Introducing R E A Holdings

Palm Oil - keepin' it REA-l in 2024

Palm Oil isn’t my usual form of investment. So when a reader suggested this for the Oak Bloke Top 20 2024 my first inclination was to reject this idea out of hand. So why didn’t I? One of my pre-check criteria was discount. I was gobsmacked to find the discount to NAV at 53%. This needed to be investigated. And on a second check I spotted a chunky dividend too! But will it survive my ESG or other screens? Let’s find out.

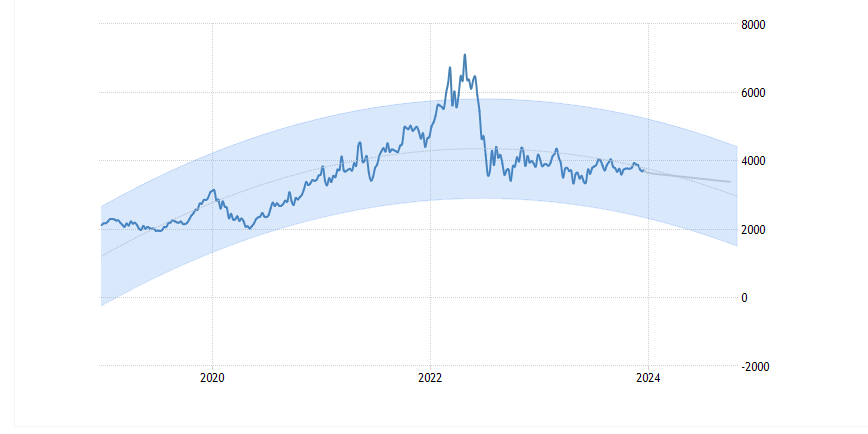

Big discounts to NAV are one thing, but P&L losses are another. I see CPO is traded in Malaysian Ringgit and is priced steadily at MYR3700/tonne and the forecast is steady prices in 2024. At these prices the business scrapes by profitably on an EBITDA basis (+$15.5m) but not deducting the “ITDA” to arrive at net profit. (-$15.2m)

There are 2 share classes ordinary and preference. The prefs (RE.B) are a 79p buy and the ords at a 70p buy. The prefs offer a 9% yield on their £1 face value (i.e. at 79p ask you get a 11.4% yield) but consider also there are arrears of 7p. So the equivalent of a 8.9% “special” dividend too! So a 2024 20.3% yield, reader!

Ordinary shares can’t receive a dividend until preference dividend arrears are brought up to date. Judging by the Prefs falling by about a 1/3 in a year there’s some doubt in the market whether these arrears will be paid. But based on the profit recovery and recent moves to reduce leverage (and associated interest payments) the market appears to have this worng.

About Palm Oil

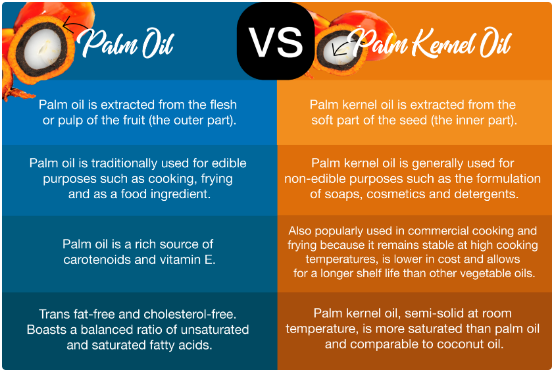

The business model of REA is you plant palms, harvest fresh fruit branches (known as FFB) and either sell those as is (at a lower price), or you process the FFB to produce Crude Palm Oil (CPO) - you guessed it at a higher price - as well as Crude Palm Kernel Oil (CPKO). What’s the difference between CPKO and CPO - basically these are the inner and outer of the palm fruit! The picture below shows the inner and outer where you get these from… who knew!

The two types of oil:

Profitability Risks for REA:

FX Rate MYR:$ - the MYR is down 10% over 5 years. $7.2m FX loss in H1 2023 of Net Profit $12.6m (there’s half the net loss explained!).

Climate/Crop Yields - the weather is out of the business’ control. Note a 5% drop in rainfall y-o-y.

Yields and extraction rates - with crops you are faced with variability as well as waste, spoiling, shelf life, product yield, processing rates. Lots of moving parts.

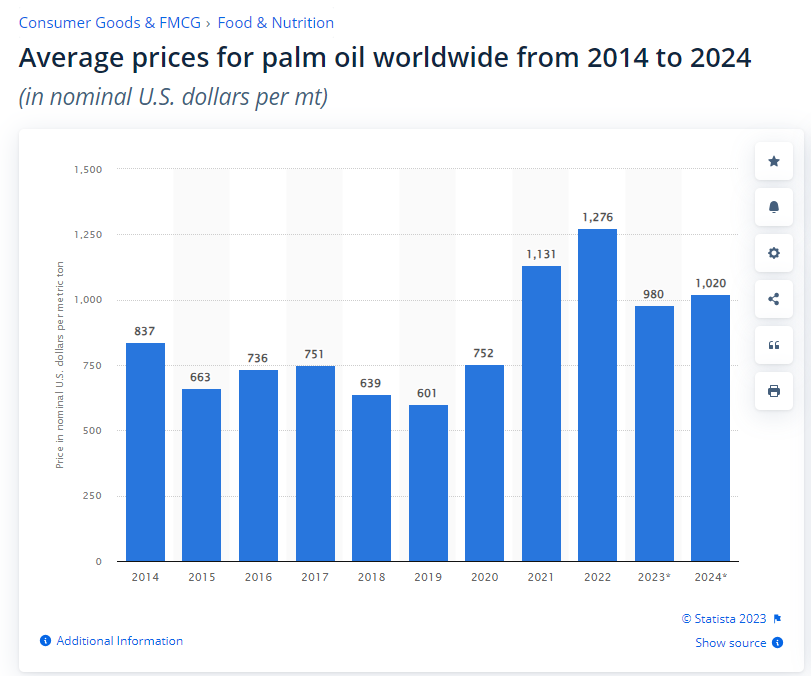

Commodity Price. We can see a drop in 2023 and depending on whether you believe Statista or Trading Economics it will go up or down in 2024.

Profitability Drivers:

Production in H1 up 7.5%. Further production increases coming on stream in H1 2023. In a “good year” with higher production of FFB, but higher conversion to CPO and CPKO, along with reversion on price “should” drive a = +$20m profit in 2024

Assuming FX is neutral or reverts could deliver a = +$5m profit in 2024.

Using the weighted 7.8% interest rate interest paid reduces $5.85m in 2024 following the $75m sale of CDM and Kaltim - see cashflow below. = +$6m profit in 2024

Certified Sustainable CPO sells at higher prices so they are reorganising to keep milling of sustainable and non-sustainable CPO separate, as well as improve the certification of FFB purchased from 3rd parties (i.e. small holders) = +$2m profit in 2024

Quartz Sand project awaiting licences in 2024. New revenue stream. Sand requires simple washing and mining will be undertaken by the Coal Mining contractor = +$1m profit in 2024

Commercial quarrying of stone commences Q4 2023. New revenue stream. Ready local demand for the stone. = +$2m profit in 2024.

Restrictions on new plantations should restrict supply growth and support prices.

Coking Coal is being mined by a sister company IPA, to whom REA have made loans.

The sale of 20% of Kaltim has a -$7.3m effect on profitability; the sale of CDM +$5.2m on profitability so a -$2.1m profit net effect.

Methane extracted which basically means nearly zero energy bill. Considering this the cost of sale is high - if the methane didn’t exist this would surely run at a loss? Surely there’s scope for driving down cost here?

RNS November 2023 - Simplification of subsidiary structure will have one-off costs but then lower costs in 2025 - assume neutral.

The net of the above is a potential for up to $34m net profit in 2024.

This puts REA on a potential 2024 PE 1.2

(Also is there a one off gain of $10m from the sale of assets - see next section)

Cash & Indebtedness Drivers

Gross indebtedness 30/06 at $204.2m is high. Good to see average interest rate falling 0.7% to 7.8% in the period. Debt due is successfully being rolled over period by period. However £30.9m non-bank Sterling notes are due 31/8/25.

Gross indebtedness due to fall $75m following the RNS 02/11/23 is for the sale of a young plantation (which had a P&L loss of $5.2m in 2022) called CDM to another CPO grower (called DSN) for $25m (i.e. at book) as well as $50m net for a further 20% ownership of a subsidiary called REA Kaltim (leaving REA with 65%). Since Kaltim is valued at $170m (for its 85% holding), the sale of 20% appears to be at $10m above book ($50m/0.85 = $200 x 20% = $40m).

Gradual future and further 14% sale of Kaltim to DSN by June 2028 - terms to be agreed. So long term REA holds 51% and DSN 49%. This “should” generate a further $35m.

Improving profitability as above, supports paying down debt perhaps by $34m.

The capital programme and depreciation appear to differ - approx $7m vs $14m. This lower sustainable cost of capital means the P&L depreciation loss is a paper loss and there is free cash flow to pay down debt.

Sale of assets - there remains $345m of PPE - Property, Plant & Equipment however very low disposal values - can any of this be sold and turned to cash?

Loan recoveries for Coal, Stone, Plasma gross at $60.5m

Sale of assets - could the stone/coal/quartz assets be sold off? (Perhaps along with assigning the loans too).

The net of the above is that REA (astonishingly) could be debt free by early 2025. Or “net debt” of zero at least.

ESG

REA is now ISO14001 accredited. It is a member of sustainable palm oil scheme and it is good to see they are actively supporting a wetlands scheme for the critically endanged probiscus monkey.

Good, too, to see REA buy CPO from 3rd party small holders and there’s a microfinance initiative to improve yields on existing land and improve traceability (RSPO sustainability certification rating) rather than to extend the amount of land these people use.

Conclusion

The news of the partial sale and the cash this generates as well as production, processing, simplification, new product sales, recovery of loans, all bodes well for REA. In fact very well, the November RNS of the partial sale changes the dynamic. The share price is only up what 3%-4% on the news. What the heck?

On the face of it the share price has been punished as it delivered a poor 2023 H1 result and facing a burgeoning debt pile. Debt means risk in peoples’ eyes. Also maybe delaying the pref dividend, and telling the ords they can’t have a dividend, and the apparent losses and falling prices for palm oil have contrived to make REA a bargain.

I nearly dismissed this one as garbage - and the 53% discount stopped me. As you look closer still, this is actually got some exciting potential. Ironically, while the 53% is notable the true drivers of this share rerating in 2024 is very different to the potential for asset stripping (although the partial sale at book price just shows the value is solid).

There’s potential for profit to recover strongly.

There’s potential for net debt to head towards - and potentially arrive at zero.

Final Thought

Should you buy the Pref or Ord? Pref probably. Voting doesn’t bother me, and the 20.3% 2024 dividend has me salivating, reader.

This is not advice

Oak

Been thinking about DSN's now 35% holding in RE's main asset; irrespective of RE's own performance, I think DSN provides upside here. I looked through their (extremely detailed) annual accounts, and almost all their assets are 99/100% owned, with the exception of a mere handful, the lowest holding of which is 66%. They are also very profitable, suggesting they won't accept average performance in this holding, and taking full/majority control is obviously their plan.

11.5p announced for pref shares today (RNS on the main RE. Listing)