IDHC - buying back in

FY2025 results

Dear reader

As readers who’ve read the OB picks for 26 update saw a further idea crept back in to the picks for 26 - and at a discount too! Here’s why.

More, more, more, more and more. The efficiency engine at IDHC is firing on all cylinders.

“IDH has delivered robust growth, strengthened its regional platform, and enhanced the quality and breadth of its service offering, all while navigating a complex global and regional environment” says Lord St John and “We are cautiously optimistic that increasing economic stability in Egypt… will provide a more supportive backdrop… although conflict with Iran may introduce renewed pressure”

A core strategy is geographic diversification and a focus towards higher-value more specialised services. That suite today is more than 3,000 internationally accredited pathology tests complemented by a full range of radiology and radiotherapy services.

But also “digital healthcare” which means prescription delivery to your home, in-home consultations with a digital referral service and digital access to health records. Historically you’d be a “walk in” which meant physically doing just that. IDHC has brought that into the 21st Century and to the convenience of a customer’s home. The UK is starting to do that (e.g. via Oak Bloke idea recently covered in “Fuelling up with ESO”) but so far only NHS England permits this - the other UK regions haven’t kept up with Egypt!

IDHC is focused on building its brands across its markets. Appreciate these aren’t familiar brands to you, reader (probably) but they are the “Bupa” of those countries.

How is it that I was able to buy back in at less than March’s $0.60 sell? At $0.56 rebuy per share the buy price last week was just too tempting. The results of IDHC’s 2025 results were superb.

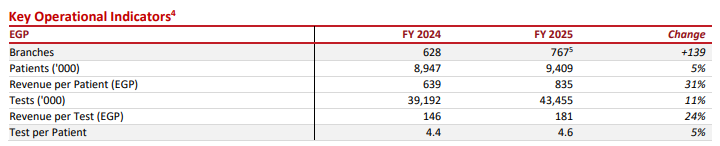

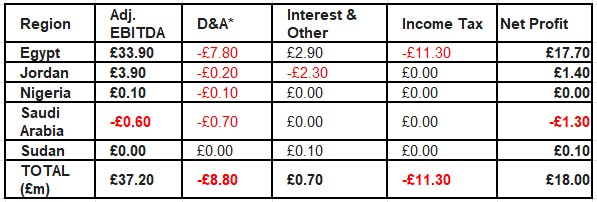

The full year results at IDHC provided confirmation that 4Q25 was solid compared with 3Q25. Overall EBITDA profits were up across every country in IDHC’s coverage in 2025.

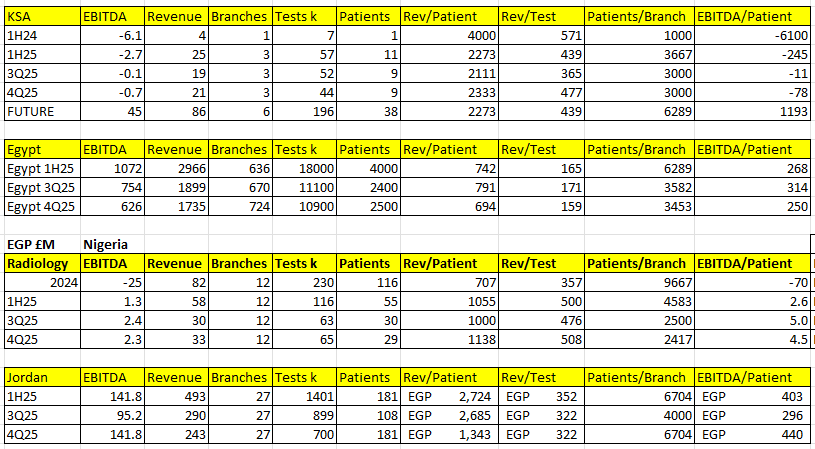

We also see Radiology grew to EGP310m from EGP 224m but don’t get an exact breakout - we do know it is part of the reason the revenue per patient is up 31% Y-o-Y.

Progress was made across every country in 2025.

Although the 4Q25 admittedly weren’t all just continuous improvement vs 3Q25, the 4Q25 results were substantially stronger than those of 2024 or of 1H25.

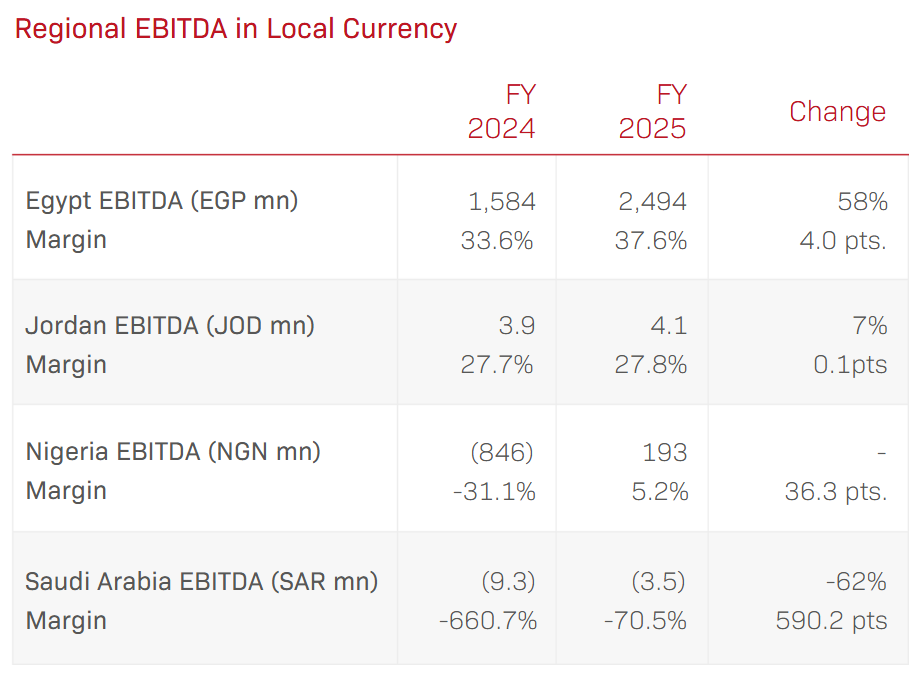

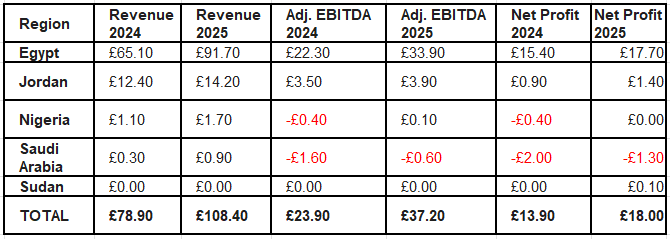

Net profits in EGP terms reveal a performance across each country on a net profit basis too.

In GBP terms we see Nigeria on the turn, KSA improving and Egypt going from strength to strength.

But also the Egypt segment carrying the lion share of the central costs and tax burden. If the other regions can grow then they are worth investing in - but apart from Jordan - IDHC are investing into those still and they aren’t delivering any net profit today.

Post period and today the EBP is 72.5 to GBP (so slightly weaker and down from 66 EGP:1GBP)

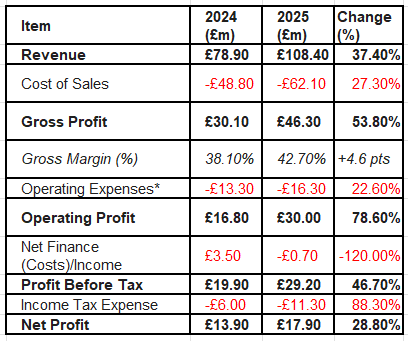

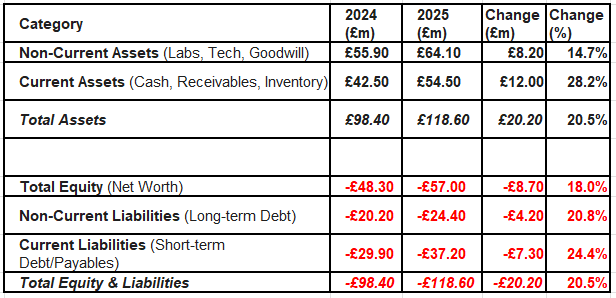

The P&L for 2025 is impressive on top of 2024’s results which were not shabby:

(On a £240m market cap £18m net profit is 12.5X P/E although adjusting for one offs and tax underlying net profit was below 10X P/E)

I’m presenting the article in GBP terms (at 74EGP:1GBP).

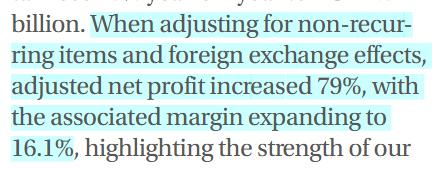

If we consider the EGP results and strip out currency effect and exceptions then we see a 79% improvement to net profit in 2025 vs 2024. (Although only 29% improvement in Statutory Terms).

GBP translation makes the results appear less impressive.

We see an efficiency effect as revenue growth outpaced cost of sales growth and operating expenses. Marketing expense increased 50% reflecting an investment into its brand and into share of mind. Profit increased despite a drop in Finance Income, reflecting the strength of the core business. The increased tax bill is due to prepaid tax on subsidiary dividends up to the parent (Egyptian) company as well as losses in KSA/Nigeria that they can’t yet offset. After those adjustments net profit was about £21m putting this on a P/E of 11X with other exceptions putting this below 10X.

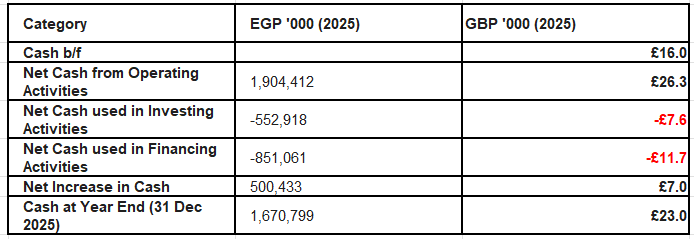

The business was highly cash generative and increased its dividends in 2025. This is a cash flow summary in GBP terms:

PP&E capex increased to £27.5m, reflecting adding 139 new branches and the related hub-and-spoke equipment to support those.

Cash rose nearly £7m even after factoring in £7.4m of dividends and the acquisition of the Cairo Ray business. Receivables rose 39% to £19.4m reflecting the slower payments of Contract customers. Cash net of borrowings puts IDHC as net cash.

The put option reserve increased 20% which reflects the value of minority positions in KSA, Nigeria and Jordan.

New Large Shareholder:

The arrival of Elliott Investment Management in April 2026 is a massive signal to the market. Elliott an $80bn hedge fund, led by Paul Singer, is one of the world’s most formidable “activist” hedge funds. They don’t just buy stocks to watch them grow; they buy stakes to force changes that they believe will drive the share price higher.

Following the completion of their transaction on April 9th Elliott now holds exactly 21.67% of IDHC.

1. Why IDHC?

Elliott typically targets companies that meet three criteria, all of which IDHC currently fits:

Strong Cash Generation: As you can see above, IDHC is a “cash cow.” Elliott targets with excess cash they can use to pay higher dividends or buy back shares.

Undervaluation: Despite the 78% jump in operating profit, the market cap hasn’t really moved at $325M USD. 12X earnings is “cheap” for a dominant healthcare leader.

Trim the Fat: Elliott looks for areas where costs can be cut or where non-performing divisions (like perhaps the current loss-making branches in Nigeria or the early-stage Saudi expansion) can be streamlined. Both appear to be blossoming nicely but will we see big change?

2. The “Elliott Playbook” (What to Expect Next)

Based on Elliott’s recent moves in other healthcare firms (like Medtronic in late 2025), here is what they might push for at IDHC:

Board Representation: Elliott rarely stays on the sidelines. Expect them to request at least one or two seats on the board to “oversee operational performance.”

Increased Dividends: You noticed the dividend payout was only about 19% of profits. Elliott often pushes for a much higher payout ratio (40-50%) or a large one-off special dividend using that £23m cash pile.

Strategic Divestiture: If Nigeria continues to show “unrecognised tax losses” and slow growth, Elliott might push IDHC to sell that business and refocus exclusively on the higher-margin markets in Egypt and KSA.

M&A Discipline: While IDHC is currently in “expansion mode” (200 new branches), Elliott will likely demand that these new branches show a specific Return on Capital within 12 months, or they will push to shut them down.

Conclusion

IDHC acknowledges there could be difficulty ahead, but the re-entry price is compelling, and Healthcare is a core activity. The new shareholder, Elliott, adds a further dynamic and the 2025 results are strong. I’m back in on this.

IDHC has plans for further growth during the rest of 2026.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Might be that Elliott just got a great bargain on quite a small ticket for them. Certainly Actis, the party selling to Elliott, took a helluva bath on this line which they purchased in 2014 for $115m, 21% being worth today $60m ish at market - was it a permanent capital investment or was it an end of life fund selling (after 10+2 life) and therefore a forced seller? Unusually, perhaps, for many Elliott “activist” deals, the CEO here has a blocking shareholding at 27%. Is she a good operator? In that regard, the numbers look OK, but the company seems severely underpromoted to the capital markets.

PS there was a fraud in emerging market healthcare, NMC Health, a few years ago. Might be worth checking any softness in numbers and the quality of the advisory line up, although I imagine Elliott has done that already.