Nein to Digital Nine?

Sell off of Verne is announced Q4 23 - what does it mean?

Share price bid/ask 40.05p - 40.35p, NAV 101.6p/share

Mar Cap £347.8m Shares in issue 865.17m. NAV £879m.

What Rotten luck

DGI9 has had a run of back luck. The fund manager walked out.

Its dividend was secure. Then it suddenly wasn’t. Cut to zero.

It made a 6p “loss” in H1.Share price crashed and now on a huge 60.3% discount.

Why do I think there could be value here?

Follow the leader

First of all the fund manager has been replaced with a highly experienced new person. He started back in June so has now settled in. So the ship is steadied.

NAV loss in H1 23

There’s an element of FX loss £33.9m (about 2.9p/share), a dividend paid of £35.8m (3p) and that’s the approximate 6p loss. There’s also a negligible negative value movement -£5.1m and a positive reduction in discount +£5.8m.

H1 Movement in Portfolio:

So apart from a pause to the dividend, no actual reason to halve the share price.

In fact quite the opposite from a profitability point of view. This is an excerpt:

I love paused dividends. Everyone gets very upset about “losing” their dividends, and sell up in a huff…..that baby is going straight out with the bathwater….. if you paused and looked and saw actually 10% profits growth in 2022’s tough climate of supply shocks, inflation and malaise…. I think people obsess over share prices and get fixated on bad news headlines when under the hood things are not as bad. Certainly 40p is an interesting price for this IT.

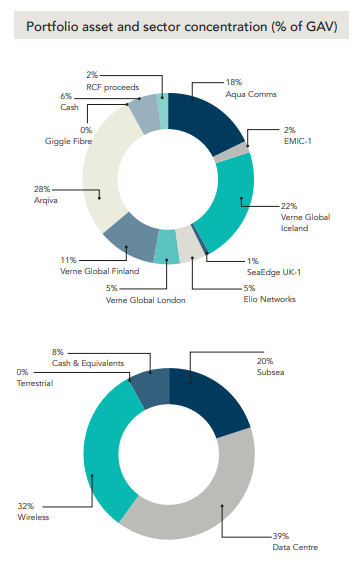

Bye bye Verne Global 38%

Second of all, Verne is up for sale and its sale should conclude in Q4. If Verne sells for its NAV price then the (I think unwarranted) 60.3% discount will be flushed out.

…the Board is assessing is a divestment of the Company's entire stake in the Verne Global group of companies ("Verne Global") (the "Proposed Transaction"). The Company received indicative offers from interested parties for the Proposed Transaction during the competitive process to syndicate a majority stake in Verne Global to a strategic capital partner (the "Syndication") and executed terms are expected to be announced in Q4 2023.

What you need to consider is we know there are multiple bids - why? Because it’s a fast growing and profitable asset. Although Verne is very cash hungry because it’s growing so fast…. it’s “too successful”! So while it needs cash to grow, it’s also true a lot of costs have already been sunk (presold), so there’s £21.2m of additional operating cash flow arriving over the next 6 months.

But also it is very ESG friendly. Data Centres usually burn a lot of CO2 through their energy use. Not Verne. Much like Iceland makes a lot of aluminium because energy is cheap now it’s providing data centres too….. because energy is cheap. It’s a prize asset and could sell for above Book Value in my opinion.

The current balance sheet (once you factor debt in) looks like this. “Investments - Debt” is “off the balance sheet” at TopCo i.e. held at portfolio company somewhere - mainly at Arqiva. So I’m factoring it in for visibility.

The left hand side BS is currently the make up of DGI9.

The 2nd is what happens when Verne sells (assuming for book)

The right hand Balance Sheet is what happens when DGI9 unlocks Arqiva. The balance sheet looks unremarkable but it’s a DOMINO EFFECT - read more below.

So the “39% data centre” part of the pie has been sold off in this scenario turning into Cash. Cash is now 47% of the portfolio.

Unlocking Arqiva

Currently this is the prediction of when cash flow comes on line (it includes the expected cash flow from Verne).

The 0.4X refers to the dividend cover from FCF.

As can be seen, the dividend is more than covered in 6-8 months time and 1.6X in due course. But Arqiva can’t pay dividends to DGI until the £163m Vendor Loan Note (VLN) is paid plus any interest (£7). So £170m must be found to unlock Arqiva. So the Verne 0.4X and Arqiva 0.4X cover are kind of mutually exclusive to one another. Disposing of Verne pays the VLN and unlocks Arqiva.

Optionality

An option is to recommence the dividend. At £50m this would be 14% yield at current prices. Or the company speaks to beginning buy backs - or do both. The remaining RCF debt is fixed to SONIA + 3.75% (9.05% currently) and restructuring the debt, to portfolio level is planned. Cash would fully repay the RCF saving 9% a year, or keep the leverage if greater than 9% returns can be achieved.

Accretive Value

With Verne gone, there’s plenty of opportunities to grow its portfolio companies. Arqiva, for example, is the backbone to the UK’s internet. It has a bright future as the Internet of Things (“IoT”) unfurls. The Investment Manager views this part of Arqiva’s strategy as a huge NAV accretion opportunity and expects it to be a key driver of value in the future. Smart Utilities already contributes around a quarter of Arqiva’s revenues and it is expected to continue to grow

Conclusion

This is an Investment Trust with some very interesting holdings and has been unfairly punished. It is also a very defensive trust. Even if the future holds a nasty recession these assets will continue to generate - and grow - income unless communications and internet were to somehow decline for the 1st time in history. Nowhere is that in the price.

This is my opinion and I hope you enjoy reading my thoughts but this is not advice.

All very cogent arguments. I held DGI9 and sold out when the nixed the divi. Why? Not because I was irritated at losing a few quid. No. It was because the Board had sworn blind for months on end that the divi was safe. And that against a backdrop where they had completely and utterly mismanaged the Trust, buying assets (like Verne) they who's growth financing they could not afford, and like Arqiva they could not afford full stop. So the issue for me is not the quality of the assets, rather the quality of the management.