JLP further thoughts

14th October 2023

Further thoughts on JLP and fast forwarding to 2025. Let’s try to predict that too.

Having now had an opportunity to listen to Leon’s presentation on Investor Meet Company I ran some further numbers.

My FY2024 numbers were glum. Profit drops year on year. What about the year after?

Assumptions:

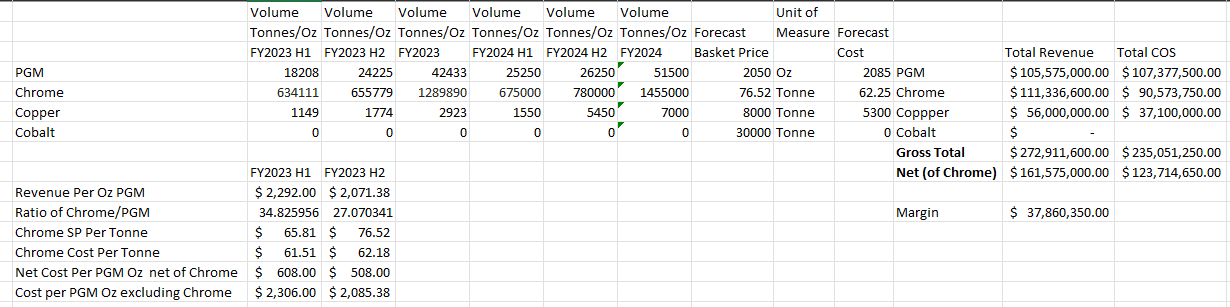

SA: In the 2 year plan towards 2m Chrome, and 100k ozs PGMs, I forecast a modest 60k ozs PGMs and 1.9MT Chrome.

Southern Strategy: I assume modest further growth in the Chrome price from $76 to $80. As described by Leon easy chrome is exhausted. Deep mining chrome is what’s left. And tailings :). I also assume modest recovery of the PGM basket to $2,400/oz. I’ll leave Seisnav to stun you with graphs but 15% recovery from a real current low point in 16 months isn’t unreasonable - I believe. Assuming, too, Roan achieves only 90% of copper nameplate by FY2025. Assuming Cobalt price recovers to $80k. The Cobalt circuit is activated and works at 100% of name plate.

Northern Strategy generates zero in FY2025 which seems the modest assumption of all.

So I think you’ll agree there’s upside scenarios to those assumptions, particularly the northern strategy which has wastes at least 2X the size of the Southern strategy.

The impact on profitability even with my professed modesty is astonishing.

Profit grows by over 5X to the FY2023 results to circa £65m net profit. A PE of 2.5

(Remember margin is hitting a fairly fixed cost - that’s why +$70m in FY2025 revenue = 5x earnings)

FY 2025 forecast:

FY 2024 forecast:

But will we see more than a modest jump in PGMs as being talked about on BBs?

I don’t think so.

Bulletin boards are awash with talk of a jump in Rhodium. Up 7% on the day. Unfortunately the forecast at Trading Economics for Rhodium suggests the 2021 spike will not return. Least not quickly.

Nor for other PGMs. A gentle return is all we can expect. Yet and yet. PGMs are stores of value as well as industrial. Gold is quietly going back to its prior highs. Will Gold race ahead and leave its PGM cousins behind? Is gold the only store of value?? Why could PGMs do much better than a gentle return - regardless of what’s going on with catalytic convertors for stricter emissions while PGMs also get used in new energy electrolysers generating hydrogen.

Why? I do genuinely worry about the level of governmental indebtedness in the US and UK.

In 2023 the UK is spending 4.4% of GDP or 9.6% of government spending on interest payments. When a spendaholic Labour government are waiting in the wings in 2024 isn’t that a terrifying combination? The Conservatives have set the bar on spending.

US is spending 1.9% of GDP on interest. Yet a lot of US debt is off the books at state level, inside Fannie Mae/Freddie Mac and in future liabilities. Since 2016 both Trump and Biden have set the US deficit on an unsustainable path in my opinion. Trump cutting taxes, and Biden spending. PGM prices could go mental. JLP does give an intriguing exposure to such a possibility.

Why else than trust in the US debt levels are bond yields continuing to increase despite a fairly clear trajectory that “higher for longer” just isn’t happening?

2 live wars (Ukraine and Israel) and a cold war (Taiwan) , and feuding are reasons are why not.

Conclusion: Linear thinking doesn’t usually explain the world. Did it explain very much any time period you care to pick?

At its worst JLP will continue to generate cash and generate a small profit while Leon aspires to grow. Change the metrics and suddenly JLP becomes highly profitable. It might even serve as a leveraged bet on profligate government. Its obsession with its own investment and its own growth might become rewarding. Someone criticised the annual report because it was full of words like “transformative”, “modular”, and “potential”. But show me another firm achieving a net $508 net Cost Per PGM Oz net of by products? Answer: they don’t exist. So is JLP actually transformative? Well based on its actual results it appears the answer is yes. If they repeat the actuals on copper net of cobalt and if cobalt and/or copper returns to its prior price levels or exceed them - for example Copper’s forecast with Trading Economics as pictured below suggests a higher price in the future. The same as chrome, politics, resource exhaustion, and deeper mining, means copper is harder to mine or extract. Yet we need bucket loads of copper for the new energy revolution.

ROI is all about the return - isn’t it?

I’m happy that JLP will generate a return. Perhaps a much bigger return than the market gives it credit right now.

These are my own thoughts and this is not advice. I wish you every success in your own investment decisions.

A happy weekend

Oak.

good update - it's a long term hold for me - perfect for the SIPP!

here is AMPLATS CEO on the future of PGM prices (from earlier in the week)...

https://www.miningmx.com/top-story/54679-amplats-ceo-says-metals-to-recover-15-to-20-as-market-prices-floor/