Oh 'eck, E-Q-TEC

Deep value or in deep trouble?

Dear reader

You’ve got to wonder how many people covering Eqtec (ticker EQT) over the years have smeared their reputations, since it has delivered such a resoundingly poor performance. According to its detractors (and there are many) it is more dog-like than Lassie and the Littlest Hobo combined.

If you say anything even mildly positive then you have to live with that. I reckon a few brokers have lost a lot of credibility with their positive write ups on EQT. A number of readers have asked me to cover it and I’ve been reluctant to do so. I say it as I see it and I was worried I would find deep value, be positive, and be wrong.

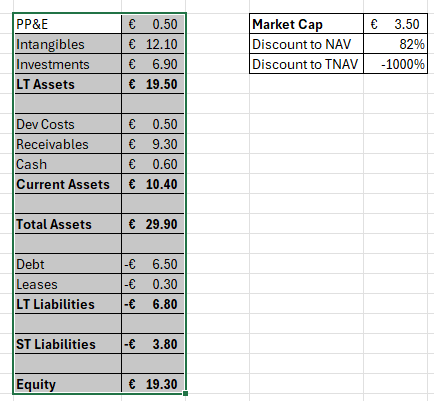

EQT is a £3m market cap and the shareholder’s equity in the last balance sheet is 5X that number… so an 80% discount to NAV. Does that make this an opportunity?

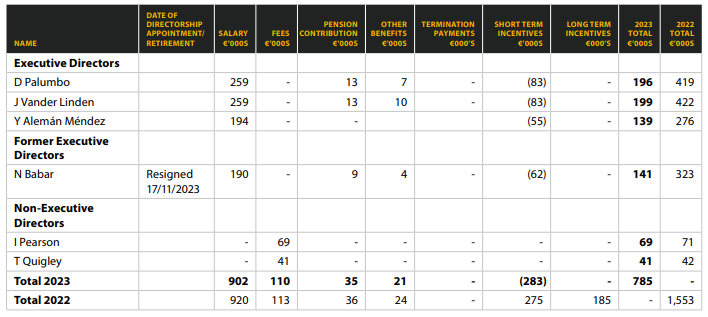

EQT has 611,245,373 shares in issue in new money, equivalent to 61 billion shares prior to a 100-for-1 share reduction. EQT’s CEO David Palumbo is listed as a Director of 49 UK registered companies including Eqtec. Many companies dissolved; I couldn’t be bothered to count how many. Palumbo holds 0.7m shares in EQT so 0.1% of the company and he bought those in October 2023 at a cost of £10,274. Cost around 1 month of his net pay.

Gross pay and emphasis on the first word for Directors is around £0.75m per annum or 25% per annum of the market cap.

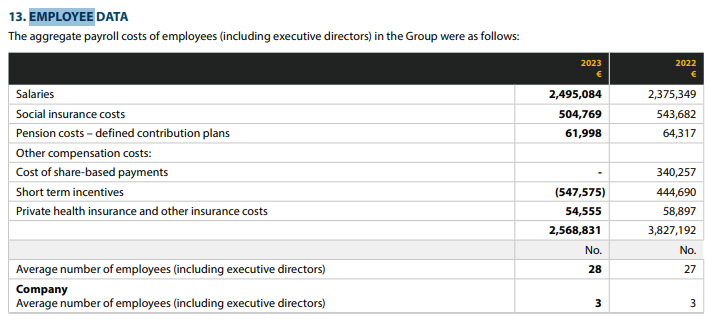

There are 23 employees outside of the 5 Directors who got gross remuneration of €111k on average (€2.57m total) in the last accounts. Those kinds of wages are for engineers and skilled people surely? Not back office admins. If they are engineers then why is that not a cost of sale? I discuss this below.

The EQT web site shows photos of 9 plants (3 are pictured below) giving the impression that their portfolio spans 9 sites. I don’t have any reason to disbelieve the photos.

It probably does have 9 sites at various stages of completion. But it is of little consequence since there is virtually no ongoing recurring revenue from its IP.

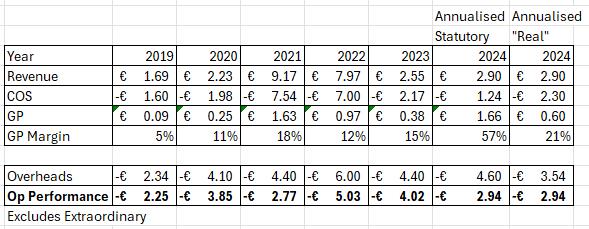

In the last accounts (as at June 2024) the revenue mix was:

“51% from design engineering services, 24% from equipment sales and 25% from operations and maintenance services”

Assuming the same proportion for Cost of Sales then 75% or -€460k of costs in 1H24 was “people costs” (not equipment sales)

Yet the 1H24 wage bill is -€1.3m. If we are very generous and say €300k is back office staff then the real COS wage bill is -€1m. Yes that includes Directors, they don’t get to hide in the back office, I expect them to be part of delivering projects. The CEO, CTO and COO particularly, whereas it’s fair for the non execs to hide.

By doing so we see the 1H24 “transformation” is potentially one of numbers not of performance. Note I’m annualising the interim numbers (doubling) to provide a comparison to prior years. A 21% gross margin is far less impressive than 57%, and in fact strongly suggests that there is no IP to speak of (or what there is cannot attract any kind of premium). It’s just a value judgement that I’m doing but it feels a reasonable one to do.

Or put another way, on a statutory basis on average 11 of 28 people are currently a cost of sale and none of the Directors so incredibly there are more back office people than fee earners despite arguing that they are pursuing “a shift toward high-margin IP-rich services and a departure from high-risk development activities”

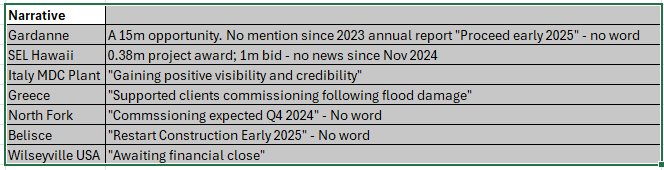

The lack of progress despite being told of expectations of progress in late 2024 or early 2025. Yet here we are on the cusp of summer 2025. Is May 12th still early 2025?

To lose one narrative might be a misfortune but to lose seven narratives, Mr Palumbo, seems like carelessness. The latest slippage and failure is just a continuation of former failures.

I’ve not included the various 2022 and 2023 UK (and elsewhere) failed projects in the above narratives. The balance sheet is where we must consider the value of assets. €19.5m of assets are intangibles and investments. The share is either an 82% discount or the market cap is 10X its assets depending on the answer to the value of those intangibles and investments: €19m or €0m?

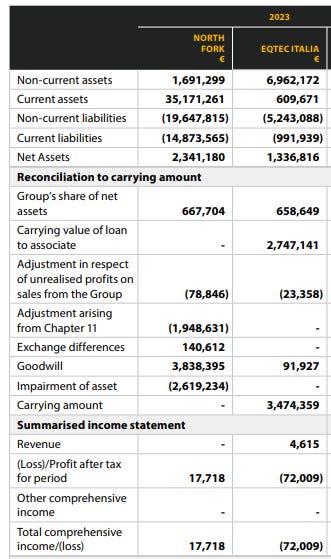

It is terrifying that Eqtec Italia the Tuscan plant half owned by EQT and is part of that €19m valued at €4.4m yet generated €4,615 of revenue and no profit. We get no absolutely no proper disclosure in the 1H24 update other than EQT speaks of “stabilisation” without providing much detail beyond telling us of “funding” from a bank - presumably further project-level debt.

So I can’t ascribe any value to the IP, and the numbers show strong signs that it is actually zero.

Regardless, I see a non-viable operation, I see repeated failures and (if it can be) worst of all dressing up of numbers to present a positive gross profit margin when the truth appears to be quite different.

I wish this were what it is dressed up to be. Intellectual property that chews through the vast waste of waste sounds great. But what problem are we actually trying to solve with “IP”?

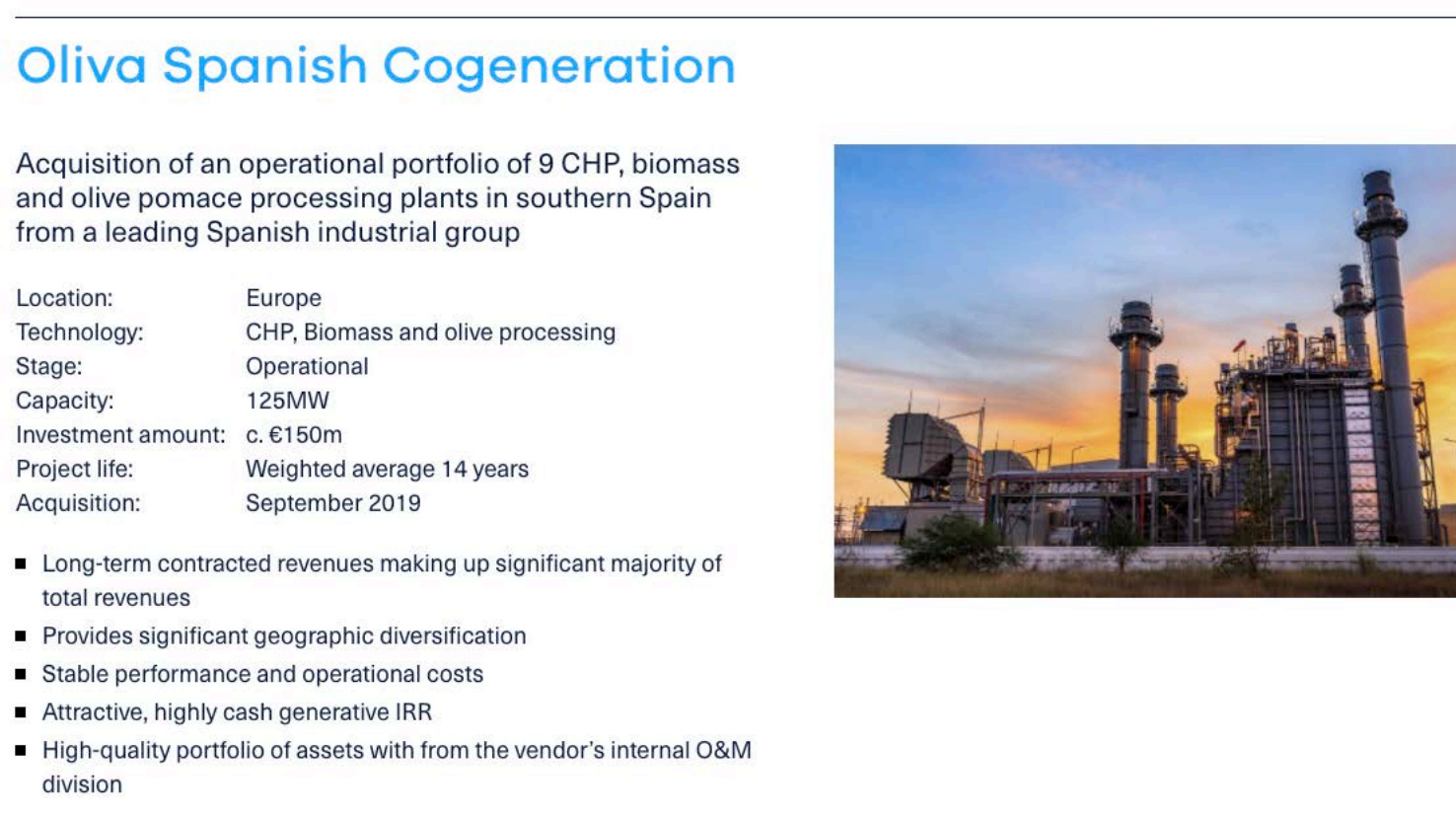

My OB25 for 25 idea SEIT does that already via its holding Oliva. Profitably, with “Attractive, highly cash generative IRR” of €70m EBITDA in 2023 from a €150m investment. It generates a 13.6% dividend or 3.4% each quarter so you can actually SEIT-in-your-bank-account.

Conclusion

There are huge red flags and risks with EQT.

What problem are we actually trying to solve with IP where the market doesn’t already have a solution - like at SEIT’s Oliva?

You make your own decisions but if I were you I’d be joining the folks in today’s picture.

Woof woof.

What’s that Lassie?

Woof!

No pointless running for help on this occasion Lassie; just run.

Regards,

The Oak Bloke.

Disclaimers:

This is not advice; you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"