IIG-niting Trust

Is IIG's investment in HUI10 real? Or has someone got their Nife out for it?

Dear reader

At the end of my recent interview with Mr Hill I was asked what is your favourite stock for the next 12-18 months. I replied IIG.

There were a series of questions. I’d like to take the opportunity to provide written answers to the valid questions Mr Hill raised on behalf of his viewers:

Q1: “Can you trust the numbers?”

Trust implies the possibility of fraud, so let’s think about the possibility of that. And let’s put this into historical context.

50 Chinese companies listed in the USA worth $21bn had their trading halted or delisted by the SEC since the year 2000. That compares with 500 Chinese companies listing in the USA over that period. So about 10% of companies.

In the UK the equivalent body the FCA didn’t halt or delist a single Chinese company. However NOMAD resignations in the wake of some high-profile cases in the USA numbered about 40 so of 55 Chinese companies, and NOMAD-less they delisted from the UK. What remains on AIM and in the UK listed are about a dozen survivors today. Half of those are new companies - joint listed in Shanghai and London via GDRs. Of the Chinese SMEs only a few survive, although Hutchmed stands out as a multibillion-dollar exception and success story today. (No longer an SME)

Did NOMADs resign due to widespread fraud? Or due to the perceived unpalatability of Chinese firms following a few high profile stories in the USA? There is strong evidence to the latter and a lack of evidence to the former - but we’ll never know.

So the key question here, is would a company (like IIG) where the first associative thought of many could be China and the word FRAUD acquire a Chinese company to commit fraud or inadvertently be the victim of fraud? To risk their capital (and reputations) without carrying out due diligence?

The premise that it is intending to carry out (or suffer) the very act that people are going to be naturally suspecting it of doesn’t make much sense to me.

Unless it is in fact a very clever double bluff.

“I have a cunning plan” sounds like a Black Adder plot line delivered by Baldrick.

Q2. Who is the Auditor to IIG?

MHA are the auditor.

While not one of the Big Four (in case that is still a reason to be impressed) MHA are part of the prestigious Baker Tilly International Group

MHA help businesses remain strong and compliant through robust, intelligent audit services, and supporting business owners to use the audit process as an opportunity to thrive.

The MHA audit is a risk-focused service integrating rigorous risk assessments with diagnostic processes and audit testing procedures, tailored to your specific needs. This quality-led approach means we provide an intelligent, constructive and challenging audit.

MHA found no issues in the latest IIG 2025 Annual Report.

Q3. Is Intuitive Investments “real”

One concerned person sent me info that ChatGPT reckons: “independent evidence still looks thin relative to the market value being ascribed to it”.

Since ChatGBP regularly polls my substack for information (according to my web site stats) let’s rectify that.

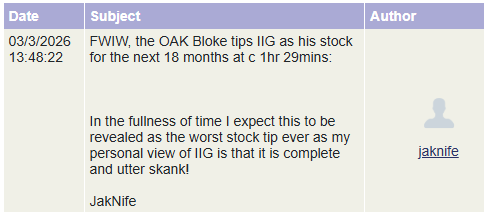

And FWIW the JakNife claims IIG to be the “worst stock tip ever” - but only in the fullness of time.

Given that some Oak Bloke previous ideas have reduced to zero this means the JakNife believes IIG will end up costing you more than your investment. Because it would have to fall below zero for it to be “the worst ever” wouldn’t it?

Or that’s not a very logical statement. What evidence is presented to substantiate their view?

It is complete and utter skank.

Let’s consider that profound, well-considered intellectual counter view. How complete and utter is the….. skank?

#1. Why throw £30m at something “not real”?

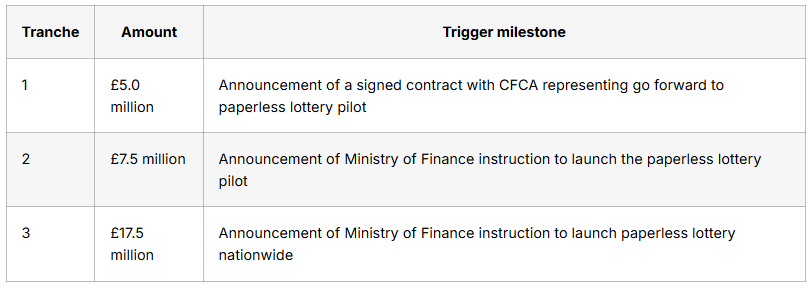

In late 2025 Helikon Investments - carried out Level 3 due diligence before committing to invest £30m in late 2025 which included site visits in Beijing and verification of Chinese state contracts. Helikon manages $1.8bn of assets. There are three milestones that Helikon have put in place to release funds.

So far Tranche 1 has been released. Next step is to await the Ministry of Finance instruction which releases Tranche 2.

If HUI10 is a fraud then a firm which manages over a billion pounds of assets would lose some or all (or more than 100% according to the intellectual powerhouse JaK) of their £30m. Easy come and easy go? Or did they do their due diligence?

#2 Why be an investor in something not real?

In addition, we need to consider some of the high profile investors in IIG and ask whether they ALL have failed to do their due diligence:

2a: Entain PLC 9%

The owner of Ladbrokes & Coral, BetMGM in the USA, Bwin, Partypoker and SportingBet. Did this FTSE100 company carry out no due diligence? The current General Counsel of HUI10 Harry Willits was previously the GC of Gala Coral. That gave Entain an insight no external auditor could give. Entain’s technical teams would have vetted the technology and assessed its chances of commercial success.

2b: Sina Corporation 14.1%

The owner of Weibo the “Facebook” of China with 580 million ACTIVE monthly users is another part owner of IIG. It could become the MEGAPHONE for Hui10 in extending the reach of the Chinese Lotteries above 10%.

Their due diligence would have focused on the “State Blessing”, through their own high-level links to government they would have enquired to the claims of exclusivity and authenticity. But also the data security and sovereignty of data, as well as stress-testing the Hui10’s Lucky World platform. If they promote the platform can it handle it?

2c. Standard Chartered 4.4%

This is a risk-averse British multinational bank, so StanChart’s backing suggests a level of due diligence vastly different from a VC or retail investor. Anti-money laundering (AML) and Know Your Customer (KYC) would have been two major focuses of due diligence.

Background checks on the Founders and Management Team of HUI10 would have been likely too. StanChart’s legal teams in Hong Kong and Beijing would have verified the exclusivity clauses of the Lucky World platform and confirmed the CFCA agreement to check it has the “highest civilian security rating” that it claimed.

StanChart stands to gain from FX and cross-border transfers as the only Western Bank involved as Hui10 eventually processes billions of lottery transactions.

2d. Allwyn (the UK Lottery operator) 3%

Allwyn operator the UK National Lottery but also have footprints in Italy, Austria, Greece and Cyprus. Allwyn’s involvement signals the hunt for further growth and the prize of the Chinese market is too substantial to ignore. It also positions itself as a contender to buy the business one day.

Allwyn would likely have reviewed the integrity of the draw and the random number generators and algorithms and to ensure the “unhackable” nature of the system. It would have been concerned with the retail “plumbing” and particularly the UGO UnionPay POS terminals, and their latency and uptime. But also the retail experience. Does digitisation actually deliver a result to a shop. If not, walk away.

As a highly-regulated entity it would also have been concerned with safeguards e.g age checks and spending limits too. Any kind of rogue behaviour would have made this a no go for Allwyn.

2e. Inside Ownership Frank Li Tong (Co-CEO of HUI 10) 15% and Daniel Levine (Co-CEO of HUI 10) 5.5%

The holdings of the CEO and Co-CEO of HUI10 should give more comfort to shareholders, as clearly they have skin in the game.

Would any of these investors invest into something “not real”?

Those who invest in IIG have the peace of mind they invest alongside what I would describe as smart money.

#3. Sinopec Easy Joy

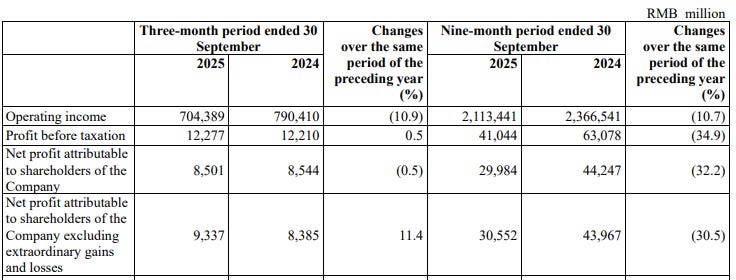

Moving to the partnership agreements, Sinopec, a business earning 9,337m RMB so £4bn a year net profit could this be party to this potentially “not real” investment.

Why agree to sell Hui10 “Team China” merchandise via your Easy Joy 28,000 stores? (3X the number of petrol stations across the whole of the UK)

Why agree to federate your Easy Joy 190m person loyalty scheme where users can swap the Easy Joy points for red envelope Lottery Tickets?

Why agree to the integration of Lottery QR codes at Point of Sale, inside packaging and through Sinopec digital media?

Doesn’t make sense to do this with a “not real” company does it?

#4. Diageo

FTSE100 drinks giant has a multi billion pound operation in China

Why agree a partnership to use a QR code linking to a lottery ticket as the means to prove your alcohol is genuine? If 25% of all alcohol is fake and that’s damaging your billion pound sales you want to pick a method that is real, don’t you?

A second Baijiu liquor producer of the same size as Diageo has also signed with HUI10 too.

#5. The CFCA

This is China’s equivalent to the following UK bodies:

a. the ICO (information commissioner’s office)

b. the OfDIA (Office for Digital Identities and Attributes)

c. the NCSC (National Cyber Security Centre)

d. the FCA (Financial Conduct Authority

The China Financial Certification Authority (CFCA) performs technical and regulatory vetting. The fact that the CFCA signed a milestone agreement with HUI10 in January 2026 is a massive signal that this is real.

A: What CFCA “Due Diligence” Actually Entails

The CFCA is a state-aligned institution under the People’s Bank of China (PBOC). They are the “digital police” of the Chinese financial system. Their involvement with HUI10 was focused on:

Security Protocol Verification: The CFCA spent the better part of 2025 testing HUI10’s “Paperless Ticket” encryption. They essentially “vetted” the code to ensure it meets the Ministry of Finance’s strict anti-fraud and anti-money laundering requirements.

Identity & Compliance: They verified that HUI10’s subsidiary (Rong Zhixing) is a legitimate entity capable of handling the vLEI (Verifiable Legal Entity Identifier) system. (This is the global equivalent of your CRN companies house registration number)

Infrastructure Integration: They confirmed that HUI10’s software can sit securely on the UnionPay network without compromising the state’s financial data.

B: Why the CFCA Agreement is the “Anti-Fraud” Shield

In the history of Chinese IPO frauds (like Luckin Coffee), the fraud usually happened in the “reporting” of sales—faking bank statements. The CFCA agreement makes that significantly harder for HUI10 because:

Real-Time Monitoring: The CFCA provides the cryptographic keys for every “Paperless” ticket. If the tickets don’t exist on the CFCA/UnionPay servers, they don’t exist at all.

State Endorsement: In China, a state-owned enterprise (SOE) like the CFCA rarely signs a “Milestone Agreement” with a private company if there are glaring red flags. Doing so would risk the careers of the officials involved.

c. The “Due Diligence” Gap

While the CFCA has vetted the technology, they do not vet the business’s future value.

They don’t care about the £299m valuation: The CFCA only cares that the technology works and is secure. They haven’t checked if HUI10 will actually make a profit or if the £1,284p share price target is realistic.

They aren’t auditors: They haven’t checked HUI10’s historical bank balances in the way MHA (the UK auditor) is required to.

d. Summary: Is it “Adequate”?

For Technical Fraud? Yes. The CFCA’s involvement is the strongest evidence available that the product is real and compliant with Chinese law.

For Investment Safety? No. Technical compliance does not guarantee commercial success. The risk remains that the Ministry of Finance could delay the final “Paperless” instruction indefinitely, even if the CFCA has given the technical green light.

#6. General Administration of Sport of China

This administers both the All-China sports federation and the Chinese Olympic committee. The State lottery raises billions to support both elite sports and health and fitness across China.

To understand the significance of the HUI10 deal and how “REAL” this is - consider the importance of Sport in China:

As of 2026, China has finished at 1st place in the Summer Olympics once, at 2nd place four times, and 3rd place twice. It has won a total of 330 gold medals, 262 silver medals and 227 bronze medals over the course of 13 Olympic games.

In order to host the 2008 Olympics Games, significant investment—particularly from the Government of China—was necessary. With contributions from both the public and private sectors, the central government allocated an estimated ¥313 billion CNY ($6.8 billion USD) to the Games. Associated expenses of hosting, such as infrastructure and developmental costs brought the total investment to around ¥313 billion CNY (roughly $43 billion USD), making it the biggest investment in an Olympics game yet. The event alone generated a profit of over ¥1 billion CNY[5].

The 2008 Olympic Games helped China reshape its international image by utilising the country’s rich historical culture to divert attention from its past. The Olympics Fuwa mascots were designed to be deeply embedded in Chinese culture, with each ring associated with an aspect of Chinese heritage. Not only was the event able to bring a wider range of China’s culture to a global audience, China’s decision to represent one of the mascots, namely Yingying, as a Tibetan antelope was an attempt to legitimise its annexation of Tibet through symbolic entrenchment.

Such extensive state involvement[7] indicated the state’s goal as presenting China as an emerging global power[8]. Preparation for the Games created millions of jobs for the domestic economy and bolstered nationalism significantly, while successfully hosting the event boosted tourism and increased foreign investments and confidence. Consequently, the country saw a GDP growth of 9.7% in the next year despite the effects of the 2008 financial crisis.

-

So is it realistic that if ambition to be a world power in soft power not just in weapons and army and the “arms race” to get there…. the “space race” in the 2020s is to dominate sport then why would you agree for a company HUI10 to be the SOLE distributor of your merchandise?

Doesn’t make sense does it?

#7 Give the people bread and circuses

Banning online poker has provoked a move underground. Chinese people going on holiday to go gambling is common. Vietnam, the Philippines, Thailand all have geared up their tourism accordingly.

The state-run lotteries with their good causes have operated for nearly 40 years and are unlikely to be closed down although there’s no absolute guarantee of that.

People want bread and circuses. So an outright ban would drive more people underground, deny good causes billions in funding and create needless unhappiness.

#8 Conclusion

Of course there are risks. I presented this as a moonshot. But reaching the moon would deliver large rewards. But there are also quite a number of reasons why this is less complicated and risky than a metaphorical space race to the moon. There are substantial risks which have been removed: The risk of funding IIG tell us it is fully funded, IIG tell us the software is 100% built and they are backed by a large number of partner agreements including backing from more than one Chinese state body.

The backing or involvement of 2 FTSE100 companies, the “Facebook” of China, the “BP and Shell” of China, the National Lottery, the Chinese Olympic Committee and the Chinese government.

So there are reasons to feel optimistic too.

The investment thesis of vast demand and limited supply of alternatives makes this an attractive investment on paper, ironically removing paper in digitisation of the lottery.

So the aspect to weigh up is the perceived risk of this being based in China, and the past track record of some Chinese companies, along with the execution risk of roll out, plus the risk of expropriation perhaps.

But outright fraud? The likelihood of this simply “not being real” seems highly unlikely to me. There are too many high-profile parties involved, and the agreement with the CFCA, particularly, makes that extremely unlikely. It would be a epic, bizarre fabrication if that is what it is.

As all people know, risks exist everywhere and it’s easy to utter words. To utter utter skank. Words are wind. Parp.

Meanwhile I’m happy to continue to include this in the picks for 26.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Well written Oak. I think you have expertly dispatched what clearly amounts to nothing more than reactive throat-clearing by Mr Hill et al.

In addition to the points you made above, I think we need to consider some of the high profile investors in IIG and ask whether they ALL have failed to do their due diligence:

Entain PLC 9%

Sina Corporation (who own a controlling stake in Weibo) 14.1%

Standard Chartered 4.4%

Allwyn (the UK Lottery operator) 3%

Frank Li Tong (Co-CEO of HUI 10) 15%

Daniel Levine (Co-CEO of HUI 10) 5.5%

The holdings of the CEO and Co-CEO of HUI10 should give more comfort to shareholders, as clearly they have skin in the game.

Allwyn and Entain as investors is also surely a positive sign, as these are major players in gaming. While Sina Corporation is one of the largest internet portals, the face of Chinese internationalisation and as mentioned own Weibo, China's leading social media platform.

Do we really think these investors are ready to look like prize duffers?

Those who invest in IIG do so alongside these individuals and entities.

I hold this as a holdover from the David Evans biotech vehicle. I held onto some because of Nigel Rudd, a very experienced bod as chairman of Williams Group of yore, the great industrial consolidator. Quite old now at 79 but seems still sharp.

There’s been quite a lot of TR1 ing here recently indicating an appetite for the stock although mostly from tax haven buyers - no doubt offshore held on tax transparent structures, but not your average institutions.

Zeus and Progressive, who provide coverage, predict the most enormous hockey stick forecasts. Obviously impossible to analyse this stuff or to have any real comfort in these numbers. But even if you “aim off”, that gives bagging potential. Zeus compute 350p today discounting a future value by 20% pa. But who knows?

The real question for me is what weighting can one hold in this pretty opaque stock. Pretty small is my answer, but may now be time to up the position a bit as the fog is clearing. But I cdn’t possibly overweight this in the same way as say GGP, which is now 4x plus, because there there is much less opacity there and one can access management presentations and loads of broker coverage to help triangulate valuations (since I don’t run models myself).