MPAC - arming for automation

Inline and Improving - T/U 2H25

Dear reader

Stabilised performance. Sounds inspiring? Read on reader read on.

For the patient investor who - like me - took advantage of the sentiment lull and gave MPAC a fresh look in October last year this now stands at a 15% gain in share price.

Did it report deeply exciting results? Or modest ones?

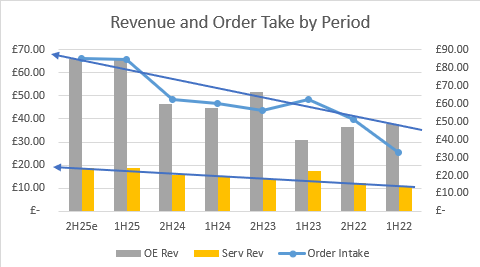

£170m full year revenue up from £122.4m in FY24 implies continued progress year on year but no large boost from 1H to 2H25.

However the upward trajectory thesis remains in play

Order intake continues to grow to end at £91.7m down from £92m meant an order intake of £85.3m in 2H25.

I’ve assumed a 66.6%/33.3% split of OE and Service below but I don’t know that that is the case.

But what isn’t guess work is that in 1H25 the OE order intake fell to £42.7m so we do know that the order intake for OE grew to £53.4m in 2H25 (making it 62.5% of the total order intake) …..and that’s 25% more. More OE means a greater future (follow on) order book of services, right?

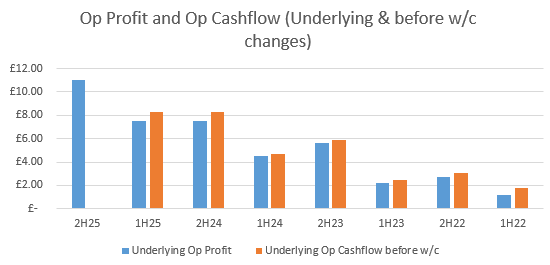

In my prior article I said following cost cutting meant we “should” see improvements to margin. This is confirmed in the t/u also.

Given the £5m underlying PBT in 1H25 and the expected £13.5m for FY25 that means profits grew to £8.5m in 2H25, implying an £11m operating profit.

Which represents substantial progress, and a full year £18.5m Op Profit vs £11m in 2024 and £7.8m in 2023.

The thesis of the OBBBA remains in play but it appears this could take several years and not just months, but the improving picture is clear to see.

Mpac operates in the substantial growing markets of Healthcare and Food and Beverage, although macro uncertainty remains, MPAC starts 2026 with good quote activity, as well as an improved offering through combined product lines from businesses acquired in 2024.

The opening order book, the prospect pipeline, and the actions taken in 2025 position the Group well to deliver on market expectations for the current financial year and beyond.

Adam Holland, Chief Executive, commented:

“The Group has delivered full year performance in line with market expectations, against the backdrop of macro-economic uncertainty, which led to customers deferring expenditure. We took decisive actions to reduce operating costs in the light of these near-term challenges. While we are mindful of the ongoing uncertainty in end markets, we have a strong and broad-based opportunity pipeline with clear order intake targets. Combined with a relentless focus on cost and cash management we expect this will allow the Group to make further progress in 2026. Looking further ahead, we remain confident in delivering enhanced shareholder value through the Group’s growth strategy, driven by innovation, operational excellence and outstanding customer service.’‘

The Group’s full year results for the year ended 31 December 2025 are expected to be announced on 21 April 2026.

Regards

The Oak Bloke.

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”