Introducing TP ICAP

Part of the Oak Bloke Top 20

TP ICAP connects buyers and sellers in global financial, energy and commodities markets as a wholesale market intermediary, with a portfolio of businesses that provide broking services, data & analytics and market intelligence, with 60 offices across 28 countries, supporting brokers with award-winning and market-leading technology.

Let’s break that down - so TP ICAP is a intermediary business plus a data/analytics provider which operates across:

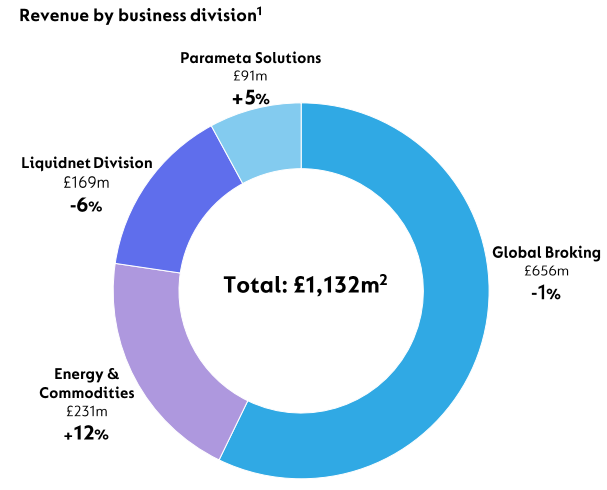

“Global Broking” - via its 2 Tullett Prebon and ICAP brands

“E&C” - which is energy & commodities via its 3 Tullett Prebon, ICAP and PVM brands

“Liquidnet” division - an electronic trading network of US$33tn equity & fixed income assets - via 2 further brands Liquidnet and Coex

“Parameta” division is Data & Analytics - via its Parameta brand

So about half of the broking is “rates” and this covers interest rates so options, swaps and futures for bonds, treasuries, repo, municipals. One imagines “the stock market” doing this but, no, actually this is done by a handful of firms where TP ICAP is the largest. Activity is driven by central bank changes and by economic good and bad news. For example when J Powell speaks TP ICAP’s tills go ching ching. As inflows and outflows into and between asset classes occur then TP ICAP’s tills go ching ching.

Fusion

As one reads about TCAP the word “Fusion” quickly emerges. About half of participants are using the Fusion interface and TCAP are driving this number upwards. Why? Good ol’ Cross sell and upsell. But not just of the divisional products (Global Broking, E&C and Liquidnet). Brands too. Like Daz and Arial brands compete with one another on the same supermarket shelf and ching ching the revenue - Fusion is the TCAP’s shelf. No silos here apparently. The same with regions. Via Fusion you can connect to liquidity pools globally and buy and sell from the same single “award-winning” interface.

But the cross sell doesn’t end there. Imagine you do 2 things: firstly, brokerage and you want a broker to buy and sell more stuff, but second is data and analytics which is delivered by its Parameta division. Hooking in Parameta as part of Fusion is a genius move. No silo here either. Charge brokerage to clients for buying and selling and then sell info about buying and selling trends of £217tn worth of transactions over 37 countries going back over 20 years. But also help with regulatory compliance, risk management

It’s also the case that while some products are generic, others are not. This is where brokers also use Fusion “drawing on its range of capabilities to construct the most relevant liquidity solutions to best service clients’ needs.” A custom futures product with a custom settlement date for example.

Parameta

Interestingly Parameta generates about 30% of net profit, and is growing the fastest (at least in 2023), with a contribution margin above 50% this is the jewel in the crown.

Also interestingly where brokerage can “discover” prices and drive liquidity Parameta can then follow. A great example of this is how gas markets work. Historically each country/region had their own index. TTF, UK, JKM and Henry Hub. But what happens when regions can buy and sell gas between themselves? i.e. Via LNG ships. This is what happens - parameta can productise the data to help generate a market as seen in this case study LNG global pricing

I’ve read talk about a Sum of the Parts argument where spinning off Parameta could be worth as much as TCAP’s current market cap. I think this misses the point of synergy. That the value of a market is liquidity and price discovery… and Parameta helps drive better discovery, provides revenue enhancement, and cheaper compliance.

Better information leads to more trading which generates more brokerage fees.

Why would you want to break that virtuous circle and sell it?

A further example is in E&C where the Net Zero green transition is an enormous opportunity for TCAP. Pricing and linking buyers and sellers of carbon certificates, methane, are examples…… I also listen to people babble on about the value of Blockchain to do all of this. Perhaps. But isn’t the true value to be able to audit the data, to be able to transact at low cost, and to generate a pool of liquidity? Buyers drive sellers and more sellers drive more buyers. If TCAP thought the most efficient way to host all of that was on Blockchain great. Right now they call it Parameta - and there’s a clear value that this division’s circa £180m largely recurring revenue and circa £80m EBIT doesn’t show. Especially as one off costs of £21m in 2022 relating to Russia mean this is really a £100m EBIT division - and growing.

Does Parameta not provide a USP to the brokerage platform too? Hargreaves Lansdown have been doing this for years reaping the profits. Not the cheapest charges, but providing the best info and the best service.

Liquidnet

I read about the “troubled” division. An acquisition from 2021. To me it just seems Equity has had a tough two years (20%-30% down) and 2024 should see an improvement. Integration with Fusion, integration synergies of £38m, an increase of banks connected on D2C from two to three all bodes well going into 2024.

Risk and downsides

The strength of TCAP that it prospers during volatility is also its weakness - the degree of success and failure is driven by market volatility and trends. Liquidnet is a good example of this. The business has a sizeable chunk of >£1bn debt, some due in 24-36 months and some with higher 7.8% rates. Yes, this is 100% covered by cash but the cash is restricted and used for trading so should actually be thought of “illiquid”. Having said that, TCAP is cash generative and is paying down debt so it’s not a critical risk.

Complexity and regulations are another challenge. I watched a documentary on FTX yesterday setting out how Sam Bankman-Fraud allegedly deceived the world. Technology obsolescence is an ongoing challenge too.

TCAP seems well positioned but it’s true this business is harder to understand a widget seller.

Valuation

Apart from the growing and 3x covered dividend being valuable, let’s look at whether 195p is good value?

£1.51bn market cap and 772.7m shares. 38.8% discount to NAV. Or 66% premium to TNAV (i.e. excluding goodwill). £30m buy backs assuming at £2/share reduces the discount to NAV to 39.5%. Also noting based on either a 3.5x P/FCF or 7x PE, this is cheap.

TCAP has doubled in price in 18 months to £1.95, but £1.95 is still a great entry price. I disagree that a spin off is next stage to realise value. Instead, continued execution of the strategy seems exactly the right course to take. Forecast earnings per share for 2024 are over 28p/share.

Conclusion

TCAP’s business model, if you think about it, is not dissimilar to Amazon’s “buy/sell that drives data and drives further buy/sell”. Offering a great interface, a compelling proposition via liquid marketplace, delivering a rapid and reliable service, and leverage your cumulative data advantage. The difference is you pay 8 times more for Amazon on a PE basis!

Putting TCAP even on 15 x Earnings (versus Amazon’s 57x) is conservative and puts this above £4 a share, also on a current yield above 7%. TCAP taking a 10 year view was well above £4 in 2017. Is this share a great example of “perceived declinism”, post Brexit? Did the market assume that Brexit would kill The City of London and by extension TCAP, in favour of Dublin/Frankfurt/Paris. Ignoring that TCAP trades pan Europe (and pan Global), seven years on actually the City thrives. The UK thrives. Seven years on, TCAP thrives. Ignoring inflation you can buy a more valuable business with a stronger technological position, better able to synergise its cumulative data advantage, covering a wider range of activities and positioned to address future markets in 2024. An exciting buy and a great share for the Oak Bloke’s Top 20 for 2024.

This is not advice.

Oak

Thanks for this one. Not one I would ever have considered, but it's piqued my interest, not least because of it's ownership of PVM which is a no lose money machine. For those with oil stocks, they also do a daily view on matters impacting oil which holders of oil stocks may find insightful.

Hmmm, I sold half last month, because it had doubled and had some other idea. Perhaps I shouldn't have; will now run the small rest. And no, I won't blame you if it doesn't work!