Is Andrada shaking the tin?

Is Andrada shaking the tin?

Q3 results vs Oak Bloke Forecasts

This morning’s ATM provided a Q3 update. There was a notable jump in the AISC for the quarter.

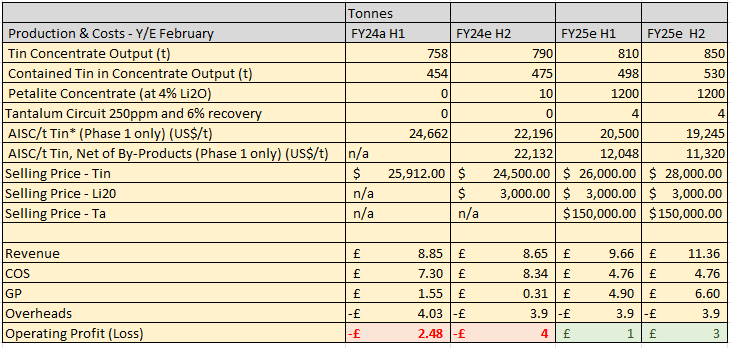

In ATM forever Afritin I made this forecast for H2 FY2024:

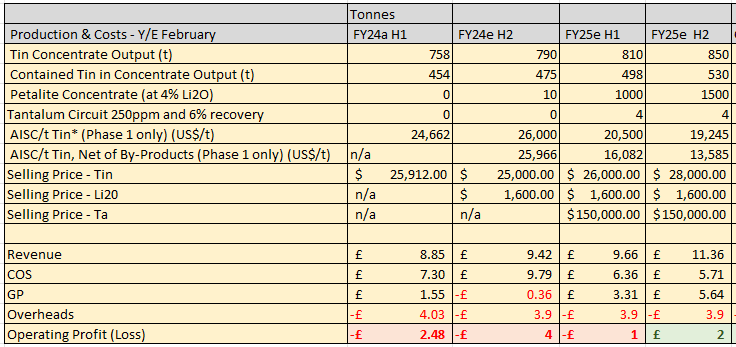

I am today revising my forecasts based on the Q3 update:

Key take aways:

The business remains on track to substantially reduce its AISC in the coming year but due to falling Lithium prices less than forecast. I’ve used the lower end anticipated selling price so forecasts reduce slightly, but upside remains.

The crucial point in the Q3 results is that C1 and C2 are down 3%-4% and heading in the right direction. The AISC went the other way, suggesting some one off factors like stripping costs. I’ve raised the H2 AISC. We know there are further optimisations are ongoing and Tin production is due to more than double through further investment and optimisation.

Successful production of 10 tonnes Li02 already achieved. (I had assumed this would be achieved by February ‘24)

The update that production of 250 tonnes/month Lithium and a Tantalum Circuit from March will be achieved. I’ve assumed in my forecast the lithium won’t fully ramp until May ‘24.

The news that 6.8% high grade concentrate is being achieved is significant. The orginal plan assumed 4% being the level achieved. This helps reduce costs further. It also gives optionality to supply Lithium Carbonate (potentially for EVs) as well as Petalite used for Ceramics.

Lithium meanwhile is down 81% YoY and the 1 year futures are flat. A new shortage is now predicted only in 2028 according to Trading Economics.

Lithium offtake Partner discussions are “progressing well”.

Conclusion:

Hannam say they see 6 bagger value at ATM where its EV/Resource (in US$/t of Li2O equivalents) currently sits at US$161/t, a 71% discount to pre-production hard-rock lithium peers. I’m not sure which pre-production hard-rock lithium peers they are thinking of (and they don’t say) because every one I know have had their valuations battered - like EMH, ALL, KZG. The other difficulty I have with this valuation is that works on a valuation as though ATM is putting itself up for sale - it isn’t.

Valuing ATM and unlocking the value here, in my opinion, instead requires scale. As can be seen in FY25e H2 scaling the by-products helps and starts to deliver profit. £2m operating profit gives a PE of 42 (ATM’s Market Cap is £83.75m). Ouch.

The CI2 project changes everything. Assuming the targeted 2000 tonnes contained tin can be achieved as planned (there isn’t a constraint either on resource nor it would seem on their engineering prowess thus far, nor with the Orion and Bank funding now in place) with a 2nd pilot lithium plant and pro rata tantalum recovery then we can see the effect on profit below. £18m Operating Profit or a PE of 4.5. Nice!

And if Lithium retraces even half of its recent fall and Tin returns to $38,000 (given the current disruption in Myanmar that’s not an unrealistic scenario) then Operating Profit doubles to £42m. A PE of 2. Very nice!

A valuation PE of 8-10 is realistic so ATM would/coule have a 2X to 4X upside, although paying down debt will delay any kind of dividends - so a gentler rise is likely.

Upside?

The CI2 Project is wholly based on Tin with 2 x Lithium Pilots of 250 tonnes a month. The current 3 drilling programmes listed below and offtake agreements are to significantly and subtantially scale Lithium i.e. from hundreds of tonnes to thousands of tonnes a month. We do not yet know the economics or commercials and a DFS (definitive feasibility study) would be required, so this is some time away. The pilot plants will be extremely helpful in modelling the flowsheets.

§ Uis (ML134): Resource validation drilling over the Northern and Central pegmatite clusters to enhance the current Mineral Resource Estimate ("MRE") classification of tin, as well as to establish the mineral potential for lithium and other technology metals.

§ Lithium Ridge (ML133): High-density drilling campaign at the historical TinTan mine for the development of a maiden MRE, and to enhance understanding of the lithium mineralisation within the identified high priority pegmatites.

§ Spodumene Hill (ML129): Drilling programme to delineate the higher grade spodumene zones within the B1 and C1 pegmatites, as well as on the mapped satellite bodies surrounding the main mineralised units.

I really like ATM, really like Anthony Viljoen as its leader, think today’s 5.4p ask is cheap, but don’t believe it offers compelling value in 2024. So while it’s a strong contender I have chosen to not include it in my 2024 Oak Bloke Top 20. This is a list I will be producing for entertainment and interest.

This is not advice. As ever, if you need advice my advice is to go and get it.

Oak.

Christmas Appeal

I hope you enjoy reading OakBloke articles and these are useful as you make your own investment decisions. My choice of picture and title shaking the tin, apart from being the usual “dad joke” double entendre title you’ve come to know and love is also because I’d like to ask for your help this Christmas.

The Salvation Army do a huge amount of great work supporting over 3,000 homeless including veterans and people who’ve fallen on hard times. Some people escaping their unsafe home. It’s not just for the homeless the Salvo’s serve a Christmas meal to lonely elderly people too. Please, please, please would you join me in helping the Salvo’s by donating something, even a small amount. DONATE LINK. Click my poll to let me know you’ve done that. And thank you. Merry Christmas.