Livermore Peachy Existence

2024 results from LIV - OB idea #21 for 2025

Dear reader

2024 results delivers good and bad for this OB25 idea. Let’s consider both.

$0.042 dividend will be borne on the 4th July. Total returns since 2020 exceed 25p so over 50% the price of this share.

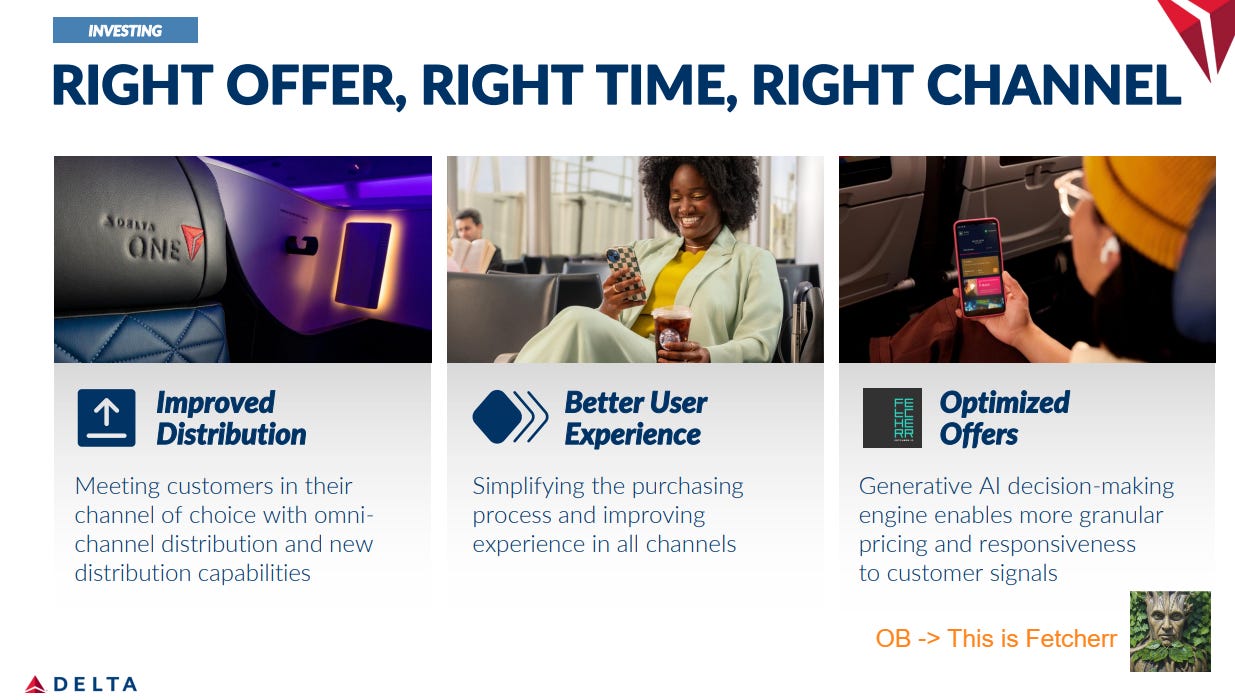

Fetcherr

LIV tell us “Our investment in Fetcherr continues to perform well” and “another bright spot in the portfolio”. It has proven itself at Delta Airlines and Virgin Atlantic.

Price optimisation can be survival, particularly in industries with little differentiation. Use Fetcherr to use data to capture the perfect price point for every transaction. The difference? An average 5% profit boost without changing anything else about your business.

Airline revenues, costs and profits based on IATA numbers in 2024 were $996 billion revenue, -$936 billion costs, and $6.14 profit per passenger. For 2025, IATA expect revenues around $1.007 trillion, costs around -$940 billion, and a profit per passenger of approximately $7.00. Margins remain thin.

Despite winning several awards, and gaining new airline clients, and despite expectations that it shall successfully execute on its large and growing pipeline in 2025 it wrote down the value of the investment without explanation. This was despite an upround at a valuation 2.5X higher in May 2024 (at a $250m valuation LIV’s holding would be valued at $28.77m)

In 2025 Fetcherr is extending its offering with a Network Engine that will optimise route planning, scheduling, and capacity management. Like Dynamic Pricing it will use an AI-powered Large Market Model (LMM) integrating real-time data to enhance operational efficiency and profitability. So extending “what should I sell it for?” to “what should I sell?”. It is also working on a bundle pricing engine, so extending “what should I sell?” to “what else should I sell?”

Phytech

Irrigation IoT specialist is another holding that is proving its worth. It combines monitoring of soil health, tree stress and fruit sizing. No other AgTech company offers this. The point also being that when you sell IoT that you can invent and sell more “things”.

This is a Dendrometer. It attaches to a tree trunk, branch, or stem to measure microscopic changes in its diameter. Think of it as a stethoscope for your trees. It listens to the subtle shifts in growth and water uptake that occur throughout the day accurate to the size of a human hair.

It’s not just water and watering either. Also frost management as Kaitlyn explains here:

The technology developed by Phytech is currently utilised by over 1,000 growers worldwide, spanning 18,000 farms in countries including the U.S., Australia, and Israel. These farms are significant contributors to global agriculture, producing large percentages of the world's almonds, and substantial portions of the U.S. apple and citrus outputs. Processing 25 million data points daily from over 45 million trees, Phytech's platform enables growers to make informed irrigation and fertilisation decisions, resulting in an average annual savings of 25% in water, fertiliser, and electricity costs, and an 8% increase in yield.

Essentially Phytech don’t manufacture anything and are a software house that uses kit. So it’s smart to work with those that make kit. Now in 2025 it does.

Strategic agreements mean this customer base got MUCH BIGGER in 2025. A partnership with Rivulis who has a strong global presence, including 20 manufacturing facilities, 3,000 employees, 3 R&D centers (in Israel, Greece and California) works with over 6,000 partners & 7,000 growers worldwide to provide full turnkey micro irrigations solutions for any, and all, grower needs from the individual grower to large corporate plantations in the agriculture, horticulture, greenhouse and mining industries.

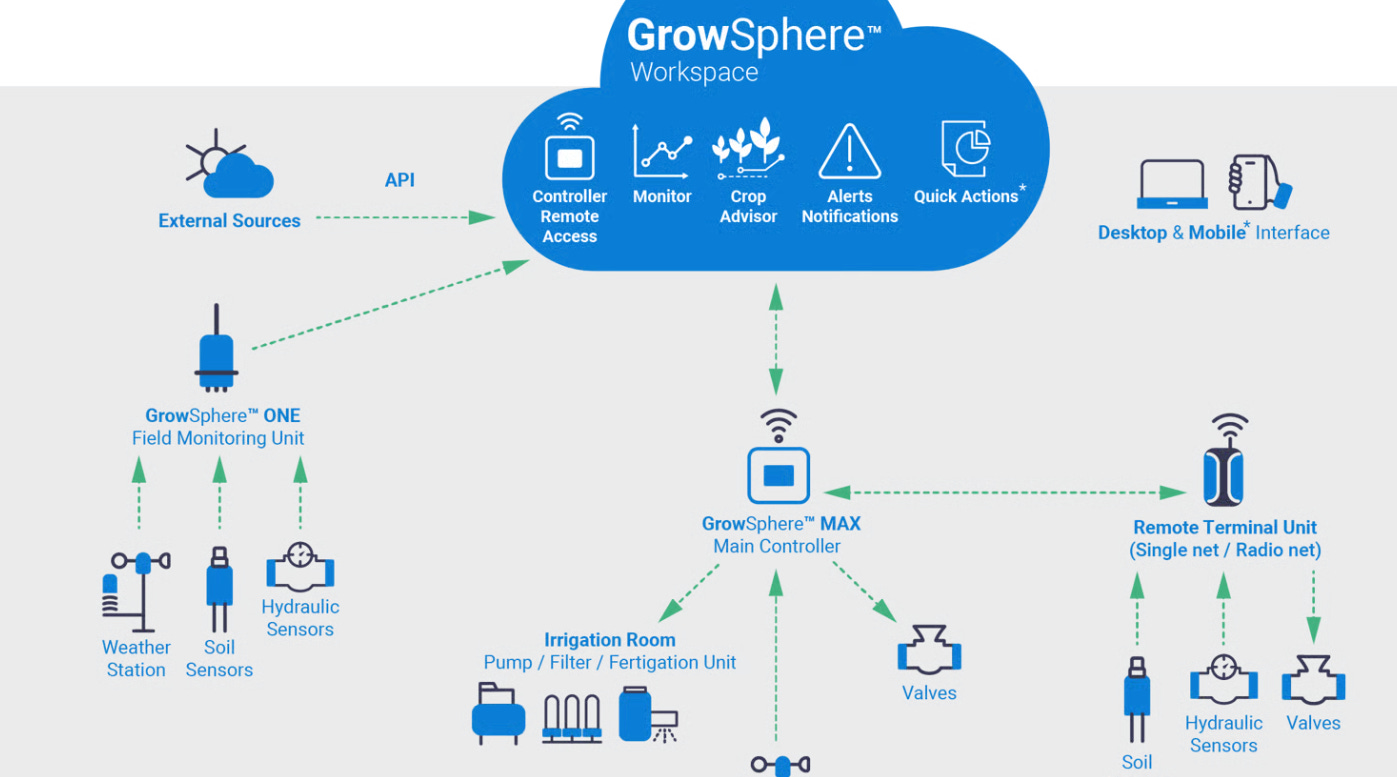

A 2nd partnership with $8.2bn annual revenue Orbia’s Precision Agriculture business is even larger. The world’s largest irrigation company and a global leader in precision agriculture solutions and pioneered the drip revolution, creating a paradigm shift toward precision irrigation. With 33 subsidiaries, 19 manufacturing plants, 2 recycling plants and more than 4,500 employees worldwide, Orbia Netafim delivers innovative, tailor-made irrigation and fertigation solutions to millions of farmers, allowing smallholders to large-scale agricultural producers and investors in over 100 countries to grow more with less. Phytech is being integrated into the Growsphere software platform.

Phytech's CEO, Oren Kind, remarked: "In a rare vote of confidence, Rivulis and Netafim have chosen Phytech to lead the digital farming offering for farmers around the world. This selection highlights over a decade of success, marked by significant revenue growth and the proven ability to scale in-field monitoring solutions and drive digital adoption across farm operations globally. This achievement is thanks to our growers, whose commitment to transformative technology has driven our innovation. Together, these relationships enable us to expand our unique hardware and software solutions, supporting growers and ecosystems worldwide."

Fixed Income and Loans

CLOs and US senior secured loans performed well in 2024. A high carry provided by these floating rate investments was attractive for yield oriented investors. LIV’s CLO and warehouse portfolio performed well generating $22m in cashflow and $10.3m in net gains during the year. Management had good success trading CLO BB and B rated tranches during the year. LIV also opened two warehouses in the first half of 2024 with Blackstone and MJX and converted them into new issue CLOs. Furthermore, LIV opened one warehouse with PGIM and another with Blackstone in the second half of 2024 at very attractive terms.

P&L:

If we consider portfolio income LIV generated a net 3p per share return in 2024.

You have to decide whether the PE portfolio is worth more than the 9.3p a share.

The underlying income from the portfolio of CLOs generated 9.1p per share in 2024. CLOs typically generate 15%-20% returns and while government bonds are probably not so racy there’s a nice range of income styles.

62.7p of assets vs a 49p buy price is a 27% discount to NAV. This is less than the discount when I included this idea, and is largely based on the strengthening of GBP and the reduction in Fetcherr’s valuation.

Strip out listed and cash and you get to a 29.6% discount.

If the $:£ moves back to 1.25 then this would add £9m to the NAV.

LIV is 90% owned by two Investors. Ron Baron is one (15%):

Noam Lanir the other (75%)

Conclusion

This contains two Private Equity holdings that I believe are worth more than their current NAV valuation, and the rest of the fund is a range of holdings which generate strong income and have performed well.

This idea was up 40% and now back to up 0% YTD. I remain optimistic that this idea will do well in 2025.

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

I recently opened up a Trader 212 account. On several occasions, have tried to purchase using the Trader ap, to no avail. One one occasion, was able to purchase only 235 shares at 49.8 p. Just wondering if anyone else has had a similar problem with liquidity of this stock? I think that it is currently attractively priced and I like it's investment thesis. Would value any insights on the write down on Fetcher. Thank you OB for all your time and trouble compiling the notes around the idea. The potential for optimal water irrigation in areas where crops in particular depend on desalinated water must be of great importance.