HGT-2-dry

Is the drop at HG Capital Trust an opportunity? Or has it been hung out to dry?

(This article was written 4th Feb, published 5th Feb on YouTube, 6th Feb on Substack)

Dear reader

A trust that barely runs at a discount for twenty years suddenly drops to a -26.6% discount because “AI is taking over the world”. Where the MACD revisits an oversold level last seen at the height of covid and where that trust boasts decades of solid performance.

Has the world actually suddenly changed? The markets believe so because US co Anthropic have released a new version of software called Claude. An agentic AI and the sudden concern is that “legacy” software systems are made redundant. Suddenly. Trillions would be wiped off the stockmarket if software is worthless. Or simply worth less.

Let’s take a breath and consider the facts. Is it worth less?

Currently the cost of using Claude as a commercial user is a $100 “Max” plan so £75/month or £900/year per user/seat. Plus usage fees which are based on a vague token cost of $5 per million tokens of input and $25 per million of output. For average levels of usage this will at least double that cost to £2k/year per user/seat. (A major concern for buying is consumption-based billing that makes calculating an ROI difficult)

But is Claude a replacement ERP system? A payroll system? A Procure to Pay system? An Engineering system? A contract system? An insurance system?

No. It is none of these things. It is a means to automate such systems. The data still has to reside somewhere. Could the data reside in a spreadsheet, or in a word document? In an unstructured system? Automation relies on repetition and structured approaches. The risk of operating from an unstructured system with any level of success with any level of complexity has not ever occurred. Has that changed in 2026? Very doubtful. Extremely doubtful. Automation can automate what’s already there. Automate existing structures but not act as a system in its own right - at least not yet.

Businesses do not miraculously jump from system to system either. Apart from the simple commercial reality that finance records must be retained for 7 years under HMRC rules (and similar provisions exist in other countries) businesses will be tied in to contracts - perhaps multi year ones.

Moving systems is tough. People get badges, flowers, thank you cards for successfully migrating systems. Some people climb Everest, others migrate systems. There are compromises, disruption, months perhaps years of configuring, building, learning, testing, derisking and desnagging to move to a new system. You don’t make that decision lightly.

And then there’s the human nature of resisting change.

Meanwhile leaving aside that software isn’t under threat, what proportion of AI projects are actually resulting in success? So far few.

That’s right. You might spend anywhere between £10k’s-£10m’s on automation which fails. If you leave your existing system in place and added AI? Recent research from MIT found 5% success and a 95% failure rate.

It’s not to say that companies aren’t spending money on AI. Adoption is high. But transformation is rare.

There are plenty of reasons to think why AI will not be replacing software or people any time soon.

Considering HGT

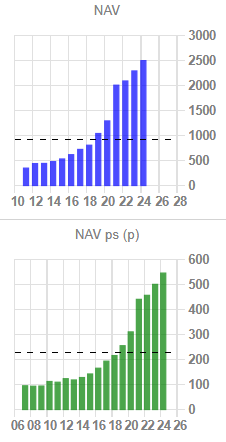

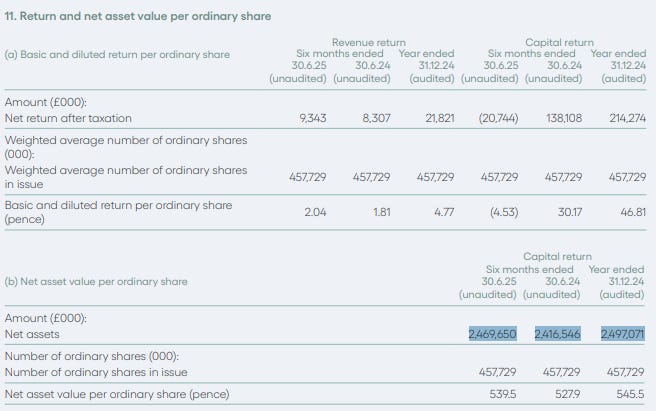

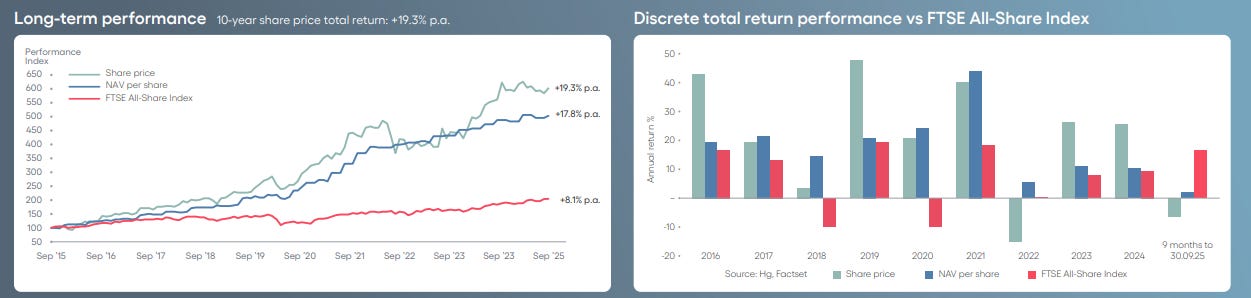

HGT had a NAV per share in 2015 of 142p and as at 30/09/25 nearly quadrupled to 545.5p.

The reason for that growth in NAV was exits and earnings growth in holdings.

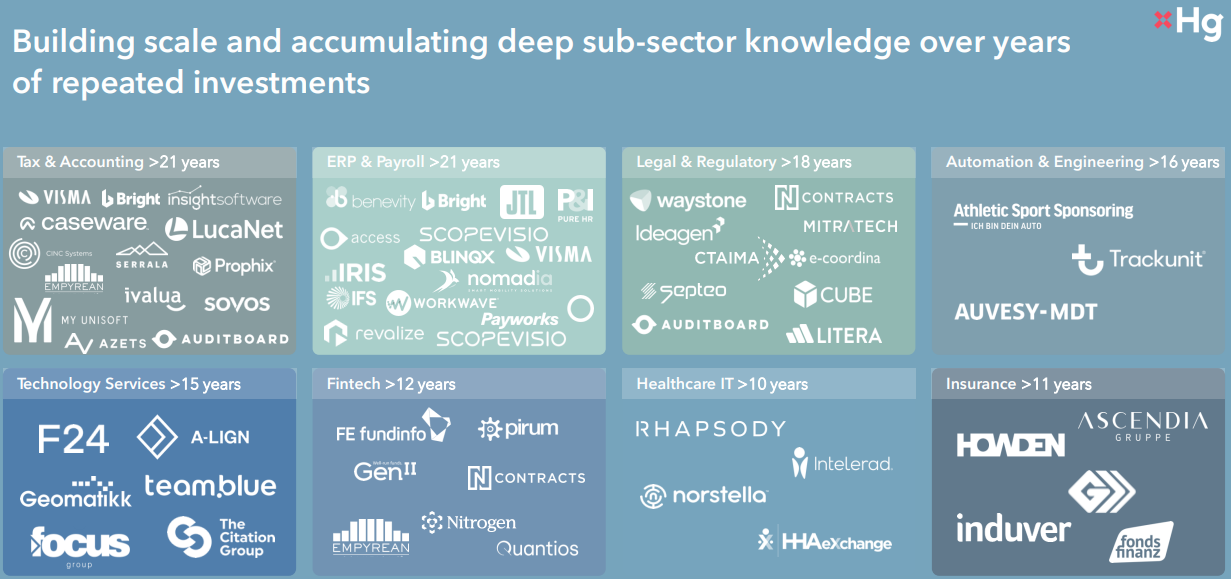

HGT holds many brands and names from across Europe and has deep sector knowledge stretching back decades or at least many years. Rinse and repeat. Buy and build. Consolidate. It’s classic playbook. An accounting system can benefit from a payroll plugin, an insurance platform needs a payment gateway. Your platforms become toolkits to added value.

And now we get to the nub. Even if AI shall be successful, will disruption come from a plugin? Or will it more likely come from the author who - after all - can build a model specifically for a use case. Say Pet Insurance. The nuances might be that your customer is the owner. That heavily uses Social Media e.g. the Poodle Owners club of Bournemouth. That worries about the health of their “fur baby” and are therefore are open to upsell opportunities on their insurance. Where brokers essentially run a back-to-back revenue and cost recognition of the customer pays their insurance and I pay a slice of that to the underwriter. Where claims are an offset against premiums and insight into the actuarial process can be optimised by a large market model.

Would anthropic’s claude be as adept in such a task? No, everything I’ve just posited is specific to pet insurance.

So change from within a software vendor is much more likely to succeed - even if the approach is a partnership using Claude. This has been the case for decades…. and a product released just a few days ago is unlikely to hand brake turn that juggernaut.

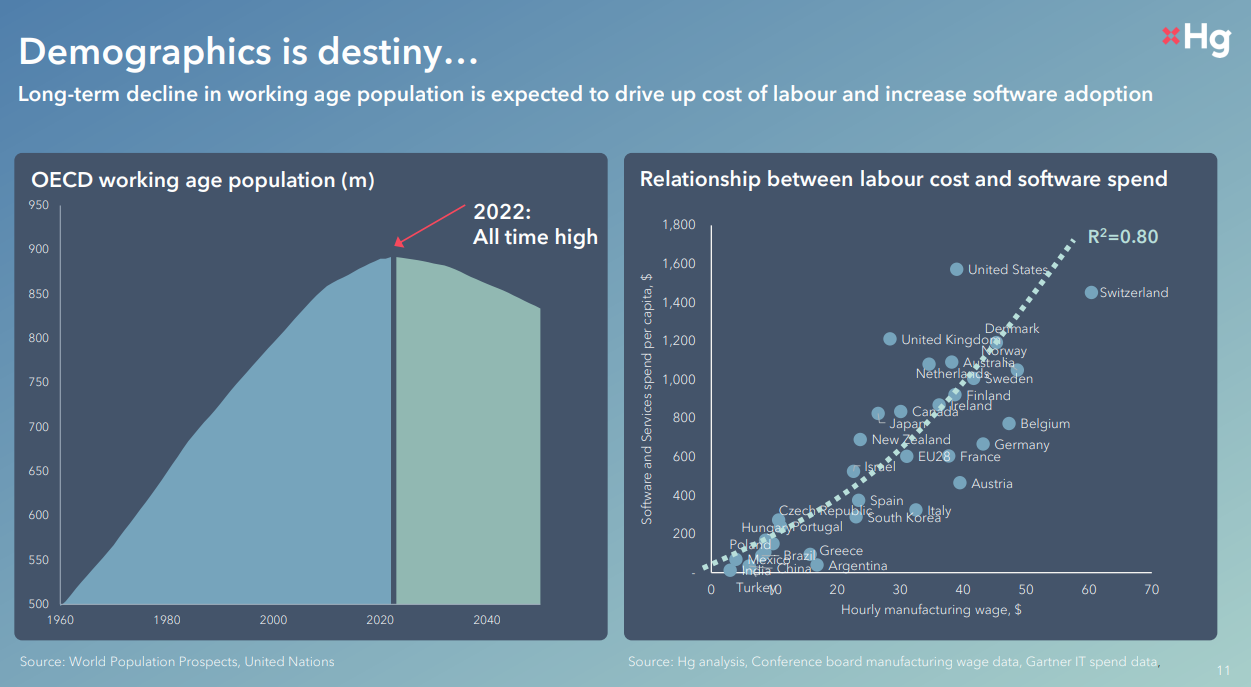

AI is after all simply capital spending. K vs L as my economist professor once taught me. As L increases in price then the substitutability of K also increases. HGT show us that this is the case on a country-by-country basis.

Thanks to Rachel’s taxes L is not getting any cheaper. Wages growth is running at a healthy level (UK wages growth is 4.7% as at Nov 25) thanks to demographics but also labour market participation rates. There are those who can and those who can’t. Skills and frictions abound. Software is a means to improve the productivity of those who you retain. Is that positive or negative for HGT?

Resoundingly positive.

Is it not unskilled labour, or labour that does not adapt to new realities that is in danger of obsolescence in a world of more software and more automation.

That performance has been proven over many years, albeit with a slower +17.6p per share growth to 2H24 followed by a drop of -6p per share in 1H25, and +10.9p in the latest 3 month update to 3Q25.

The portfolio is ERP heavy (56% are ERP/Payroll/Accounting/Tax) and “mission critical” so enjoys low churn and barriers to exit.

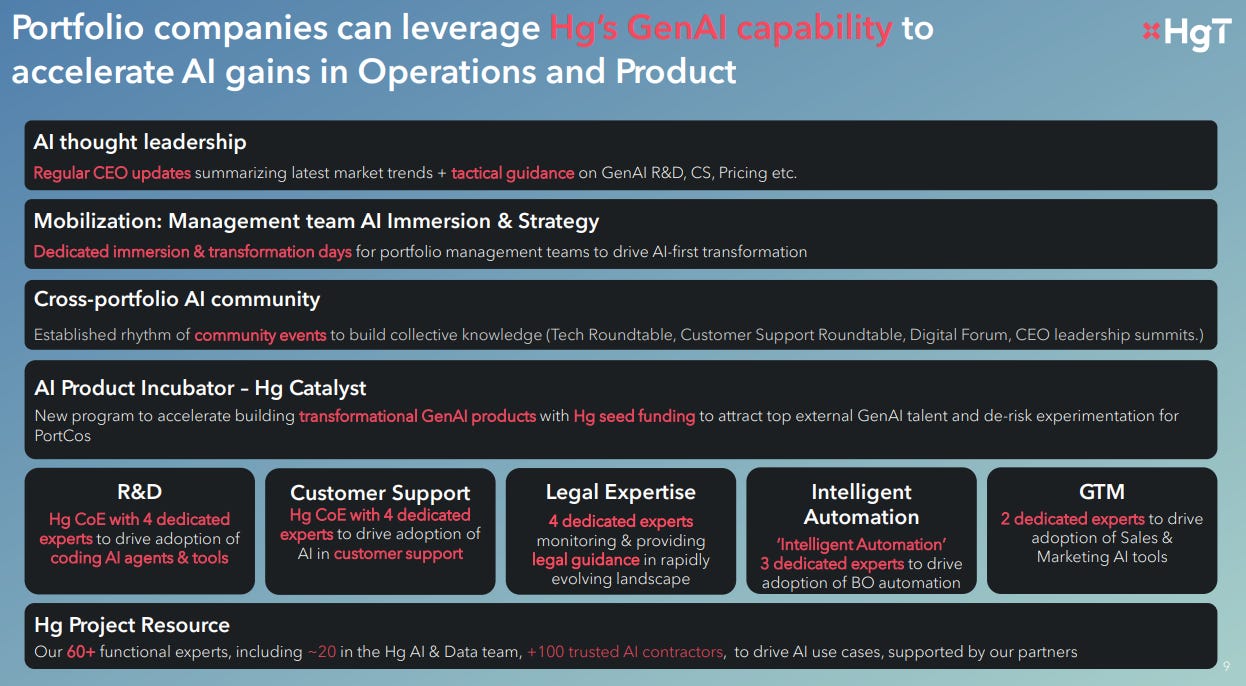

Each HgT portfolio company runs standalone but where 60+ Hg specialists work within “Value Creation” so driving synergies, placements, collaboration, strategic aspects such as AI, access to networks and mentoring. A problem shared is a problem halved and all that.

Conclusion

Companies that deliver software automation are ten a penny. Yes they can announce new software and results that are “Deep Seek-esque”. But I’m sceptical.

AI is simply capital vs labour and AI even agentic AI is unlikely to replace databases and systems. They work alongside.

So buying HGT was an easy decision for me. A set of quality, defensive businesses delivering productivity gains to their customers, compounding on a rule of 44 at a 26.6% discount? (Rule of 44 = 33% EBITDA growth and 11% revenue growth)

Yes please!

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

FWIW i did an investor call with Netcall. Which does CX and intelligent automation software for public sector outfits, banks and insurers where we had an extensive discussion on AI.

No customers are looking to insource any of this stuff and vibe code anything. Having mostly elected to outsource these things to a SaaS player, there seems no appetite to insource again - for which as separate specialist AI dev team wd be needed. One of the operational issues wd be the frequency of change in AI models which wd probably expose the insourcer to significant risks in practice. By using Netcall’s Liberty platform which embeds AI functionality, the customer is outsourcing to a trusted provider wd can deliver the entire package with version control, tracking history and so forth. There’s also a lot of customer feedback that AI is far from perfect, in that an expert human agent is better than the AI, although AI is generally better than average or below par humans, although this may change over time.

In terms of altering the economics of the software provider, this might impact a revs model using per seat pricing (not applicable to Netcall who seem to have some “all you can eat” pricing, but only 30% per seat), in that fewer agents at the customer end to do the same amount of stuff. In fact, the approach to date, seems to be to keep the same number of agents but allow them to do more and perhaps more complicated stuff, so perhaps per seat pricing won’t be affected.

THe CEO says that some 20% of the raw code creation is subject to attrition by vibe coding, but not security, testing and other parts of the value chain (yet). His current view is that they wd probably retain good talent to do more stuff and grow faster. He speculated that the current 30% drop through rate might increase to 40% over time.

So the net effect of AI will probably be positive to EBITDA.

I think that the complicated vertical software stuff in which HgT plays is probably safe from disintermediation, and indeed Netcall is a case where the sp has been heavily and unreasonably bashed by the general AI scare. Nice to have had this convo, since I have accumulated a large HgT holding at a 30% discount.

I broadly agree with your thesis in the long run, as someone who works in tech and uses AI daily. There are many components to a successful software company and vibe coding impacts only a few of them. However, once the narrative takes hold it may be a while before it turns. Would think it better to average in over time rather than take a position now.