Grow forward!

Is GROW's merger with Fwd a good thing or a bad thing?

I covered GROW back in GROW-ing pains and since then we’ve had the H1 results and a merger.

There was a raise of £50m equity @ 279p for follow on investments as well as a 1:9 share issue for the merger of Forward Partners (FWD).

It baffles me that shareholders moan about dilution. Do they not realise that more shares equals more capital? Yes it’s true that the new shares get a bit of your NAV discount but the new firepower can grow the pie so if you trust the calibre of the investment manager then isn’t it a moot point? And if you don’t trust the investment manager then why are you invested? Sell! Run for the hills!

Let’s quantify the dilution:

Why am I excited about the FWD merger and fundraise? Why am I relaxed about dilution?

1. Money!

I’m excited by what Martin and team can achieve with £156m of firepower. Clearly VC/PE is in the doldrums so there’s bargains galore. Great that I can get the experts to buy at attractive values.

2. Accretion!

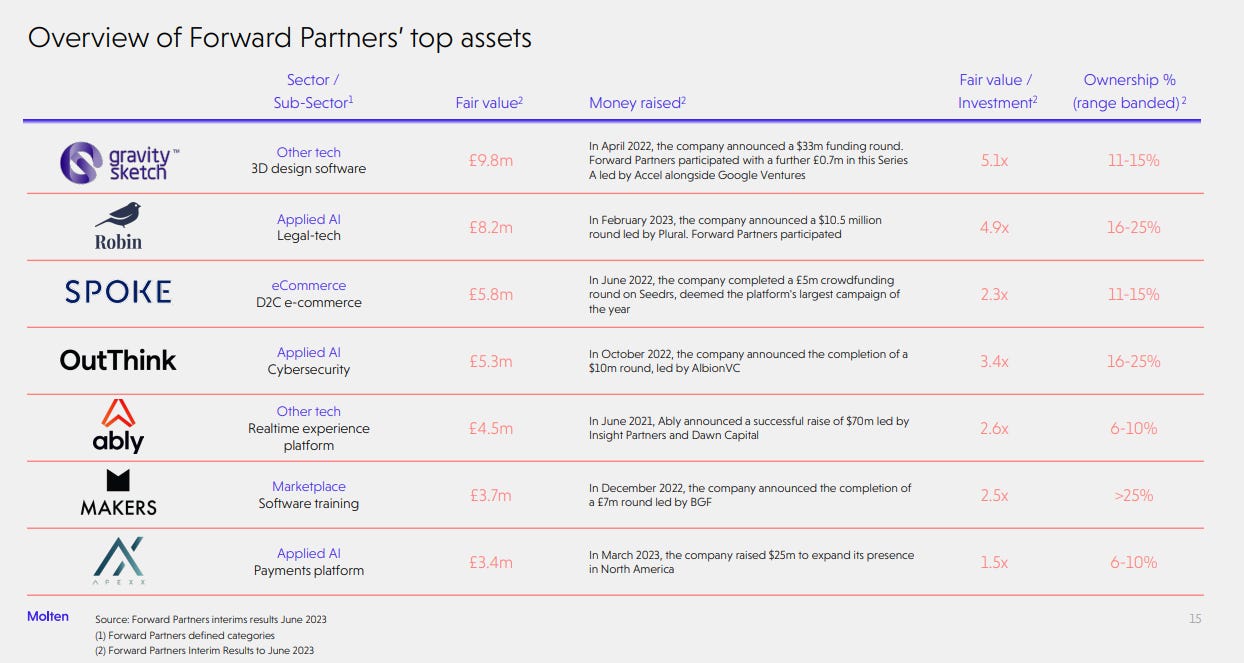

What caught my eye is the top 7 of FWD are about 50% of its fair value and look at the MOIC. (The multiple of invested capital). Average about 3X (already). Some tasty assets and also that they grew revenue at 133% year on year.

Combining the 2 companies and the fund raises leads us to also learn that the NAV has grown by 13.3%. So you dilute to grow.

But OH HO I hear the cynical reader say, Oh ho, 20% dilution is bigger than 13.3% accretion so the dilution is overall a negative.

I YAWN in reply.

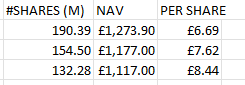

But aren’t you forgetting the firepower? If I use that firepower (cash) to fund buybacks without touching debt I can buy 35.9m shares. Using the RCF I can buy 58.11m shares.

The result is the NAV per share grows. Grows more than where it started (£7.35/share)

Do you still think it a negative, cynical reader?

3.Nic

I rate Nic very highly. And his beard. Must be wise with a beard like that. This merger is a “coming home” to GROW for Nic.

Nic is the founder and CEO of Forward Partners. He has worked in venture capital in London and Silicon Valley for over 20 years. Prior to founding Forward in 2013, he was a founding Partner at leading venture capital firm Molten Ventures (formerly Draper Espirit). Before entering the venture capital industry, Nic worked as a strategy consultant for Gemini Consulting and at London-based startup Operis Group plc.

Nic has led on over 100 investments and has overseen several successful exits, including, most recently, Wonderbly and Heights from the Forward portfolio. In 2021, Forward listed on the London Stock Exchange, raising £36.6m. He currently sits on the board of multiple fast-growth startups including; Robin, Makers and Koru Kids.

Watch him present, and judge for yourself:

Culturally, Forward Partners are much more than a Venture Capital source of money. Tell me reader, where else you could read insights like “How to start a data room”? Think Dragon’s Den. FWD appear more hands on than other VCs. What better way to safeguard your risk capital but to be actively involved with your investee? This is a screenshot from FWD’s growth playbooks page:

Conclusion

Yet again GROW demonstrates resilience and shrewd decision making. I don’t think the merger has been understood even if the IIs backing the raise clearly do.

I’ve demonstrated how the deal adds firepower which can be used in a number of ways to add value.

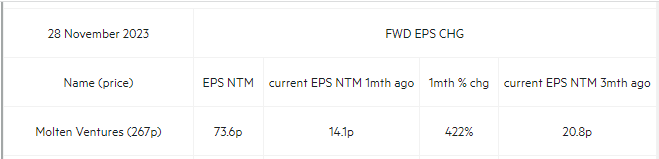

Final thought, did you know reader that Brokers have upped their next twelve month EPS estimates on GROW? By a WHOPPING 422%. Seems Oak is in fine company (for once). A PE of 4.

Recommended reading: 5 insights about the state of AI

If you need advice then go and get it. I don’t offer advice. This article is not advice.

I am happy to share my thoughts on GROW and other investments, and hope you find it insightful and useful.

GROW seems to continue to shrink. Was thinking it was the continual demise of graphcore although that's old news IMO. Could be GROWs debt or maybe that interest rates will remain high for longer preventing exits.....tricky times for the VC market. Rich pickings for the vultures?