Kazera Investments (KZG)

All aboard HMS Diamond miner!

Market Cap £5.6m, Estimated NAV £12.1m* Discount to NAV 53.7%

*includes gain on disposal of Aftan to Xinjian

Kazera is a mining investment company with 3 projects:

1. 100% of a Lithium/Tantalite project in Namibia “Aftan” (but this is currently in the process of being sold)

2. 60% of “Deep Blue” a diamond sands operation in Alexander Bay, South Africa between 2 historic De Beers operations.

3. 60% of “Whale Head” the Walviskop Heavy Mineral Sands Project, which covers over five hectares of beach surf deposit.

Progress

Aftan

The current state of Aftan is that Xinjian (the buyer) has part paid US$4.85 million, and completion of payments is due by December 2023. The balance of the $13m ($8.15m) attracts 8% interest. The cash outstanding (let alone the accrued interest) is greater than the current market price of Kazera!

One of three things could happen next. If Xinjian default, KZG keep the $4.85m and can take back the mine. If Xinjian pay up then they have bought a great asset at a great price. The JORC shows an indicated/Inferred 110,000Kg Tantalum and 370,000 Tonnes/ Lithium. By the way, KZG get a 2.5% royalty on all future revenue generated from Aftan. At $30k/Tonne of Lithium, the Royalty is theoretically worth $277m (with no associated cost).

An obvious question therefore is who are Xinjian? Xinjian or HeBei Xinjian Construction CC was established in August 2013 in Namibia, but its parent company, HeBei Xinjian Construction Group, was founded in July 1952.

The group’s core business has been housing construction, decoration, industrial and civil equipment installation, plumbing, electrical and instrument installation, real estate development, overseas project contracting, labour export, import, and export trading. It has registered capital of RMB1.7 billion (£200m) and is listed on the Hongkong Stock Exchange ranked 365th among the "Top 500 Enterprises in China" in 2019 and ranked 18th among the "Top 80 Contractors in China" in 2018.

Intriguingly it has been reported that HeBei Xinjian was seeking to expand its offtake deals in Namibia’s Tantalite Valley in the Kharas region after offering a letter of intent to Arcadia Minerals Ltd to negotiate sales for tantalum pentoxide and lithium oxide from the Swanson tantalum/lithium project.

The plot thickens where HeBei (As the Arcadians call them) have also done a deal with Arcadia to part own Swanson (38% ownership) in return for $7m and to build a 20,000T processing plant. Swanson contains about 3x as much Lithium and Tantalite but over a much larger area (i.e. Aftan is the jewel in the crown). Now maybe they got the Hebei jeebies, ha ha, and don’t plan to pay up but it turns out they’ve spent far more than the $4.85m paid to Kazera, they’ve invested a much bigger chunk of money so walking away would be that much harder.

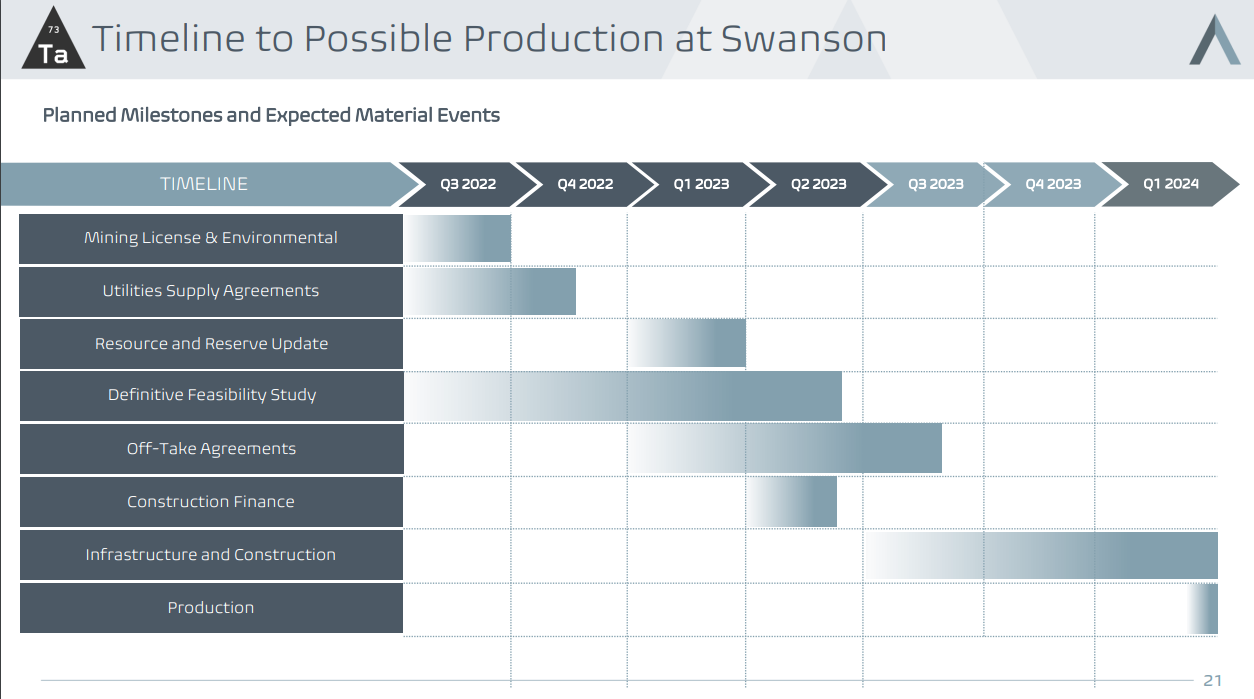

In fact on the 22nd September 2023 Arcadia updated the ASX that they are exploring further pegmatites at Swanson and report Hebei’s “Construction is ongoing”. So doesn’t sounds like Hebei Jeebies to me! Their presentation speaks to commencing production in Q1 2024 so not too long to know.

However is there a 3rd possibility of Kazera saying goodbye to Xinjian and g’day to Arcadia, strewth, those are some fantastic pegmatites, mate! Because Arcadia quite literally surround Aftan. Remember if KZG took it back, there are cash flows from Deep Blue and Walviskop to now support Aftan and some sort of half built facility at Swanson thanks to Hebei - fair dinkum!

DEEP BLUE

Deep Blue is “in operation” with some shiny new equipment probably bought with some of the above $4.85m (although $350k equipment was spent back in 2020). According to Align, the competent person’s report completed in April 2020 outlines an Inferred Mineral Resource of 208,000 carats at a grade of 6.0ct/100m³. This suggests something like US$60 million of top line revenue.

Walviskorp

Walviskorp is equally as exciting. Estimates of 1.5MT (million tonnes) of Heavy Mineral Sands (HMS) at a concentration of 49.9%. More than this there are MARINE DIAMONDS. These tend to be larger than inland diamonds and no other company has ever had both a DIAMOND and HMS mining licence. The mining area is in the surf of the beach. It is also the case that a HMS miner down the coast had a 2.7MT JORC and has extracted 9.5MT since 2014 (i.e. the waves naturally replenishes the resource!)

But subject to a current frustration. The South African National Nuclear Regulator have halted works just before they were due to begin, and require a permit for radioactivity. This is anticipated Q1 2024. The operation and equipment are all ready once they have the permit.

Forecast Income Streams FY2024 & FY2025 (Y/End is June):

These are my own estimates based on the KZG Annual Report/Accounts, numbers in the Align report, email conversations with KZG and my own conjecture.

1. $13m Cash receipts from Xinjian for the sale of the Aftan Lithium/Tantalum holding. (Cash equals 200% of the current share price… i.e. 1.2p cash/share). The carrying cost of Aftan was $1.8 million so there is an $11.2m profit on disposal – assume sale is booked in FY2024.

2. 60% Inland Diamonds from Deep Blue Minerals (Alex) (FY2024 GP $0.2m; FY2025 GP $0.8m*)

3. 60% Coastal Diamonds from Whale Head (FY2024 GP $0.3m; FY2025 GP $1.2m**)

4. 60% HMS from Whale Head (FY2024 GP circa $0.9m; 2024 GP circa $3.6m**)

5. 2.5% NSR for Tantalum/Lithium from Xinjian (FY2024 GP $0m; FY2025 $1.2m***)

6. 8% interest on o/s from Xinjian will be worth about $0.4m in FY2024 (End of Jan $9.3m x 8% x ½ assuming paid throughout 2023)

7. Less Overheads assuming to be 2X higher @ $2m

FY2024 Forecast Net Profit $11.2m (PE = 0.66X ..... £9.18m earnings PBT)

FY2025 Forecast Net Profit $4.8m (PE = 1.66X..... £3.7m PBT)

Y/E 2023 cash balance circa £8m based on earnings, full payment for Aftan

A target PE of 6 is not unreasonable which suggests a target price of 2.25p/share but noting the upsides below.

Notes to Forecast Income:

* - assumes zero diamond production Jan - September 2023; steady state therefter. $50k Gross Profit in FY24 growing to $100k in FY25 due to expansion.

** - assumes radiation issue curtails production until end of March 2024. Assumes no VHMs. $300k GP per month - sourced from KZG RNS.

*** - assumes production begins Q3 2024 based on 1600/tonnes annually of Lithium at $30k/tonne and at a 2.5% royalty.

Upside potential: (beyond forecast)

1. Can the HMS scale beyond the current operation? (6000 tonnes/month on a 1.5MT resource which replenishes by wave action 4X suggests a 67+ year mine life)

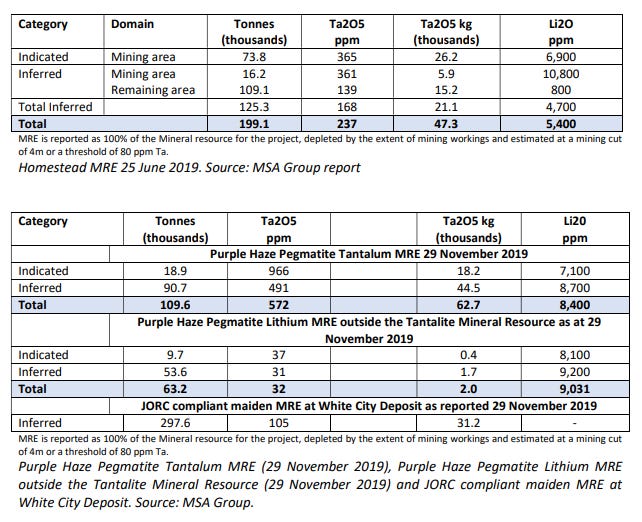

2. The 2.5% revenue share from Aftan has upside potential according to the Align report. The uppside to the aforementioned revenue share worth $277m to KZG based on 100% extraction of the JORC materials.

This is the JORC resource for the 3 Aftan sites that Align published in its research note:

3. The value of AMS introduced opportunities? (if you believe that's their intention!)

3b: A nearby beach to Walviskorp rich in HMS and 35X larger than Walviskorp has been mentioned in Align’s report called “Perdevlei”. I’ve spent time roaming the SA and Namibian coast (on Google Earth and Google Maps reader!) without finding this beach. Dennis has been very cagey about the status of this due to ongoing negotiations. But the caginess suggests it exists. Like some sort of paradise lost!

4. Will KZG get a takeover bid? AMS recently bought 29.9% of KZG at 1.5p/share from Align. If they offer 1.5p a share for the remaining 70.1%, that may be attractive to shareholders (as it’s a more than "100% upside" to the current price)

4b. Having sold its 29.9% holding, Align have since bought back. I think that tells you something too?

5. VHMs - Valuable Heavy Mineral Sands at Whalehead - rutile, zircon, and monazite - would double revenue with cost increasing by an estimated $66k/month ($4m equipment amortised over 5 years) so would take $300k/month profit to $533k/month - or $2.8m/year additional profit through VHMs. (58% increased profit)

6. Net Asset Value. I stated NAV was £12.1m which is £2.912m from the December 2022 Balance Sheet less the carrying value of Aftan plus the Gain on Disposal. However strip out that gain and the 2 remaining operations are in the books at £1.4m. I probably don’t need to tell you that there’s hidden value in the current NAV do I?

7. What if Walkiskorp is about to get even more significant?

7i:CREO Design's JORC noted valuable mineral sands (VMS) of Zircon and rutile accounted for 1.2% and 0.92% on the beach. Will it prove higher in the surf? These sell for much higher prices per tonne if they can be separated.

7ii: The company confirms radioactivity is mainly coming from the Monazite. But what does the Monazite contain? In Monazinte one can find Thorium (there is growing interest in using this as a nuclear fuel), and less often Uranium, but frequently rare earths are found in Monazite too.

(Source: https://en.wikipedia.org/wiki/Monazite)

Could there be commercial viability of Thorium/Uranium/REE extraction? If these are commercially available, this could be a further game changer. It's not unheard of. Iluka in the example HMS operations below extracts Rare Earths from HMS.

Example HMS operations worldwide:

1. Iluka 4.7% grades of HMS. Yet achieve an EBITDA margin of 53%. KZG has a 49.9% grade.

https://www.iluka.com/media/u3nbgflj/quarterly-review-to-31-march-2023.pdf

2. Someone getting very excited about Chilwa which has 3.9% HMS content. Because "There has been a global underinvestment in heavy mineral sands projects over the past decade." Nice to hear. Remember KZG has 49.9%.

(Source: https://www.sharecafe.com.au/2023/07/06/searching-for-heavy-mineral-sands-and-rare-earth-elements-in-africa/)

3. Image Resources "flagged an updated ore reserve at Atlas of 5.5Mt at 9.4 per cent total heavy minerals,". 9.4%? Nice but KZG is 49.9%.

(Source: https://www.businessnews.com.au/article/Image-Resources-upbeat-for-mineral-sands-production-in-2023)

4. Base Resources "The heavy mineral (HM) grade of ore mined in the quarter was lower at 3.0% (last quarter: 3.9%) due to the lower grades associated with the North Dune. 3%? KZG is 49.9%

(Source: https://wcsecure.weblink.com.au/pdf/BSE/02689519.pdf)

5. Grade for the quarter was 4.03%. Despite this "Cash generation has remained strong, supported by product pricing and shipments. In addition to paying record dividends and scheduled debt repayments, the business has continued to build cash. In line with our capital allocation policy, we are considering a share buyback of approximately $30 million. A further update will be provided with our H1 2023 results in mid-August.”. 4.03%? KZG has 49.9%

(Source: https://ir.q4europe.com/Solutions/Kenmare2018tf/3908/newsArticle.aspx?storyid=15823758)

I’ve probably not made by the KZG has 49.9% HMS too delicately have I?

Conclusion:

While there are questions and delays hanging over Kazera, if you agree there’s a fairly binary answer to those questions, and yes there’s delay, but that ends in a few months. It’s quite hard to explain quite why this has fallen to 0.7p other than people have just given up and don’t want to wait. It’s “nearly there” but has been “nearly there” for a long time. I guess that what you need to discern is will can it get beyond “nearly there” - as IT ALREADY HAS ACHIEVED IN ITS OTHER 2 OPERATIONS! (via Sale and via Operational Rollout). When there’s trommels, diggers ready to pounce, when there’s 12X Concentrations of HMS to any other listed Co. HMS operation I suspect there’s good times ahead to KZG.

This is not advice and I write this to help me with my own investment decisions. Good fortune with your own investment decisions.

Is the 2.5% royalty figure correct?