Hit & Miss!

Some musings on recent results

Dear reader,

The doomsters must be terribly disappointed and can you hear the shuffling of feet? A clear bullish pattern is emerging, frustrating those who claimed the UK was doomed. Err no. The facts say otherwise.

0.6% quarterly growth compounds to 2.7% for 2024 if the UK can keep the trajectory. With the prospect of interest rate cuts and possibly Tory tax cuts pre election combined with Labour spending post election are we going to see a bumper 2024?

I have spoken before about the productivity effect of technology and particularly AI. It is clearly evidencing in the USA so why shouldn’t it here? If tech can deliver 3% productivity to the UK as the US, then nominal inflation can run to 5% and see remain on target.

It was interesting to read both the HL and ABRDN results during my recent holiday. Not because investing in either was of any interest but what was clear was that investment into the UK markets was rising. The idea that people were withdrawing from the market was clearly not happening.

The markets are well ahead of their 200 moving average.

Even managers appear to be seeing a turning of the tide. Premier Miton for example have growing funds where AuM have grown by nearly £1bn from 3Q23 to 1Q24.

IPOs haven’t yet returned properly to the UK but there is growing interest and appetite.

TMT

Appreciate I wrote recently about TMT in Bolt upright but it was encouraging to see positive Q1 results for its holding Backblaze at the top end of expectations. Revenue $30m EBITDA margin 6%. ARR up 27% YoY. Its target price went up and its share price went down to $7.16 - bizarrely. Cavendish wrote a note and see a TP of $16. TMT sold a 1/7 of its holding at $11 recently but still holds 3m shares. I expect we will see BLZE revert quite soon.

Meanwhile another TMT holding Bolt saw its competitors report strong Q1 updates: Lyft and Uber. Uber saw bookings up 20% YoY and Lyft was 21%; Uber saw $1.4bn adj.EBITDA while Lyft just $59.4m but profitable at last. Uber even reported FCF of $1.4bn.

Previously I spoke about how Bolt is the leader - and first mover - in numerous territories where Uber/Lyft have not entered. Notably Eastern Europe and Africa. Of course you can say the $ value of somewhere like Tanzania is much lower than the USA but it is also true that there is a "leapfrog" effect in those countries where people embrace new technologies in a way mature economies do not. My impression from people who've visited various African countries is that Bolt is the "go to" option for vehicle hire. More recently Bolt has aggressively built a presence in many Western European countries - is large in Germany, Spain and Benelux and now is expanding rapidly in the UK.

It is also true that Bolt is heavily involved in mobility in a way that Uber is not. Electric scooters and the like - and it has learned lessons from early players and builds in sensors and controls to manage the behaviour of its users, but also to manage those assets (to save them from the local canal). The UK's scooter population sometimes appears to be errant children from council estates but in other countries there is a thriving daily hire business. Neither Uber or Lyft are in that space - yet.

Bolt could certainly be complementary to an existing player (either Lyft, Uber or others) so yes could be bought out rather than be listed. And to an acquirer, it certainly has some USPs geographically and in terms of service mix which make it an attractive target.

KDNC

Kadence I noticed its holding EMH is now almost double its recent lows. To the point where nearly half of KDNC’s market cap is accounted for by EMH and EG1 (its 2 listed holdings).

Assuming KDNC’s land holding at Sonora is worthless (and it probably isn’t worthless) you can acquire 34% of Amapa (a $1.1bn asset) for £4.6m. That’s a 98.5% discount to its NPV.

Iron ore is back well above $120 a tonne but Amapa’s iron ore is premium 66% stuff worth $10 a tonne more than the 62% grade. Amapa will also be able to make “green iron” due to the hydro renewable energy sources. ESG friendly high grade iron ore - yours for 98.5% off.

If EMH continues its ascendancy (the NPV of EMH is equivalent to 33.9p per KDNC share) then the 98.5% will tip above 100% discount perhaps to as much as 1100% discount - assuming it’s still at a 3.6p buy.

The next newsflow will be the DFS for Amapa and the DFS for Cinovec (the EMH mine). It strikes me as crazy you can still buy KDNC at 3.6p.

TEK

SALT has been powering up this week. 88p/93p bid ask this evening. I’m not surprised. The American Heart Association says “shake the salt habit”

Yet Statista tells us ready meal consumption will double in the next few years - so the food manufacturers are shaking the salt - not the consumers - and the manufacturers have to use salt because their food doesn’t taste good without it. It’s simple really.

It’s difficult to see how Microsalt won’t or can’t succeed but let’s at least call it as being an idea with good odds and if Pepsi or other food manufacturers embrace it (or buy it) then it will no longer be a £40m nano cap company. It will have reached its blue sky potential.

We do not yet have details of TEK’s AI 6th portfolio co. But I’ve added that based on the fundraise with £500k earmarked to its investment.

Meanwhile BELL has bounced from recent lows. For BELL we need to see a Q2 soft launch of its discov-R device with a Q3 commercial launch. We need to see production and sales - the sales back log. Detractors on bulletin boards have written BELL off based on the delays in funding. But the detractors are not the distributors nor are they the customers - and these key audiences are the ones which matter.

LUCY is nearing its launch of LION safety glasses and the roll out of Nautica is underway. We need to see 80% Q-to-Q growth in order for LUCY to succeed - although a recent fundraise has lengthened the runway a little. We also know it struck a deal with New Look a large Canadian opticians but potentially we’ll not know much else for another 6 weeks until its Q1 results.

Guident hosted an autonomy day and featured heavily at the National Autonomy day followed. The sponsor list is intriguing. Jacobs an Engineering Consultancy with 60k people and $16bn annual revenue - of which $10bn is Consultancy for “critical infrastructure” are heavily involved with autonomous vehicles - for example this thought piece by Jacobs is interesting.

Equally, Balfour Beatty a FTSE 250 engineer again a huge engineering firm and this 2050 innovation of AVs is interesting too.

Several competitors to Auvetech are also featuring as sponsors. Oxa, Holon, Beep and Adastec are all in the same space while Novelsat and Airspan are connectivity providers. It is highly likely Guident have had conversations with all of these and will announce partnerships.

The Star Robotics deal is the first example of the potential I spoke of about Drones and Robots I mused in prior articles. The wider market for humans in the loop is much larger than just public transport vehicles I argued. This is small beginning but illustrates the opportunity.

I would be very surprised if the fair value of Guident remains at just 7.3p a TEK share, based upon the progress but time will tell.

Notice I assign zero for ReVive yet we may one day we a licensing deal and progress there too.

So 23p where nearly 16p of that lies in publicly listed holdings. The disconnect in the TEK share price is incredible.

8.5p bid/9p ask puts this on a 60% discount to NAV where 172% of TEK’s share price is in publicly listed assets.

And it’s 60% if you believe Guident is still only 7.3p and ReVive is worth zero. And that SALT, BELL and LUCY can’t go up from here.

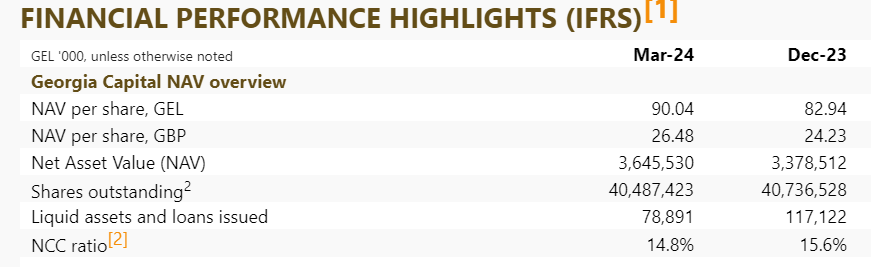

CGEO - Capital Georgia

Flag waving and a law which undermines human rights had Georgians protesting in their thousands. 70% want to join the EU and the law is a nod to Russia.

The protests have shaken investors and a retracement in CGEO and BGEO (bank of Georgia) despite knock out Q1 results exceeding the prior knock out Q4 2023 results!

A 56% discount to NAV when that NAV is growing 9% quarter to quarter?!!

I’ve topped up since I believe this unrest will settle. Ultimately Georgia is implacably opposed to Russia. Russia grabbed land from Georgia (like it did with Ukraine in the Crimea). Georgia trades with Russia but has no wish to be under Moscow’s orbit. It has no need to do so. Joining the EU meanwhile, is a path to further prosperity.

The protest is centred on requiring NGOs to declare income from overseas which seems a sensible idea, actually. Why is that a “Russian law”?

Conclusion

To conclude, evidence of a sea change is underway, and what some readers have dismissed as unhinged Oak Bloke optimism appears to be turning to tangible results. I seek to evidence what I write - so what detractors call optimism I consider to be presentation and interpretation of the facts. Facts and evidence precede results in investing. While detractors consider results (i.e. low share prices) or a lack of news to be facts and evidence. Markets are pure emotion, while strategy, moats, progress, profit and cash flows are evidence. Knowing the intrinsic value and value of future flows of income mean you’ll statistically win more than a momentum chaser riding a rollercoaster of fear, doubt and euphoria.

Well reader, I will leave it there for this evening. Writing after a busy week on a Friday eve is not ideal for me. Perhaps I’ll add more to this musing over the weekend.

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings even those held in VC stocks might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Hi Oakbloke, nice musings.

I occasionally question/disagree with you, but never question your optimism, BECAUSE it's based on diligence, detail, rather than euphoria, and is a refreshing citadel of light breaking through the prevelance of doom and gloom. And I got one, even when I don't agree, value your contribution in engendering the style of investing you (and I) advocate. Focus on the detail, ignore the noise, and patiently wait for others/markets to catch up.

Couple of quickies - agree on BGEO/CGEO - the drop was irrational and an opportunity; BSE is very quick (AND elongated) value in plain sight, albeit noting the still large 'arbitrage' oppurtunity in its current SP, seemingly to only you and me!