Gold on the Trident

$2,200 gold means a large upside for royalty co TRR

Dear reader,

Momentum appears to be growing for Gold. Forecasts are UBS $2250, JP Morgan $2300, Goldman $2175. So let’s say $2200 average in 2024. What does that mean?

In my article TRR-ific we saw how you can get the upside of increases in price (typically the royalty is a percentage of revenue) but are insulated from increases in cost. Let’s consider Trident.

With 37% (and growing) of its portfolio exposed that’s pretty interesting but I also spoke of another upside is simply that the royalty is over an area of land. So if production rises or if new discoveries are made, then that is of direct benefit to TRR, typically.

However we know that its Gold portfolio are already expanding.

The below is the Trident Royalty portfolio.

a. There is quite a bit of expansion of existing gold mines

b. There is a progressive benefit as mines come on stream in 2024 and beyond

c. There’s progressive income just based on what’s already been put in place

d. In other words there’s room for upside from profitable disposals, from operators buying their way out of a royalty agreement, further royalties (i.e. there’s headroom for more deals)

Next of all I show you the royalty stream for each Royalty over the next years. The “Gold Offtake Portfolio” on row 11 comprises the first income for the first 9. This was based on $2k gold.

Given the fact that $2,200 now appears the average for 2024 (and current price) I remodel for this higher price.

P&L estimates for TRR

The resulting P&L model shows me:

The $40m RCF debt which has been negotiated down from SOFR+5.75% to SOFR+2.5%-4.5% (depending on leverage) effectively could be paid down to zero.

This same RCF is now $60m so over the next 33 months there is potential for $60m “firepower”

$25 PAT for FY26 is a PE of 5. For a relatively low risk, that’s simply too cheap. Franco Nevada and Wheaton trade on a 35 and 39 PE by comparison.

Other reasons to be bullish on TRR:

While my focus is on the gold price it would be remiss not to mention:

The RCF has been refinanced as a 1%-3% lower interest rate saving $1.3m a year.

In the past few weeks there have been £175k of Director buys. In fact going back four years there are 13m shares/£4.1m of Director buys.

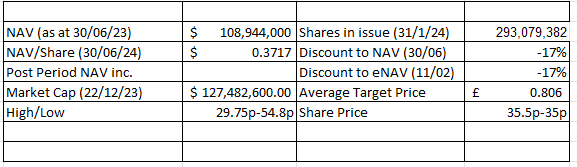

The elephant in the TRR room is Lithium and Thacker pass represents 25.5p a share or 80% of today’s share price and is the largest US lithium mine. For strategic reasons the US gov’t have made a conditional offer for a $2.26bn loan towards the $2.93bn cost of construction. With General Motors committing a further $0.33bn this now appears nailed down.

"We anticipate first production from Thacker Pass within three years and the associated royalty payments thereafter. As previously disclosed, we expect Thacker Pass royalty receipts to have a dramatic impact on our revenue, with $10.5 million generated per year at Phase 1 production and a $25,000 lithium price, increasing to $21 million per year at Phase 2."

Eagle-eyed readers will spot that the FY27 (assuming no other growth) grows income by $8m so PAT to $31m, or £24.40 putting this on a PE of 4.1

Sonora Lithium is 2/3 the value of Thacker. 19.9p/share. Yet is written down by 90% due to litigation - a smash’n’grab attempt by the Mexican authorities to nationalise their lithium resources. It is under international arbitration. TRR has the ability to demand its loaned money back but has chosen to not enforce this until 2026 in order to hopefully progress this through to a succesful outcome. It seems a madness when “friend-shoring” is such a big factor for Mexico to refuse to follow international law and to give reason for international investors to panic….. why would they kill the golden goose? Meanwhile in tax revenue Lithium would be colossal for Mexico. I’m optimistic that a resolution will be reached.

With limited risk and potential for several upsides as well as a growing income, and clearly a bullish Directors, patient investors could choose this royalty company as a way to benefit from elevated gold prices as well as a re-rating in lithium.

This is not advice

Oak

I keep meaning to say thanks for all your effort and analysis you put into all these shares. I don’t always agree with some of it (and I know you got a fair bit of flack on DEC recently) but it is appreciated.

I'm a bit concerned about TRR's Fekola Mine Royalty with B2Gold. The way things are going in Mali, it looks like they might lose this entire stream. Haven't dug into the legals on this. Also wonder whether this is what is holding down the SP