LINV-ord Christie

Is Lend Invest about to break records?

Dear reader

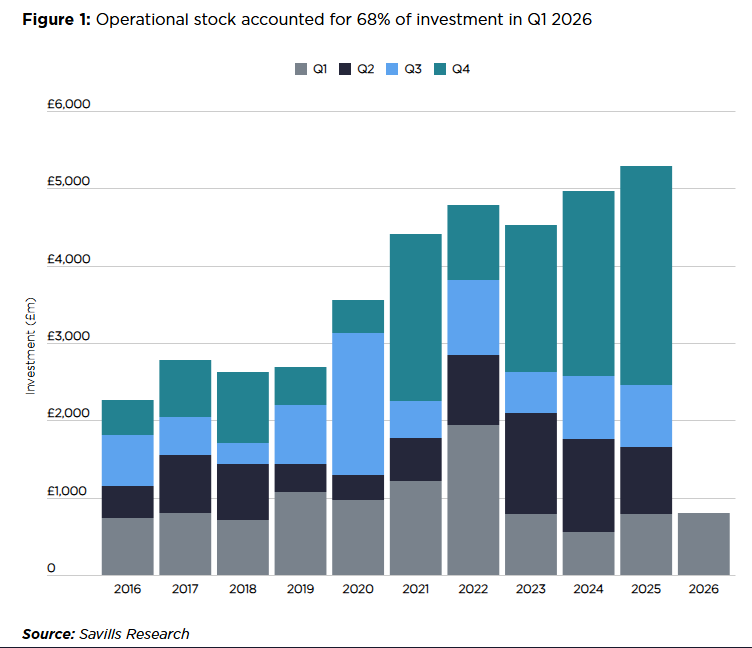

BTR is growing said Starling Bank. Their lending grew well over 20%.

BTR is growing say Savills. Here’s the proof:

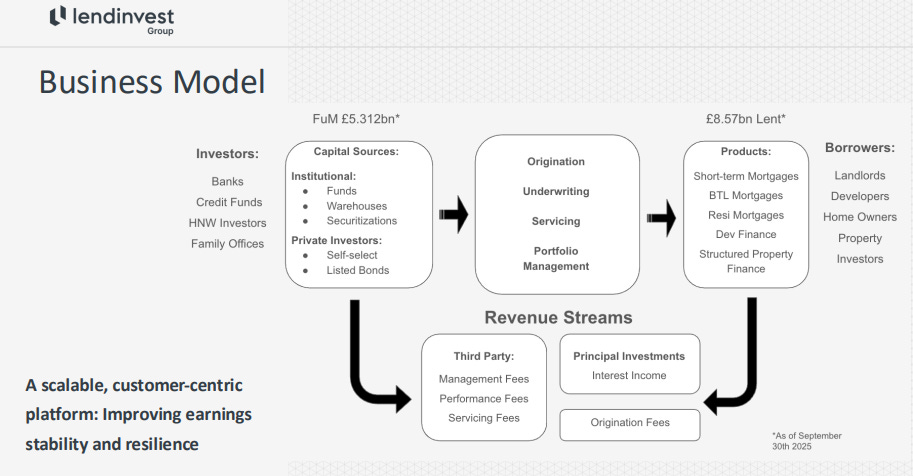

LendInvest (LINV) also lends to fund BTR. It calls it its “Mortgages” division. It also has a property development division called “Capital”.

LINV is a UK specialist property finance platform focused on buy-to-let (BTL), short-term/bridging, development, and residential mortgages. It operates a hybrid model with a shift toward capital-light operations (third-party funding, securitisations, and asset management fees) alongside selective on-balance-sheet lending for net interest income.

You can buy LINV at half price (to its NAV): A £72.7m NAV, a £63.5m TNAV and just a £35.7m market cap, is this a mispriced company?

>50% discount to its NAV.

LINV operates in two segments: BTL (buy/build to let/rent) and short-term bridging loans. You can see it has attracted a wide range of prestigious partners (and funders) so LINV itself is largely (but not wholly) capital light i.e. it lends other people’s money.

AuM are the assets earning income. Those can be on or off the balance sheet.

“On Balance Sheet” are known as its “Principal Investments” so this is where you borrow money (i.e. have a liability on your balance sheet) and lend money (i.e. have an asset on your balance sheet). You earn a net interest margin (NIM).

“Off balance sheet” is known as “3rd party funds” and, well, you don’t borrow money (i.e. no liability), but you charge a fee to a 3rd party and use their money to make loans - so you’re a service provider connecting borrowers with lenders. Typically the 3rd party will be a well-known Bank i.e. those above. But also Bondholders too.

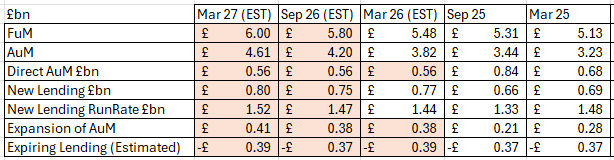

FuM is the pool of money you can use to lend. It is your “dry powder” you might say. Its recent trading update tells us that:

“The Group enters FY27 with its largest pipeline to date, providing strong visibility on forward lending.”

We also know that LINV has £1.66bn of unutilised funds to use for that pipeline, and expects to grow its funds by an estimated £0.5bn over the next year.

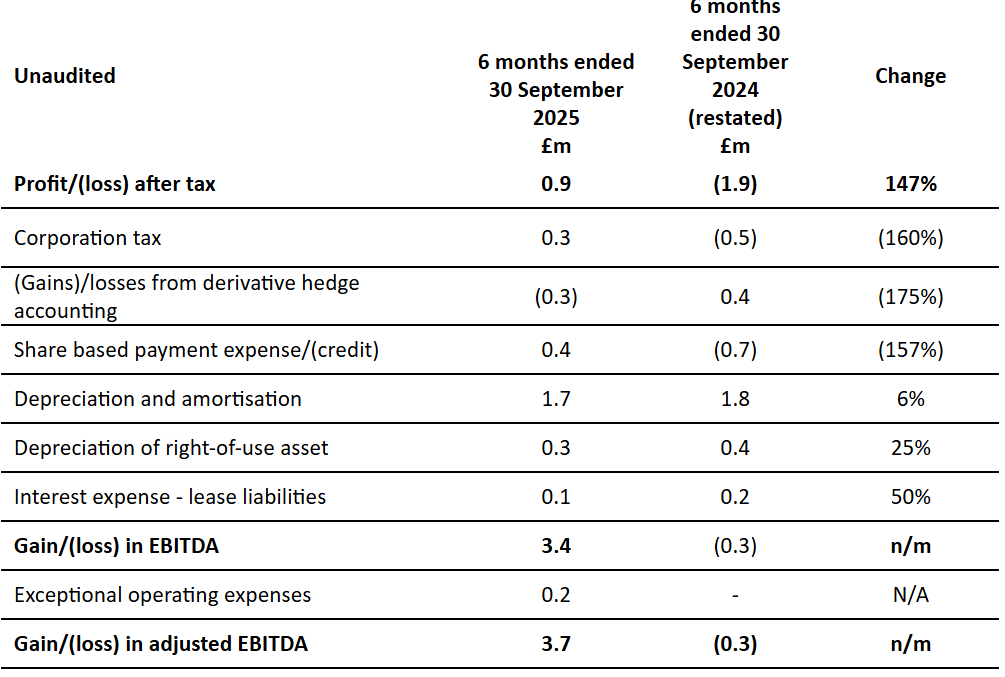

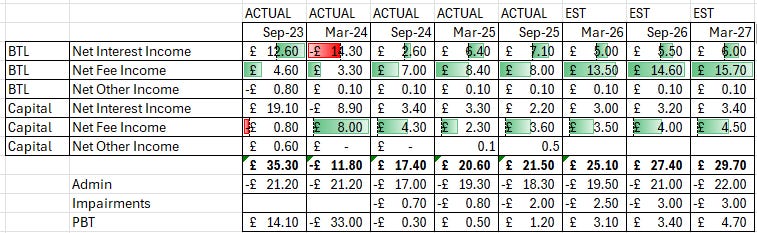

Where LINV turned profitable again last September, but on an underlying basis moved the dial by £3m adj.adj.EBITDA after I include the share-based payment back in to the numbers.

Free Technology

LINV boasts the best platform for complex mortgage applications and win plaudits for its interface.

Is it “just about AI and automation”? Err, no.

LINV’s approach isn’t about automating the underwriting decision; it’s about automating the administrative burden that slows it down.

The reality of specialist lending is that high-level experts often spend a lot of their day on “Data Friction, chasing AML trails, manual portfolio stress testing, and verifying messy asset valuations. That isn’t underwriting; it’s underwriters forced to do data entry and a poor use of talent. LINV uses technology to synthesise those disparate data points into a single, structured overview. This doesn’t replace underwriting intuition; it complements it.

Developing the platform has been an investment of over £60m over the years. That investment has been written down (impaired) by -£50m so you are paying £35m to get tangible assets (net cash and receivables) in excess of your buy price plus the IP/technology at zero price as well as a business generating profits in the price for free too.

LINV’s technology is a moving feast too where there are up to 12 changes are made (on average) per day.

About -£3m per year is amortised meaning the estimated £8.5m carried forward balance today will be fully written down to zero by 2029. It’s unlikely to actually get to zero in that further development will be capitalised but the fact that a large slice of “cost” is really a hidden asset - in the price for free.

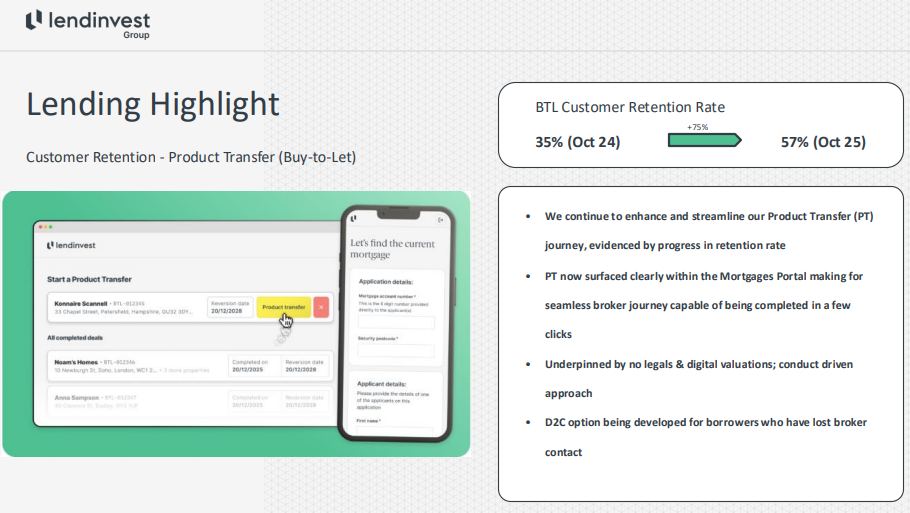

***56% retention rate

You might not consider 56% in FY26 to be all that good but it has grown from 19% FY24 to 35% FY25 to 56% FY26. It is not “normal” for specialist lenders to enjoy that level of retention. The rates are more typically 20%-30% since price and yield is the primary driver. What we appear to see is that people will pay for the convenience for LINV’s platform, since it does not offer the lowest price in all occasions.

Ability to transfer products is a big deal for example. Minimise hassle.

My analysis

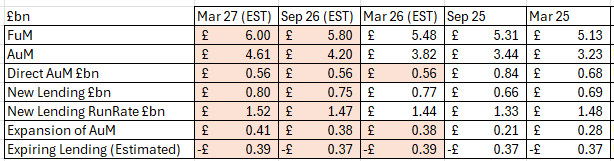

The latest trading update confirms that LINV now has funds under management (FuM) of £5.48bn up from £5.31bn and assets under management (money put to work) of £3.82bn as at 31/3/26.

This means that there £1.66bn left to deploy and LINV tell us in their trading update of their record pipeline.

Based on this my estimate is that we will see an acceleration of PBT over the next 12 months and beyond, as fixed costs are fully covered and growth drops straight to the bottom line.

This profit run rate puts this at a lowly 5.5X P/E based on the FY27 forecast.

Net Fee Income

Why am I convinced my profit model is correct?

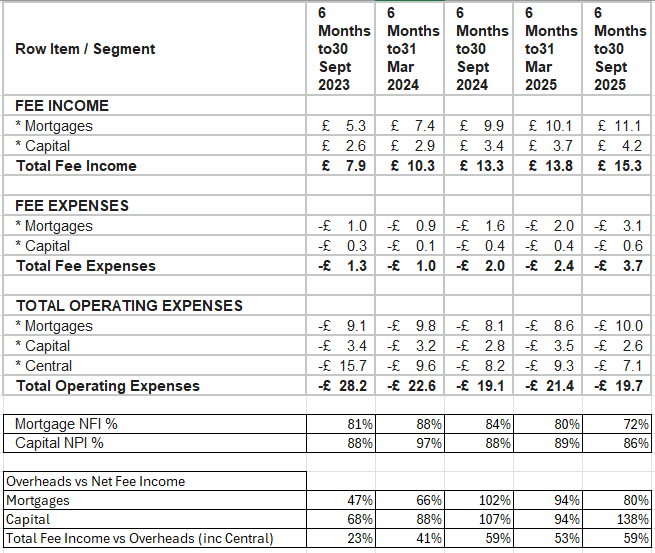

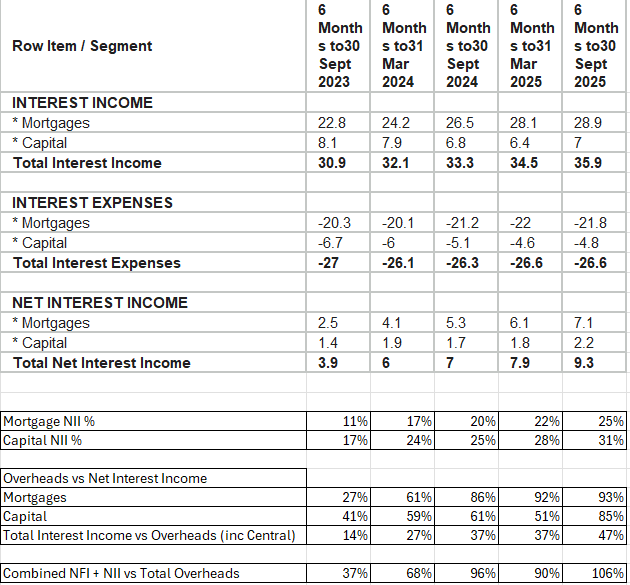

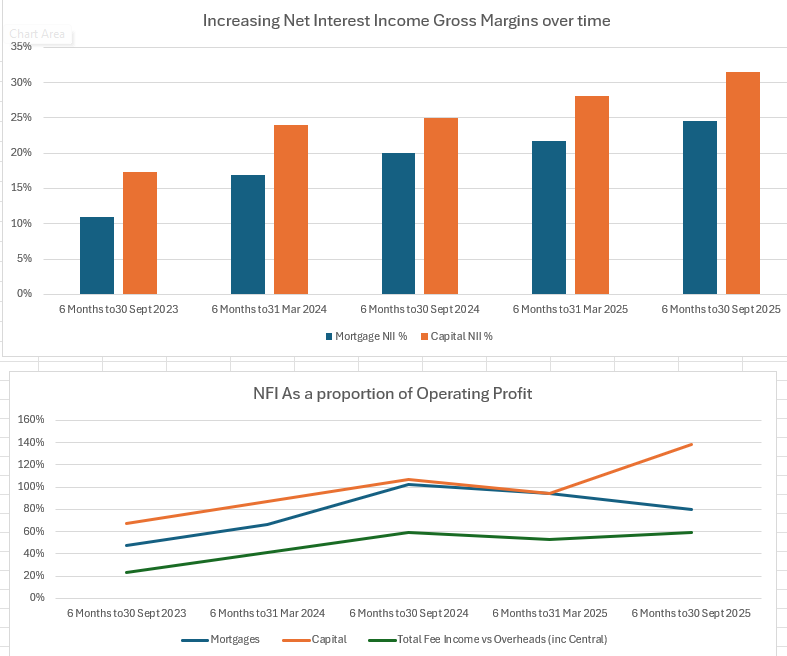

Analysing the past Net Fee Income (NFI) we can see this leverages in both segments relative to its operating expense meaning that NFI grows from covering 23% of all overheads to 59% in the most recent accounts.

At above 100% then you get Profit Before Tax, right? So NFI on its own and LINV would be toast.

But we also see the gross profit margin is 72%-88% for mortgages and 86%-97% for Capital. Almost pure profit!

Net Interest Income

Thankfully LINV also earns net interest income. NII. This is a commission from a 3rd party lender (like Lloyds Bank) and that is much lower GP margin…. but the margin has been growing - a lot.

11% grew to 25% in 1H26 for mortgages, and 17% grew to 31% for Capital.

But relative to the (same) overheads as NFI, the contribution is growing strongly. To the point where NII nearly covers all direct overheads so that the NFI is 80%-90% pure profit.

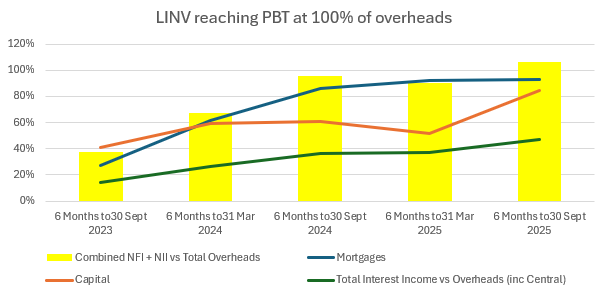

Add both together and you see the progression from 37% (i.e. -£15.7m LBT) to 106% (£1.2m PBT)

Conclusion

The year end results are due in July, and the rerate on this could take longer than one month since some exceptional costs from the refinancing of a bond means some up front costs landing in 2H26. But the trajectory appears clear. The need for more rental properties is clear.

The Renters Rights Act has created a moat for incumbents and yes has made the job of being a landlord more difficult and likely all of that drives up rents for the very people the government claims to want to support. The benefit for LINV is that this means more business, as landlords professionalise and in order to stomach the costs of red tape, they require scale and leverage.

Scale and Leverage is precisely what LINV can profitably provide through its winning mortgages/bridging loans platform, designed to be as friction free as possible and the proof is in the 56% of customers returning for more.

Regards

The Oak Bloke.

Disclaimers:

This content is for educational and informational purposes only. It does not consider your personal circumstances and is not financial, investment, tax, legal, or professional advice. Nothing here is a recommendation, offer, or solicitation to buy, sell, or hold any investment. Investing involves risk, including the loss of capital. You are solely responsible for your own decisions

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Great call by you regarding HGT.

Well, it certainly looks better value today at 25p compared to 200p 5 years ago! If you're correct with your timing and the improvement in fortunes continues then this should do very well. Thanks OB 👍