2.6m revenue and $0.83m gross profit. But that assumes all stores are the same…. they’re not. It’s feasible that number would be several times higher.

Later on you’ll see I’m assuming 8X via a compound 80% growth quarter to quarter in the P&L and cash flow forecasts.

The share of sales changes from 2022 to 2023. Ecommerce is doing well and delivers high margin sales.

Driving B2B wholesale only makes sense if the volume outweighs the loss of margin. The 32% gross margin for B2B vs 69% for sales from Lucyd’s web site is a big difference.

Interesting to see that Essilor have an aggregate 65% gross margin too.

B2C sales grew in 2023, reflecting perhaps the success of social marketing and referrals and affiliates.

The Good

Q4 sales very nearly equal combined Q1-Q3 sales

Nautica sales began Q1 (post period)

Price rises have been put through for the v2.0 without any loss in volume growth

Volume Sales are up 50% YTD

Gross margin now between 32% - 69%

Bose are withdrawing from the smart eyewear market.

Share of online sales now 47% - higher margin

Cash - we have enough for “at least 9 months”

Delisting - did you read about the reverse split planned? LUCY “should” be able to do a 10:1

Unit cost savings of 10% planned.

Lion Safety glassses imminent Q2 2024

The Bad

Dreadful level of COS due to replacements (which Lucyd say they’ve now resolved)

Marketing spend is up

Planned marketing spend is up

The Ugly

The share price is down

Cash flow looks ugly

The murmer remains on peoples lips - will Lucyd run out of cash?

So show me the money!

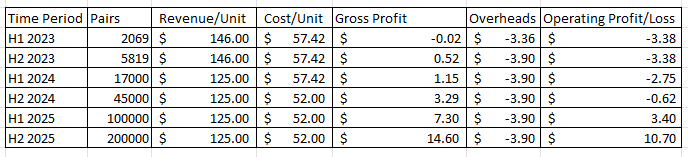

Sales P&L 2023

It was very helpful to extract Q4 (from the 2023 results) and particularly to work out the delta.

I believe nearly $0.4m was lost through replacements, hidden in the COS. $28k relates to 500 pairs given away so I believe should be a sales and marketing expense but again bundled in the Cost of Sales.

We see Q3 and Q4 marketing of nearly $1.7m is 85% of the 2023 budget.

PRIOR FORECAST

NEW FORECAST

The pairs calculation is complicated by ancilliary sales (about 25%). So I was not far out on the per unit gross profit but the value “per pair” is higher due to ancilliaries. I revery to a lower average selling price going forwards as the B2B grows faster but at a lower margin. Costs fall in 2H 24 due to new suppliers at 10% lower prices (per the SEC filing)

The cash flow burn probably leads to the need for some minor funding later in 2024. I account for this via the Convertible note from TEK. (per the filing)

Cash Flow

I’m still predicting cashflow & EBITDA positive by the end of 2024

Forecast P&L - 2024

80% Q-to-Q growth with modest sales & marketing will deliver an EBITDA postive LUCY by the end of 2024.

Conclusion

The extraordinatory cost of replacements in Q4, particularly, the cost of prescription lenses (LUCY have since amended the returns policy and introduced a restocking fee) is a huge negative. No denying. They say they fixed the issue.

The improvement to sales and the momentum combined with the successful Nautica launch is a real positive. The growth is great, and Nautica etc will drive much more growth too.

I say in my Q3 update I wanted to see cash burn drop below $2.7m - I got my wish at -$2.3m. In fact if you strip out extraordinary costs then I got a burn of just -$1.9m. If you take out marketing (i.e. capitalise that cost) then you arrive at a burn of just -$0.8m.

To get that underlying performance in Q4 23 is a real positive. But 2024 remains a make or break for Lucy. I watch Q1 update with close attention.

This is not advice

Oak