I like the base base base base - I like the buttery biscuit base

Is BASE resources an interesting buy?

Dear reader

Australian firm Base Resources (BSE) also listed in London, announced a take over offer from Energy Fuels (listed in the US and Canada) ticker UUUU.

Should you buy BSE? Let’s consider Energy Fuels first. Selling at half its recent 2022 highs of $10.85 per share it trades at $5.54 as at 3rd May 2024.

Strange, to fall when uranium prices are above $90 per pound, after surging to near $110 lb and trading economics tells us that there is tight near-term supply of uranium further magnified by speculative buying from physical trusts. I see Rick Rule and others speaking of the virtues of Uranium.

Meanwhile - crucially - the US Senate approved a bill to ban imports of nuclear fuel from Russia, the world’s top producer. Should President Biden pass the bill, Western converters and enrichers would fall under added capacity strains as trade restrictions and voluntary shuns of Russian fuel drive utilities to compete for long-term contracts.

This added to supply downgrades of uranium ores from Canada and Kazakhstan in 2023 compound the potential further rally for uranium prices due to its bullish long-term demand.

In recent developments, the US and 20 other countries announced plans to triple their nuclear power geneartion by 2050. China leads the nuclear energy bets, currently building 22 of 58 global reactors, while Japan restarted projects to build nuclear reactors.

Is uranium in a perfect storm?

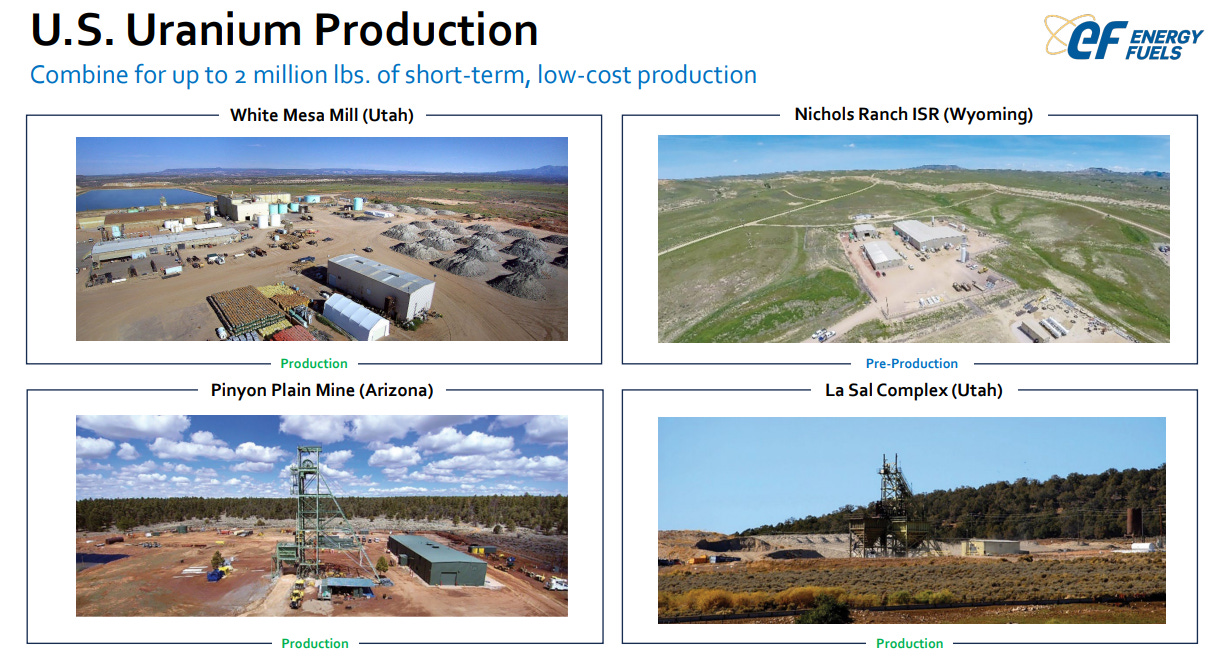

UUUU say they will produce 2m lbs of Uranium in 2024 which is $180m at current prices or $220m if prices revert to $110/lb.

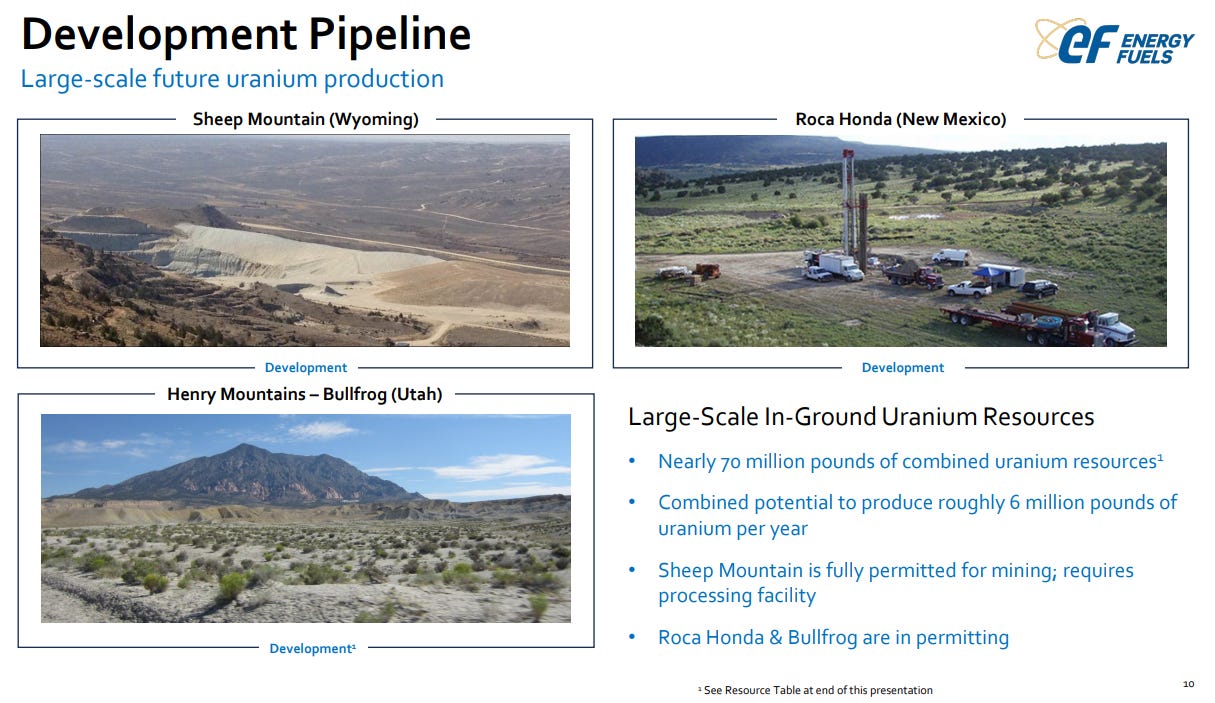

It is also developing production of a further 6m lbs a year. These will come online in future years.

Moving to Rare Earths. 2024 production is up to 800 tonnes of NdPr. That adds a further $44.8m at current prices (or $56m at 1,000 tonnes). In 2-3 years that balloons to $168m-$336m NdPr plus $63m Dy and $67m of Tb. So up to $470m additional turnover in 3 years.

It doesn’t end there. Additional sources of REE from its acquisitions (including Base) will feed further REEs into the US processing.

These could add a further $500m of REEs revenue per year

So UUUU could be a per annum $billion uranium and $billion rare earth producer in three years. I haven’t been able to guage what the profits would be but given the elevated commodity prices it’s fair to say the word “attractive” would feature.

But there is also Vanadium and production into several million pounds (once prices recover). Vanadium is at extremely low prices for now but will Russian import restrictions extend to vanadium? Will China limit vanadium exports? Will VFRBs (vanadium flow redox batteries) continue to grow and expand boosting the demand for vanadium? Moreover Iron Ore is rebounding to $120 due to infrastructure demand - that’s a huge positive for vanadium going forwards since vanadium is added to steel to improve its structural strength.

UUUU’s acquisition of Base also includes the heavy mineral sands at Toliara in Madagascar, as well as Kwale in Kenya. Kwale is nearly exhausted but has found a final lease of life for the next 18 months and is expected to drive a $26m EBITDA in 2024 from Kwale.

Toliara meanwhile is awaiting permits ahead of a FID. Those are imminent after an election last November delayed things for Base. Base recently released a “bolt on” PFS concerning monazite production for the Toliara project - clearly relating to the prospective acquisition. The PFS evaluated the possibility of recovering the monazite waste stream of the planned Toliara project.

The key findings were:

•21.8 ktpa LOM avg 90% monazite production over a 38-year life.

•59% TREO grade

•24.5% Magnet REO:TREO (Nd/Pr & Dy/Tb) ratio.

•35% payability for magnet REOs only.

•Operating costs of US$1,089/t monazite.

•Marginal US$71m capex.

•NPV10 of US$999m

A bolt on IRR of 79% (2027-30 avg monazite price ~US$6,400/t).

When combined with the existing Toliara mineral sands project, the monazite component doubles NPV10 to ~US$2bn, increases the overall IRR to 32% (from 24%) based on an initial capex of $610m (HMS)+$71m (Monazite)

Conclusion: Should you buy BASE?

If those attractive numbers from Toliara (and Energy Fuels) have you salivating then let’s understand the pathway from here.

Base Resources has reached a binding agreement with Energy Fuels to acquire 100% of Base via a scheme of arrangement.

BSE shareholders to receive 0.026 UUUU shares (worth 12.3p based on UUUU's closing price of US$5.84).

A special dividend of 3.4p to be paid to BSE shareholders (US$52m out of US$79m in cash on the balance sheet)

Deal expected to complete in 3Q24.

The total implied consideration is 15.7p (valuing Base at £184m). So at today’s 13.5p ask price for BSE you are paying 10.1p net of the special dividend. Meanwhile UUUU dropped 5.1% on the news so you are paying 18% below the implied market price of UUUU (or 13% below the UUUU market price based on its 5% drop).

UUUU had a target price of $9 according to Canaccord Genuity prior to the BSE acquisition.

UUUU looks attractive in its own right. A $billion market cap generating several $billion turnover at attractive rates seems like an opportunity for investors to seriously consider. A $2bn NPV Toliara operation added means that its $9 target price could double to $18 a share.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

Post Scriptum - Kazera

Eagle-eyed readers who know about the Oak Bloke 20 ideas for 2024 will know that Kazera a £6m market cap minnow sits on 60% of a HMS holding called Whale Head with 49.9% HMS concentration (compared to just 6.4% at Toliara although the VMS valuable mineral sands are probably a bit higher at Toliara). The NPV of Whalehead is $449m (60% of this being $270m NPV to Kazera) compared to $811m NPV for Toliara.

KZG production has been held up for 8 months due to MONAZITE. So could there be REEs in those HMS? Could we see UUUU make a bid for Whale Head? It is an intriguing possibility.

The NPV is about 55% of that of Toliara before Monazite (and a similar 2.5X might occur with the Whale Head’s Monazite potentially). 55% of £184m is £101.20m and 60% is £60.7m. £60.7m is over 10X today’s ENTIRE market cap for Kazera. Kazera also holds a lithium mine in Namibia (in the process of sale) and a diamond mining operation but has a 29.99% shareholder who has other projects on the go.

PPS

you might be confused by the title, and what a buttery biscuit base has to do with anything. So for a bit of fun, this video link makes it clearer. This video always amuses me and Swedemason is a genius - the Banksy of video editing. Jeremy Clarkson’s beatbox is worth a watch too. Hopefully we’ll see a reprise and a Sunak vs Starmer video later this year? Enjoy!

In UUUU's recent update, they said that quarters uranium sales were at a 56% gross margin

Hi OB, not sure whether you've seen this, and whilst a promo interview, the UUUU VP instills confidence. Particularly liked his response about buying BSE - "you can hardly go wrong by buying the best asset in the world...."

https://m.youtube.com/watch?v=y-0kTvyTyes