Introducing PTAL Petrotal

Introducing PTAL Petrotal

Will PTAL flower? It's amazing what a 8.5p premium can buy you.

When a reader asked me to consider PTAL based in Peru I knew an Oak Bloke article would have to involve some form of Peruvian cliche. An Alpaca, how original. Did you know reader, you can eat Alpaca? Half the fat of beef, quite gamey flavour, but a very healthy meat in anyone’s packed lunch. No, to the Alpaca? Ok, well let’s whet your appetite on Oil and Gas instead, and on Petrotal in particular.

PTAL produces 50% of Peru’s national production. It began as a sub <1000 BOPD 7 years ago and in 2023 produced an average above 14k BOPD with >20k BOPD at times.

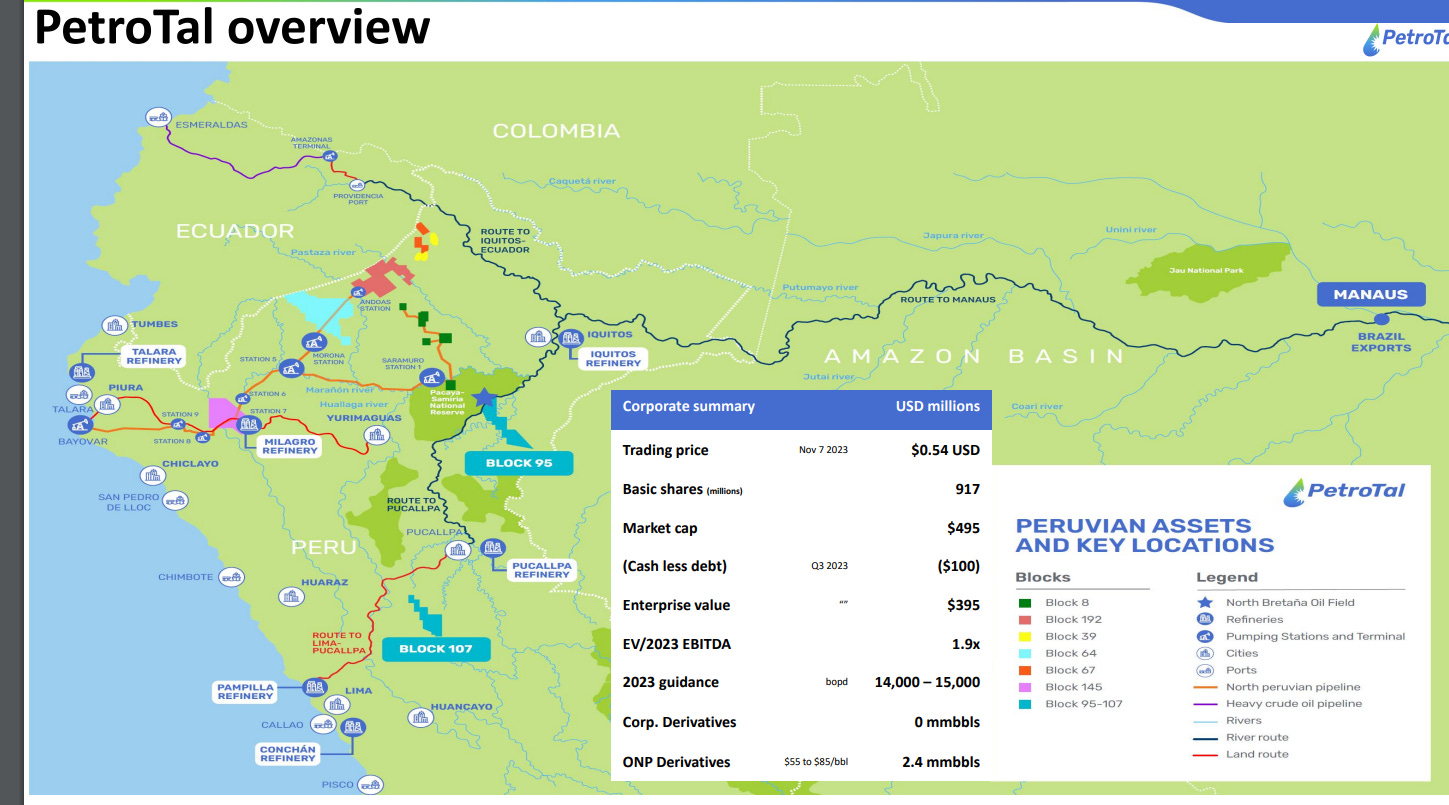

This diagram gives a birds eye view of the PTAL estate.

The company’s principal assets are its Bretana field at Block 95 as well as its future field Block 107 (both 100% owned) - and a Block 133 which they forgot to put on the map! These contain 29 million BOE and 68 million 2P resources with a further 170m BOE exploration/approval upside. So the core NAV is calculated on a DCF-basis according to Zeus at 71p a share (comprising 37p existing and 36p based on new drilling with a net 2p reduction for cash/admin). Auctus meanwhile see core NAV at 101p a share.

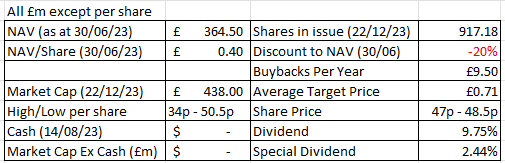

Rather than run my own DCF I’ll consider this from another angle. Premium to NAV. When we compare that against the market cap and the accounts we can see the 37p existing fully valued (with 3p cash makes 40p) and so you are paying 8.5p a share for the following:

8.5p a share premium to NAV buys you:

a - Drilling

A drilling programme which in 2024 will cost $123m and which is forecast to grow FCF by a further 10%-20% over the next 4 years. This is where production grows from ~19mbpd (19,0000 barrels a day) in 2024 to over 26mbpd in 2027. $138m FCF in 2027 would equal a dividend of 31.1% - assuming 100% capital allocation to dividends.

b - Free Cash Flow

FCF 2024 forecast as $87m or 7.4p a share (FCF is after development Capex as above)

c - A tasty dividend

A 9.75% annual dividend, 4.7p a share, so well covered by FCF (But bear in mind there appears to be a 10% witholding tax so possibly 8.8% net?)

d - and more dividend

A special dividend, gross 1.2p a share, still covered by FCF. So on a simple dividend payback basis, in around 15 months the 8.5p a share preium is “paid back”.

e - buy backs

A $12m buy back, costs the equivalent 1p a share, and is still covered by FCF, assuming a 48.5p buy price this is 3.7% accretive to the NAV (1p/share)

f - Upside exploration/appraisal

Future and further exploration/appraisal upsides within Bretana (32 mmboe), Iberia (27 mmboe) and O-K Well (111 mmboe) so 170 million barrels. Unrisked Zeus puts this at an astonishing 135p a share unrisked (and risked at 88p a share). Auctus goes further - puts the upside at 227p a share unrisked (and risked value of 143p a share)

g - Strong management

There are some O&G stinkers out there. So philosophically, PTAL’s management appear to show some strong priorities. First and foremost they appear to have a “national pride” as Peru’s leading O&G company and therefore take PTAL’s reputation very seriously. “Stakeholders” including indiginous communities appear to be listened to and considered. There are strong environmental credentials too - using modern techniques like horizontal drilling means your footprint in the rainforest is extremely small - and this is beneficial for PTAL too since the clean up and asset retirement costs are smaller too. But what comes through, too, is PTAL is clearly committed to shareholders.

h/ PTAL themselves see a 4X to their market cap by 2030. This interview reflects their ambition and how even the above assumptions of unrisked and risked value may prove conservative. Possibility of 100,000 BOPD (rather than 26,000 as discussed above) are mooted in this interview.

Risk and downside

a- Environmental disaster

A spill is an obvious risk. As I just spoke about they are careful in their activity. But the areas they operate would be front page negative news if something went wrong. No one ever expected the Deepwater Horizon disaster either from a company with the reputation of BP, nor the Exxon Valdez.

b - Peru

As a Hochschild shareholder of some years I know full well the political risk in Peru. PTAL’s approach is a 2.5% incentive. PTAL will give 2.5% of revenue to a social fund - if the natives don’t get restless. This seems like a clever way to approach the problem, and introduces some level of collective responsibility.

c - Rain

One of the biggest challenges is the fact that the oil is 100% shipped by barge. 90% east to Manaus in Brazil. At times during the year (Q3-Q4) the Ucayali river levels drop to a point that navigation becomes impossible. This risk is ameliorated by having multiple points/capacities for oil refining, including the majority which goes for export to Brazil (the city of Manaus), as well as using a competitor’s facilities (Petroperu, owned by the government) and a pilot option to export 5,000 barrels a day to Ecuador too. Traffic jams in Manaus are improving too. A barge-to-ship transfer has been arranged to reduce barge waiting times improving capacity by 10%.

d - Price of Oil

Some comparison of Auctus and Zeus show a difference between the NAV assumptions which illustrate how the value heavily relies on the price of oil. The assumptions made by the above two of $70 for the former and $65 the latter illustrate a risk but also potential upside. WTI Oil as I write is $74 a barrel. Will we see a declining oil price? Possibly.

Conclusion

When I was asked to consider this in the Oak Bloke Top 20 for 2024, disruption by low river levels, “early stage” and “high risk” were my (incorrect) beliefs of this share.

Closer examination show plans to tackle periods of time when river levels are low and this is clearly not early stage and instead is demonstrably good value and with a strong upside not reflected in the price. The 8.5p a share premium buys you an awful lot over at PTAL. Very pleased to be able to include this in the 2024 list.