NSCI Year End Accounts 2023

£103m assets in play by my reckoning; NAV of £36m

Dear reader,

It’s amazing the photos you can take when you can defy gravity.

Like discounts can defy gravity too. We shall talk about a 53.7% discount today. Or is it 82.8%? Read on reader, read on! It’s amazing the discounts you can find when you can find hidden value.

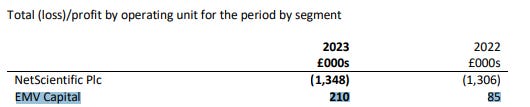

Take Netscientific’s hidden value for example. Its subsidiary holdings do not wholly appear on the balance sheet, nor does its managed capital through both EMV and Martlet appear.

…Except when they become “realised” (sold or disposed) or when they meet certain criteria - like ownership falls below 50%. As it did for DName. This led to a £1.4m gain in the 2023 accounts.

R&D costs from subsidiaries can be capitalised so appear under “Intangible assets” (rather than the cost going to the P&L). Only if it is “probable that future economic value will flow”. Equally if that probability changes you then send it to the P&L as a loss. As happened for ProAxsis’ Covid products.

£21.1m of non-current assets, and net assets of £17.1m do not tell the whole story.

£17.1m of net assets at 31/12/23 were 102% of today’s market cap.

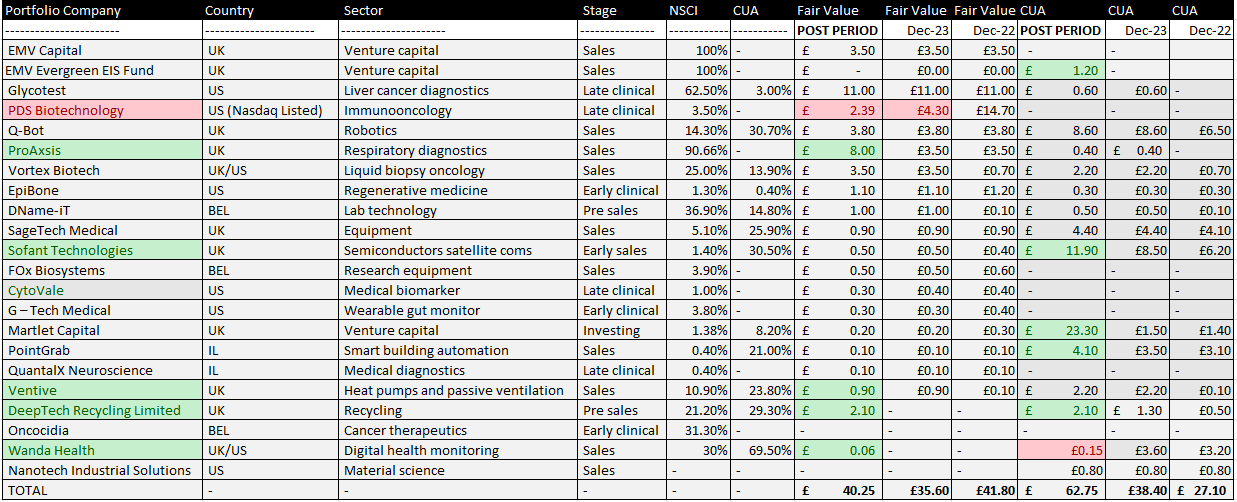

Because NSCI use the acquisition method, and because ProAxsis, Glycotest, EMV and DName-IT (part of Cetromed in the accounts) were not acquired at any significant value they are not valued at “Fair Value” in the accounts.

That £19.2m is largely missing. That’s a further 1.1X the market cap.

The upside for Capital under advisory is also missing. Carried interest or profit share agreements typically range from 15% to 20% of profits earned for investors above a minimum return hurdle rate of c.10%.

But the upside doesn’t end there. Third party Capital under advisory is expected to grow through further syndicated investments in existing and new portfolio companies and the expansion of the funds practice.

Using an average of CuA of £36m, £1.23m of fees is a 3.4% rate. CuA has grown to £62.75m so fees in 2024 should grow to £2.15m. (Even with zero profit share). NSCI want to grow CuA further. At £145m CuA revenue would be £4.9m excluding any upside from profit share. We do need to factor in Martlet’s additional costs but looking at the 2023 accounts the profit of £1.4m suggests costs are modest. Or revenue is disproportionately high? Or did Martlet earn profit share on some of its investments in 2023?

What is the “fair value” of a missing part of NSCI which can generate a £2.1m profit in 2024? How do you value £2.1m per annum profit? 10 times earnings? More? It is growing rapidly after all. But let’s be conservative and assume just 10X. 10X £2.1m is a £21m valuation…. which is 1.25X the price to buy the whole of NSCI!

Visualising the value

So if we map the growing value of NAV (excluding PDS) in orange, that is both growing and exceeds the NAV (black line).

The next 2 blocks of (EMV’s) CuA and Martlet (‘s CuA) are not part of the NSCI NAV just to be clear - but all are growing and I've added them to illustrate the growing value of the funds and assets (and the win-win of fees and profit share). The yellow in the future are the VCT/EIS funds planned. Then finally I split PDS off into the green segment and foresee a 5X return from a buy out in the future e.g. Pfizer.

PDS Biotech update

We now interrupt for a PDS Biotech update

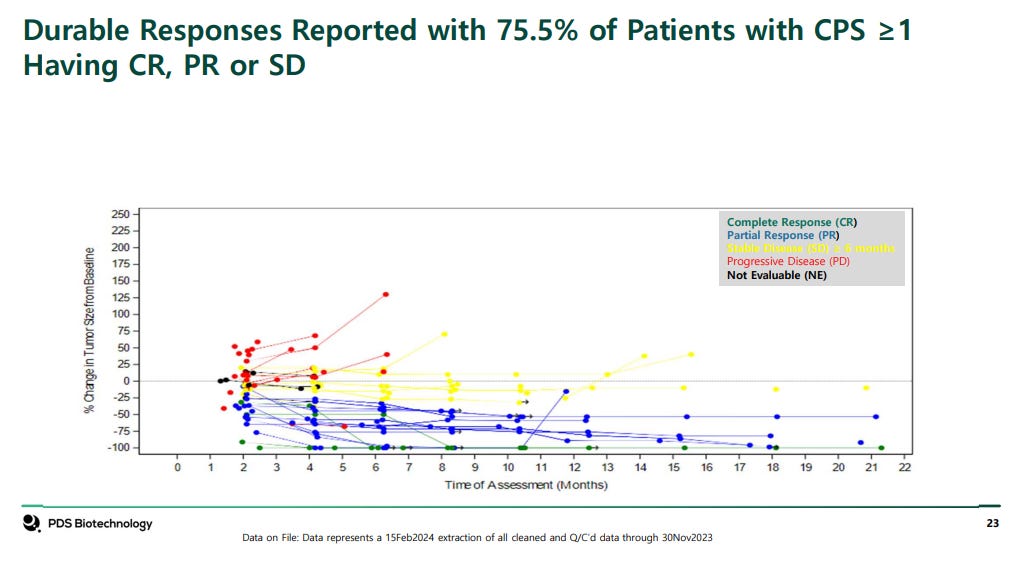

The median survival in the Versatile-002 Phase 2 trial is 30 months. But 6 months on and how many more have died? None.

“27 of the censored patients remained alive and were awaiting their next clinical assessment, 6 censored patients had withdrawn consent for further follow-up, and 2 patients had been lost to follow-up, and 18 patients had died.”

So 1/3 have died, 1/2 are still alive and 1/6 we don’t know either way.

In the other Phase 2 trial and this is a triple combination Merck + PDS Versamune + ICI 75% were either stable or had a partial or complete response. The median survival was 42 months and durable responses of over 75%.

Key events coming in Q3 and Q4:

Conclusion

The post period facts suggest a portfolio of £40.25m. I’m using FY2023’s non portfolio assets and liabilities to estimate there’s -£4m that comes off the portfolio value to arrive at a NAV of £36m. If you agree that’s a 53.7% discount to NAV to today’s share price.

I’ve today argued a £21m valuation of EMV & Martlet based on 10X FY24 forecast earnings is appropriate. If you agree you arrive to a 70.7% discount to NAV.

I’ve also set out a “future” based on a/ a reversion on the PDS holding back to £15m (so a £12.5m gain) b/ a growth in AuM to £145m (from £62.75m today). Using the same 10X valuation and an estimated profit of £4.9m that’s a £28m gain. So £40.5m gain. If you agree you arrive at an 82.8% discount to NAV.

That 82.8% discount assumes zero growth from any other holdings, no buy backs, no realisations, no IPOs, no uprounds. Nor does 82.8% discount factor in a single profit share on those growing capital under advisory balances either.

You might poo poo the thought that the CuA can grow by so much (and that PDS can revert).

But let me leave you with this thought reader. Go back to December 2022 and fast forward 18 months. £27.1m CuA and now £62.75m CuA. NSCI only has to do the same a 2nd time, then the future arrives.

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings including those held in Venture Capital might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"