#4 OB Picks for 26 - GRG 3Q25 update

Gregarious News and Garrulous Views about Greggs Plc

Dear reader,

This picture imagines GRG selling monster-sized venison and pumpkin pasties for those with those really hearty appetites. Seems a popular invention - but the eaters have been munching on their pasties for about 30 minutes and they seem no smaller. That’s the magic of Greggs.

The real GRG meanwhile has Pumpkin in their Spiced Latte. And continues to offer some interesting menu choices including egg pots and protein shakes, as well as a £5 meal deal. Here are its range of Christmas bakes:

But I’m not here to make you feel hungry for food but to instead whet your appetite to this OB pick for 2026.

To recap my last article “Greg Weathers”:

The idea of GRG has already reached UK market saturation is a nonsense. There’s plenty of opportunity left in the UK market. Plenty.

Excitement around Tesco. More evidence on that later on.

“Lower profit” in 1H25? Yes a lower PBT and Operating Profit but a higher net income and higher trading profit. Choose your metric to choose your story.

Strip out one-off costs in 1H25 and underlying profit was £10m higher. Strip out the effect of inflation and Rachel’s taxes its trading profit growth trajectory was much stronger again.

2H profits are historically higher. So ‘tis the Season to be Jolly?

Major capacity investments are nearing completion. GRG then turns seriously free cash flow generative.

McDonalds created a 2nd business for itself by offering breakfast. Greggs is going the other way and offering dinner and not just breakfast/lunch. That opportunity is only at its beginning and only at a few stores.

The opportunity to sell the Gregg’s brand via Supermarket’s Frozen Food aisle. Who better than Greggs as a brand to expand in this space?

GRG offers a 4.5% divi and I believe that shall grow - and GRG have a track record of strong shareholder rewards.

Greggs appears to be part of the fabric and zeitgeist of British culture with a strong brand and is outpacing its competitors on innovation, balancing price and quality.

The current share price offers a compelling entry point.

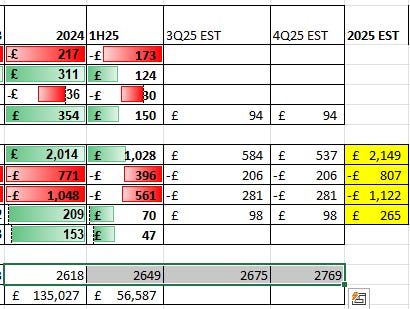

In 3Q25 we learn that LFL sales are up 1.5% yoy compared with 3Q24 and 2.2% YTD. We know from the 2024 Annual Report that 2024 LFL were £1,565m so assuming 2.2% continues in 4Q25 then that implies a £1,598m LFL revenue in 2025.

Meanwhile we learn overall sales YTD are +6.7% revenue and assuming that continues for 4Q25 then overall revenue moves to £2,149m (est) in 2025 from £2,014m in 2024.

That implies non-LFL stores and other is growing like billio. Up 22.3%! We know Franchises were growing at 4.8% in 1H25 and they don’t get a mention in the 3Q25 t/u. Franchises accounted for £280m revenue in 2024 so assuming 4.8% continues that implies £14m growth in those.

We know shops increased from 2,618 in 2024 to 2,649 in 1H25 (+31) and were 2675 in 3Q25 and the aim is to hit 120 by year end (so 2,769 shops total).

GRG Shops generate on average £0.77m revenue per year so if the average extra shops for 2025 is perhaps 40 then £30m of extra revenue is down to extra shops.

So £30m new GRG shops + £14m Franchise Growth leaves £61m revenue growth for the Supermarkets.

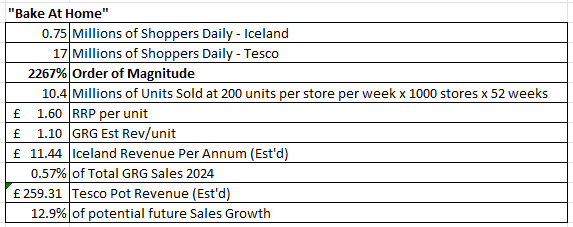

This innocuous little sentence “now available in 820 Tesco stores” might have eagle-eyed OB readers popping champagne corks or chomping down on Venison & Pumpkin never-ending pasties (NB they don’t exist).

It is my belief that Tesco’s will be part of the reason this shoots skywards once the “official” results are out for FY25.

Wait what?

Building up a presence at Iceland took 13 years. GRG nearly replicated that presence in a few months with Tesco with an initial 5 products (Sausage Rolls likely included in those SKUs). In “GRG Weathers” I spoke (in jest) of “What, what do you mean you can’t get the stock to us tomorrow”. Seems I wasn’t that far away from the truth.

Question: Will Asda, Lidl, Aldi, Morrisons stand idly by or be the third? Actually I can imagine Morrisons being trucculent and wanting to do it themselves. Good luck.

Tesco have 3,000 UK stores so with 820 penetrated there’s more to come.

P&L Forecast 2025

Using the 6.7% growth YTD and deducting the £1,028m revenue from 1H25 we arrive at a 3Q25 revenue of £584m. If we assume the same 6.7% growth for 4Q25 then that gets us to £2,149m revenue for 2025.

Extrapolating 6.7% cost growth to COS and SG&A we get to a £265m op.profit up from £209m in 2024, and £196m in 2H25 vs £70m in 1H25.

We are told costs have “marginally improved” so perhaps there’s scope for even better numbers than the above.

If, by now, you are still reading then I think I should give way to an “influencer” (430k subscribers so 100X more than the Oak Bloke :) ) who can walk you through what the “in” crowd have to say about Greggs.

It’s not all 100% positive (conclusion is 7/10 but “I get it”) but that’s why I like to “battle test” every one of my picks for 26 (and every other year).

7/10 in the above review is a solid way to say it’s decent and it costs a fraction of other alternatives. Yes it’s not best of breed grub, but it’s produced efficiently and profitably at a fraction of the price of the alternatives it’s best of breed, for its price. To sum up the commentator’s video “I get it”.

Tesco:

I believe there’s a lot more to come and that’s a further reason why the downbeat 3Q25 update is ok. I get it. I’m happy to hold for the “proper” update knowing that the percentage increases kind of safeguard this idea. Gives room for excitement that the market hasn’t realised the upside - yet.

To recap the relative stats for Tesco are these:

If the range are introduced at all Tesco stores then this Tesco’s partnership could add about 12%+ to GRG’s annual revenue. Perhaps it could be higher or lower but it’s tangible. What if Asda or Morrisons are next too?

What about Gregg’s ambition to broaden its range? Doesn’t this give an opportunity to become a substantial frozen goods manufacturer and supplier of FMCG? Leverage the brand by making a Gregg’s Quiche let’s say. Boom, brand it, sell it via shops but also sell it in Iceland and Tesco. Who has a stronger brand? Ginsters? No. Birds Eye? Please! Horsemeat anyone? You tell me. Greggs has a trendy, wholesome brand untouched by scandal or nonsense. Use it!

GRG Investment Priorities

1. Invest to maintain the business – typically circa 5% of revenue - so ~£100m/year.

2. Maintain a strong balance sheet – plan for a year-end net cash position of c.3% of revenue to accommodate working capital requirements - so £60m balance.

3. Deliver an attractive ordinary dividend to shareholders - target a progressive ordinary dividend, normally around two times covered by underlying profit after taxation. So in 2024 69p per share would be 2X covered. 75p-80p is conceivable from 2027 implying a 5%+ yield.

4. Selectively invest to grow – invest in opportunities with strong capital returns, targeting a return on investment (cash contribution versus capital investment, covering retail, supply, and working capital) of upwards of 25% on company-managed stores

5. Return surplus cash to shareholders – either through special dividends or by buying back shares.

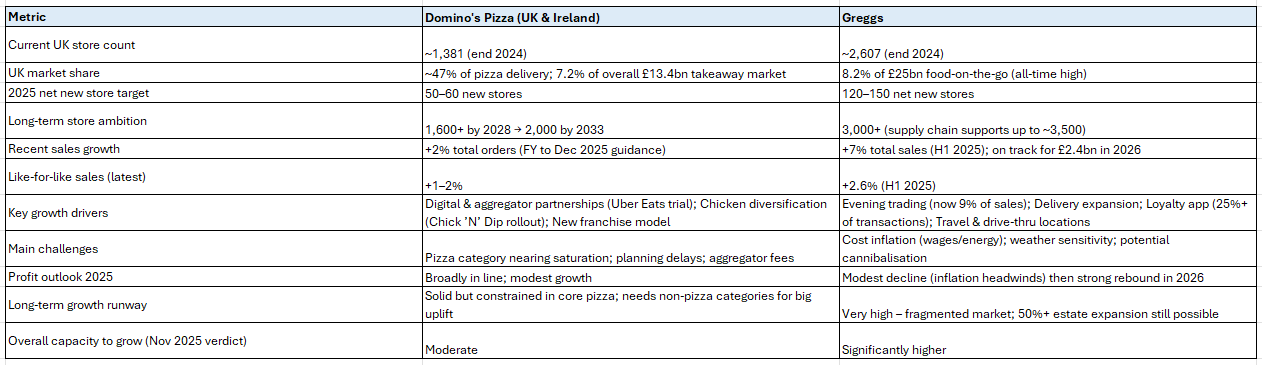

Comparing Greggs vs Dominos

I was interested to see a substack called Brevarthan aka “Brev”. The article got just 1 like! Did he like his own article?!

The article critiques Greggs. The writer describes Greggs as a “walk in shop with limited on demand (sic) food prep. On the face of it that would limit expansion opportunities.”

First of all the writer should learn to use compound adjectives.

Second what other kind of shop is there other than one you walk into? A swim up bar in a swimming pool? A drive-through restaurant I suppose? A “walk in shop” is a peculiar way to describe Greggs, don’t you think? PS Greggs has drive-throughs too. At least research it properly and don’t use weird turns of phrase. A shop, what surely not a shop that you.. that you… WALK into.

Third of all why does limited on-demand food prep limit expansion opportunities? Most of the largest food brands have expanded globally with a limited on-demand prep. McDo is Burgers. Fries. Don’t want that? Want Snails and a Belgian Lager? Forget it. Not at all clear how a focused menu limits expansion. Didn’t limit many other global food companies. No expansion to Belgian Snail aficionados maybe.

Greggs Saturation

Here we go. Again. That old chestnut.

One Greggs per 24,915 people today and the targeted 3,500 shops density would equate to 1 Greggs per 18,571 people.

There is £24bn of “on the go” expenditure in the UK (latest numbers from 2024). That equals £344.33 per person (on average) based on a 69.7m UK population. So less than £1 per person per day. So 18,571 people would equal £6.39m of on the go expenditure…. on average.

An average Gregg’s stores achieves £770k revenue per annum. So Greggs would need to capture 8.3% of UK “on the go” market share, assuming it is only selling into the Food to go (FTG) space, in order to justify 3,500 stores. (£0.77m x 3500 = £2.83bn)

According to Lumina Intelligence it currently has 19.6% of the FTG breakfast subsector, and 10% of the Hot Drinks subsector. Its footprint in evening subsector is much lower but growing fast. If it can get anywhere close to its breakfast footprint then it will justify 3,500 stores quite easily.

Let’s not forget either that B2B sales to supermarkets are not FTG. Frozen Food is a further £11bn market size. Frozen savoury Pastry Products are around £0.3bn within that.

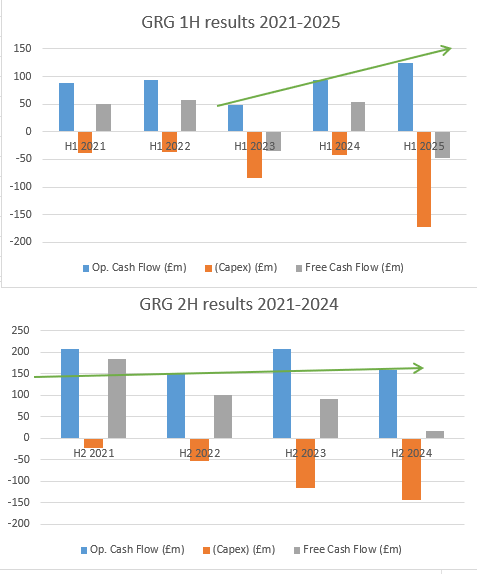

Why is Free Cash Flow a poor metric to judge GRG?

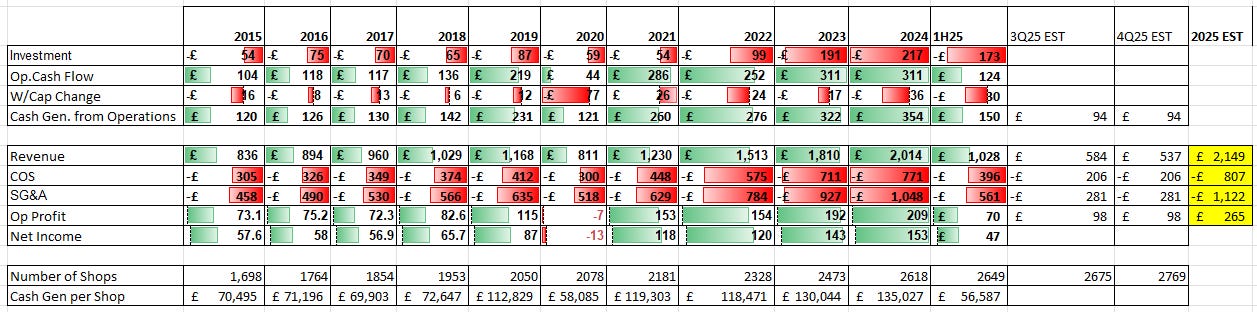

If you consider operating cash flows over 5 years, GRG has been increasing its cash generation generally. GRG estimates 5% of revenue is required for maintenance capex so that’s about £55m per year so -£27.5m per half year in the charts below. The expansionary capex therefore will support growth but also drive efficiencies in supply chain fulfilment.

A flat 2H level of operating cash flow also reflects a period of GRG managing and passing on rapidly rising costs - both from people costs, food costs and energy costs.

The strong 1H25 cash generation is particularly encouraging.

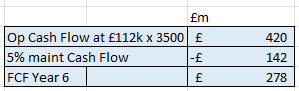

I get close to Brev’s numbers on contribution per shop (£112k vs £111k) but disagree on the £150m maintenance capex aspect. That is 7.4% of revenue today while GRG tell us the number is 5%. (See the annual report)

3,500 shops at £810k revenue would be £2.84bn turnover and 5% would be £142m maintenance capex.

3,500 shops generating £2.83bn at 7.5%-9.5% net margin would generate a net profit of £210m-£270m per year, placing GRG at just a 6X price earnings.

Is 7.5%-9.5% realistic? Burger King generates that level of net profit margin. Costa Coffee (subsidiary of Coca Cola) generates that. Tim Hortons generates that. Yum Brands generates that. Is GRG no less dominant?

All of the above are on P/E multiples in their high 20s too. GRG at a very modest 11X-12X stands out as being particularly cheap.

Let’s use the same approach as Brev and base it on FCF.

A £2,560m undiscounted valuation based on 10 years of FCF discounted to today’s £1,539 market cap is an eyewatering NPV discount of 10% per year.

Brev goes on to yodel-oh-oh-oh the praises of Domino-oh-oh-ohs. Even though Dominos holds a near 50% market share of pizza delivery, and its metrics are far less attractive.

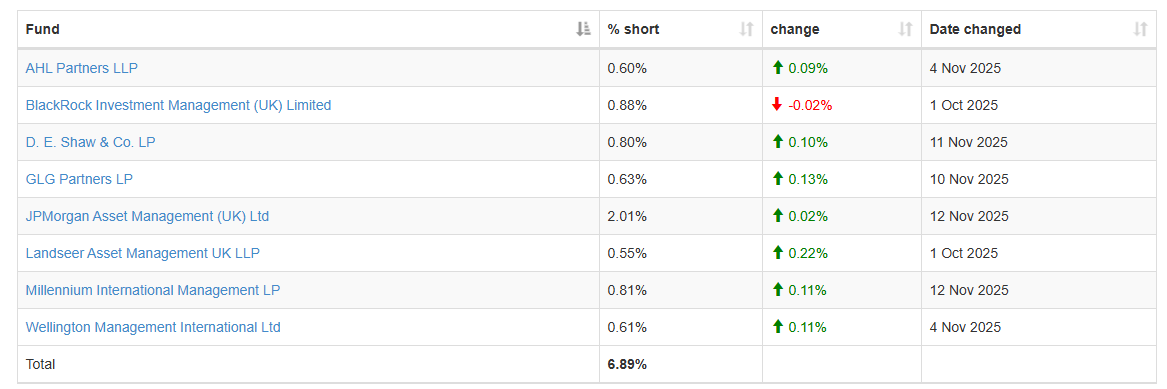

Shorts:

Shorts: Yes there are plenty of shorters shorting GRG. This Brev substack might be one of them. The disclosable ones total 6.89% of GRG’s stock. Fuel for the furnace. Stock borrowers who will need to buy back GRG stock in the future.

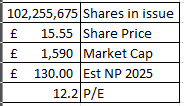

GRG’s market cap at 1505p share price today (17th Nov) is £1.539bn.

Conclusion

A slightly vague 3Q25 update. No one cared. But the percentages tell a tale.

GRG is heading - I believe - towards a far brighter outcome than today’s share price would suggest.

That’s based on an outsize level of growth at its Supermarket sales. Perhaps there’s an alternative explanation but I’m struggling to find one. It ain’t LFL stores sales growth, it’s probably not franchise growth, it’s certainly not the sales of weird Venison and Pumpkin neverending pasties - that do not even exist.

Post 1H25, the 3Q25 result hides the underlying achievement thus far of a huge Tesco deal, improved digital app usage, continued investment, store expansion, also expansion of a store’s remit to later “date parts” (aka the late afternoon and evening), and “made to order”, self service, and delivery too.

Consumer brands are not my natural hunting ground for great investment ideas but numbers are numbers and they speak to me that GRG is worth more than a >£1.59bn market cap when it’s capable of delivering profits well above £100m a year where the 2-3 year profit growth outlook is strong post investment cycle.

The transformative deal with Tesco, the return on investment into its systems, its production, its distribution and its store formats, automation and location. With a growing estate of outlets and from what I can see at least 5 years of UK demand growth still ahead, the evidence of cannabalism is simply not there, for now.

I like its profit share ethos, its brand, and am excited for its further growth and cash-generative future, and there’s no GRG 2025 Christmas advert released yet so oh dear we’ll have to make do with the 2024 one.

If Nigella were describing an investment in Greggs, I imagine she’d be describing those simply sumptious returns.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - you make your own investment decisions. (And pasty ingredients for that matter)

Micro cap and Nano cap holdings including FTSE100 companies might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

I think people like to treat themselves, even those who are hard up.

Grg at a Bridgend shopping complex have relocated to larger premises , still had to wait 20 mins to get served, worth the wait. I have never seen such a long GRG queue, must have been 30 mins by the time we finished. A great beneficiary of the value for money shopper.