Market Cap £13.44m, NAV £35.5m, Discount to NAV 62%.

Ventive

Leaky houses. Leaky buildings. Part of net zero is tackling the 16% of CO2 emissions through our buildings - which in the UK are some of the oldest in the world.

How? Better manage the inputs and minimise the outputs is the obvious solution.

Where better to turn if you wanted "best practice” than to use a tried and tested - and patented - approach featured on Grand Designs?

How effective is a Passive Ventilation with Heat Recovery (PVHR) system?

Real-life performance data from Horniman Primary School in Lewisham that was presented at the CIBSE Technical Symposium in 2017 has shown a Ventive PVHR unit achieving heat recovery with an efficiency of 94% across a nine-month period.

Longer-term testing has shown 72% thermal efficiency is regularly achieved, at a saving of 1,500kWh per year.

Presumably, reader, you know exactly how much a pint of milk costs and you know too, that a KWH is about 35p right now. So 1500KWh savings is in excess of £500 a year per household. Or much more for larger Commercial or Public buildings.

Interesting.

Ventive marries this proven and patented technology with sensors and with an integrated heat pump which will not only ventilate and heat a home but cool it also. This is a major USP which other heat pump providers don’t appear to be thinking about….. remember reader what I said at the beginning if you control the inputs and the outputs…. I know a few people who’s installed airconditioning and bemoan the cost.

Today, the RNS from NSCI announced £900k of funding. But, reader, the true number raised is actually £2.5m and also that it is partnering with Pipedrive and QM on building a factory to begin production.

In other words they are bringing partners to reduce risk, and not reinvent the wheel.

Following completion NetScientific will hold 11.0% of Ventive on a fully diluted basis, which equates to a post-investment fair value of £893,000, a substantial increase of 1,617% from the £52,000 31/12/2022 valuation (MOIC 16x). In addition, through EMV’s capital under advisory NSCI gets a potential upside (fees) with the 23.8% of the fully diluted share capital as managed capital.

-

23 other investments

There are several other holdings which are as exciting as Ventive.

Q-bot

Q-bot is in the same space as Ventive. It insulates homes using a device reminiscent of Transformers. Its Spraybot (unofficial name) has achieved 24% reduction in heat loss in studies (so another £300-£500 a year savings potentially on an average home) and has raised capital 2 months ago - this time just at a 9.5% increase for NSCI (£0.4m gain). However this has grown from £1,025,000 in 2021 to £4.1m (so a 4X return for NSCI).

Q-bot is growing fast - 60% in 2022 and 80% expected for 2023 - and has an addressable market of around 10m homes just in the UK where the alternative is a very manual process of lifting boards and placing insulation. It now is expanding in Europe and the US.

NetScientific’s holds 15.3%, and its subsidiary EMV has 30.7% of Q-Bot as capital under advisory. (Fees and upside)

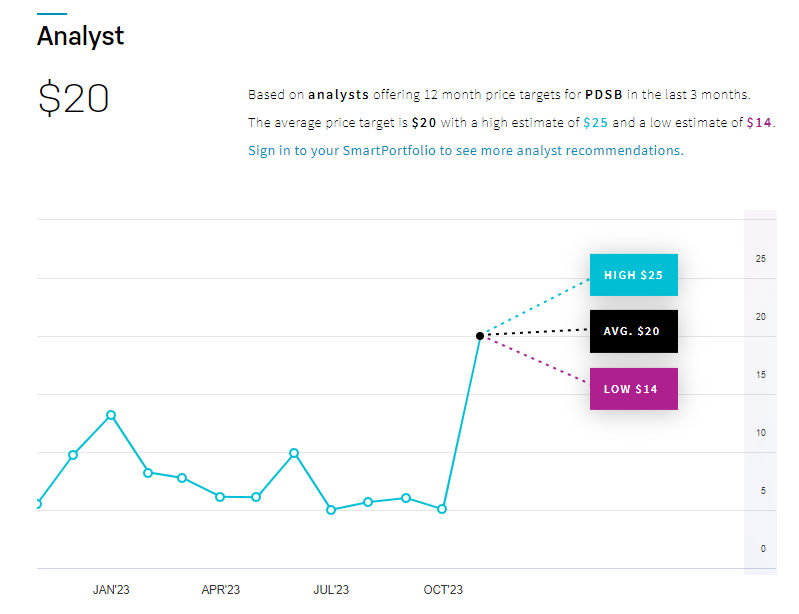

PDS

PDS Biotech Inc. (NASDAQ:PDSB) is NSCI’s only current listed holding. It owns 4.4% of PDS. PDS has made substantial clinical progress across 4 Phase 2 trials. It has announced a Phase 3 trial, and interim data indicating 12-month survival rate of 87% with PDS0101 in combination with KEYTRUDA® (pembrolizumab) for head and neck cancer patients.

For anyone (like myself) who own Avacta and is excited by the potential of the “targeted delivery” potential of its preCISION platform, AVA6000 Doxorubicin I would suggest PDS are achieving something not dissimilar - but with Keytruda instead of Doxorubicin. And by supporting the action of T-Cells rather than targetting chemotherapy….. using a proprietary cationic, lipid-based nanoparticle platform technologies are designed to harness the power of T cells to successfully recruit, train and arm T cells to execute a precise attack against the targeted disease

The analysts all believe in PDS citing a 3X to 5X target to today’s $4.67.

It has reported tremendous progress and results but the sentiment is negative due to concern about price controls being brought in by Joe Biden. (Given the US election is 1 year away this concern will rapidly diminish I think)

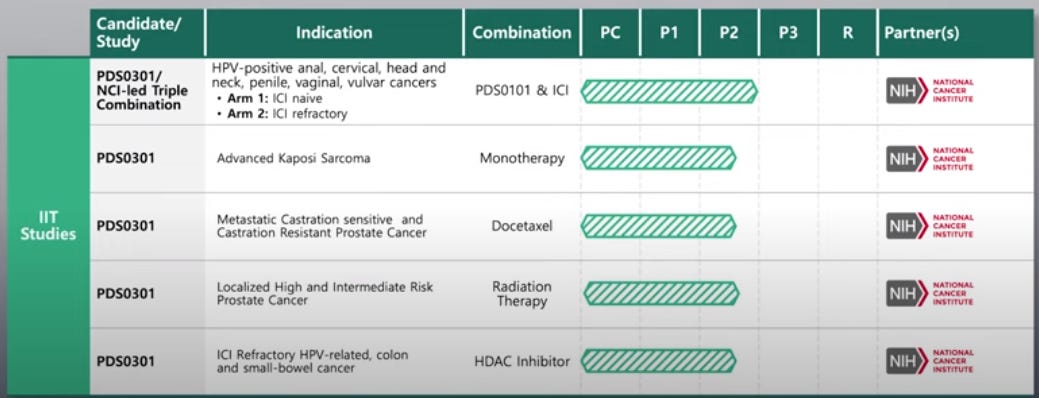

It’s PDS0101 is not its only drug in its pipeline - it has a universal flu candidate and another cancer fighting drug called PDS0301.

Combining PDS0101 with Merck’s Keytruda appears to double the level of survival.

09/11/23 update - and triple the length of time people survive advanced cancer - 36 months instead of 7-11 months. And 20 months instead of 3-4 months.

T cell infiltration

ICI = Immune checkpoint inhibitors require either pre-existing anti-tumor immunity or the presence of T cells in the tumor microenvironment to be fully effective. Certain tumor types like melanoma, are therefore most likely to respond to ICI treatment.

PDS CEO puts the case for PDS0101 here:

DeepTech Recycling (DTR)

Plastic is made from oil, right? So what if you could turn plastic back into oil? That’s the patented technology on offer here and NSCI own 30% of it.

NSCI stepped in and acquired this without paying any cash simply providing advice and services in exchange for 30%. EMV’s value creation team, has focused on consolidating assets and intellectual property, further R&D, assessing market opportunities, and starting the company’s commercial roadmap.

DTR is an aborted IPO due to be floated at £60m (making the NSCI stake potentially worth £18m or 1.3X the market cap of the whole of NSCI) and if you look at the insolvency practitioner’s documents the book value of equipment and fixed assets were worth £10m before considering the value of the patents.

DTR have developed advanced and environmentally sound technologies for recycling mixed plastic waste, generating valuable naptha, lubricants, and feedstock for the plastics industry.

Next step is a proof of concept and discussions for funding this with UK and EU parties - after all morally - and now commercially we can’t keep sending plastic in the 3rd world can we? NSCI has a solution and guess what reader that value as far as the stock market is concerned is ZERO.

GlycoTest and ProAxsis

Most of the H1 2023 losses at NSCI were due to losses of two subsidiary companies: Glycotest, a Philadelphia-based liver disease diagnostics company that is commercialising new and unique blood tests for life-threatening liver cancers and fibrosis-cirrhosis. While ProAxsis is a commercial medical technology focused on respiratory diagnostics. Going forwards both are funded by third-party sources as they move towards their commercialisation so do not require further funding from NSCI. So while that means a dilution in the holdings it also means no more calls on cash.

Conclusion:

There are plenty of other good news stories within the NSCI stable.

DeepTech growing fast. MedTech on the cusp of commercialisation. GreenTech that plays well in a NetZero world.

Similar to GROW, it is using fees from its capital under advisory approach to offset or perhaps one day eliminate the costs of running the fund. This creates a degree of freedom and latitude to retain holdings for longer rather than being constantly churning investments to maintain liquidity.

WH Ireland believe the sum of the parts price should be 188p. It’s easy to see how this could get there.

As ever I hope you enjoy reading what I write. This is not advice.

Oak