MKA - Mkango

Is its effect Magnetising?

Market Cap £21.4m, Share Price 8.50p/9p bid ask. TP 65p (215p unrisked)

Do you hold some shares and you’re not sure why?

Sounds awful to admit, but there it is reader. I bought MKA after reading a tip, about 2 years back, something about rare earths in Malawi, something about recycling rare earths in Poland. Something about Maginito (not one of the X-Men).

….And that its true value is many times that of its then current price. Should be exciting stuff. But it’s sitting on a loss. Should I stay or do I go now? Hold or sell?

So an AIM and TSX-V quoted Mkango Resources is focussed on developing its wholly owned Songwe Hill REE project in Malawi and a complementary REO separation hub in Poland, whilst also rolling out rare earth magnet recycling technology via its Maginito subsidiary to the UK, Germany and now the US.

The company is also exploring the Nkalonje, Mchinji, Chimimbe and Thambani projects elsewhere in Malawi, which hold potential for a variety of different minerals.

Its ethos is ‘Mine-Refine-Recycle’

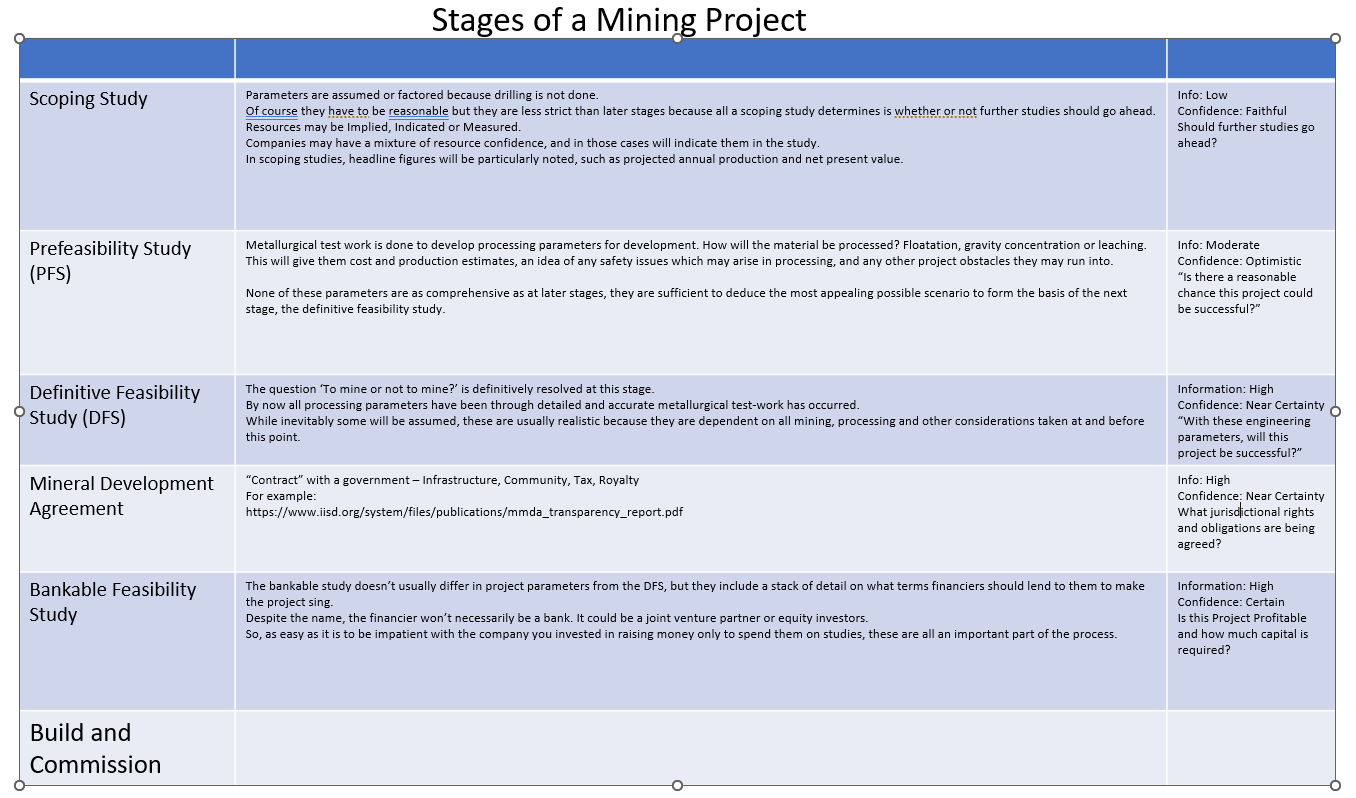

One of the challenges/risks of buying junior miner shares is the long process to progress a mining project. I’ve set out the 6 stages as it is helpful to think in terms of stages and timelines for these:

Mkango recently raised £3.5m via 28m shares equity at 12.5p to fund:

Mining: Songwe Hill has progressed beyond a DFS. The project’s Environment, Social and Health Impact Assessment was approved earlier this year. Mkango is now well advanced in negotiations with the Malawian authorities over an MDA that will set the fiscal and legal parameters for development and operation of the project. It will then progress to a BFS (or FID/Final Investment Decision) It expects to be in production by 2025.

Mining Cont’d: Last year’s definitive feasibility study (DFS) of Songwe Hill demonstrated the technical and commercial viability of developing the project as a long-life operation employing open-pit mining and flotationhydrometallurgical processing to produce an average of c.6,000t pa of total rare earth oxides in the first five years of full production contained in a mixed rare earths carbonate (MREC). Around one-third of the MREC will be NdPr oxides which are used in making permanent magnet motors for wind turbines and electric vehicles, and which are thus critical to the green energy and transport transition.

Refining: a site has been agreed for a dedicated rare-earth oxide separation facility in Poland, and discussions underway with potential partners to fund that project through full feasibility study.

Refining Cont’d: Downstream ambitions hold significant upside: Approval of the MDA will be a key milestone ahead of an investment decision and development. The Songwe DFS demonstrated the potential for robust returns (post-tax IRR of 32% and an NPV of US$559m), albeit using NdPr price forecasts that are above current levels. The DFS did not consider the value of Mkango’s proposed Pulawy rare earth oxide (REO) separation project in Poland, which would further process Songwe’s MREC product (removing the 27% discount thus improving the IRR to above 45%).

Recycling: The scale up of rare-earth magnet recycling initiatives in the USA, UK and Germany via its 90% owned tech subsidiary Maginito. The technology is called HyProMag where Mkango has developed a patented short-loop hydrogen-based process (the HPMS process) to extract, breakdown and demagnetise NdFeB magnets in scrap. HPMS is more energy-efficient compared with competing chemical-based recycling technologies (which face the challenge of having to first liberate magnets from end-of-life scrap components) and has a far smaller carbon footprint than prevailing primary supply production routes. Moreover, the ability to produce rare earth magnets or alloys directly from the recycled NdFeB powder is a key advantage versus competing recycling technologies.

Recycling UK: HyProMag is developing a £4.3m UK grant-funded demonstration plant in the UK with a minimum capacity of 100t pa of NdFeB products, and first production is expected in the next 3 months. In parallel, Maginito – via its Mkango UK subsidiary – is developing a pilot facility in the UK to chemically process recycled NdFeB powder and magnet swarf, complementing HyProMag’s short-loop HPMS recycling route.

Recycling DE: In Germany the scale up will unlock €3.7m of previously announced German and European grants to develop a rare-earth magnet recycling facility in Germany’s Baden-Württemberg State. Its 90%-owned German subsidiary HyProMag GmbH is developing a similar-sized facility to the UK (part EU grant-funded) in Baden-Württemberg State, with initial production targeted for next year. The facility will have a minimum capacity of 100t pa of NdFeB (neodymium, iron, boron) products, and first production is targeted for 2024.

Recycling USA: The US roll-out of HyProMag’s proprietary rare earth magnet recycling technology requires no initial funding call for Mkango (which gets a 45% share effectively for free), but opens access to a new, large and potentially lucrative market that is hungry for secure, domestic supply sources of rare earths vital to the country’s ‘green’ energy-and-transport transition aspirations. Establishment of the JV is another show of confidence in HyProMag’s innovative short-loop HPMS process, which offers key advantages over competing chemical-based technologies. The 50:50 joint venture with CoTec Holdings Corp (an ESG-focussed investor in innovative critical mineral extraction and processing technologies which owns the 10% balance of Maginito) to roll-out the former’s HyProMag hydrogen-based rare earth magnet recycling technology in the US. The proprietary technology will be sublicenced to the new JV company – HyProMag US – which will undertake a scoping study and then feasibility study of the potential for deploying three HPMS (hydrogen processing of magnet scrap) vessels and developing one magnet manufacturing facility in the US. Revenue is targeted within three years: The feasibility study is targeted for completion in 2024, and initial revenue is targeted for 2025/26. CoTec will fund the JV’s initial operations, including the feasibility study. Subject to a joint decision to proceed thereafter, it will also be responsible for funding (via shareholder loans) the subsequent development costs, estimated at £30-50m over the first three years. HyProMag US will also engage with the US Government over potential funding support for the project, and certain long lead-time items may be ordered early to expedite development.

DEFICIT

According to Adamas Intelligence, global demand for NdFeB permanent magnets is set to increase at a compound annual growth rate (CAGR) of almost 9% to 2035 (a tripling compared to current demand), driven by double-digit growth from the electric vehicle and wind power sectors. By contrast, Adamas forecasts that global supply will increasingly struggle to keep pace with demand over the same period owing to the long lead time of bringing new production online – it forecasts that production of Nd, Pr, Dy and Tb will grow by a CAGR of just over 5% to 2035 (a doubling compared with current supply).

Valuation:

ARC derive an NPV8% estimate of US$650m using a US$82/kg ‘basket’ price assumption to arrive at a 65p/share valuation assumes a heavy risk-adjustment (0.3x NPV - which is like discounting it by NPV26%) given the pre-funding stage, and includes just a conservative US$20m of nominal value for the recycling projects.

Conclusion:

I feel quite a lot happier now I have mine, refine, recycle in my mind. The fact that MKA has growing revenue streams is very positive too.

The deficit for REO and conservative valuation all seem to bode well for MKA too.